Here are the latest developments in global markets:

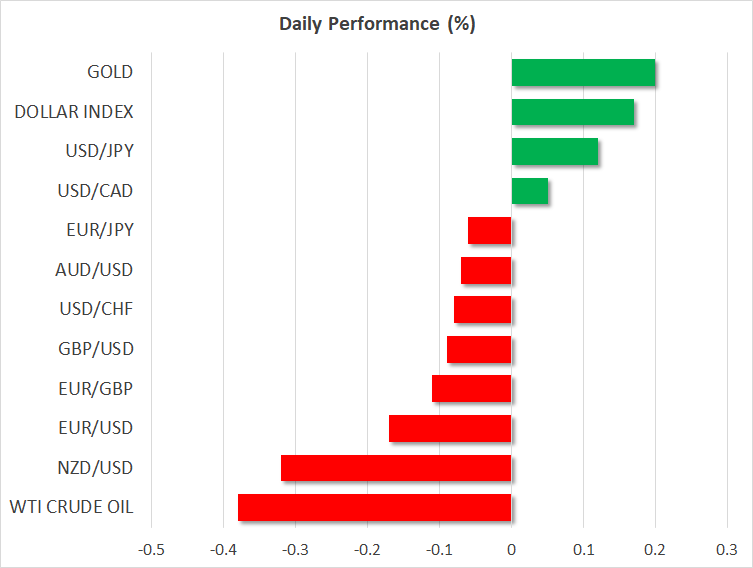

FOREX: The dollar was up by a bit less than 0.2% versus a basket of currencies on Monday. In the absence of major data releases, any updates on the Sino-US trade relationship, as well as any Turkey-related developments may act as the catalysts to steer the currency in either direction.

STOCKS: The Dow Jones, S&P 500 and Nasdaq Composite finished Friday’s trading up by 0.4%, 0.3% and 0.1% respectively, with hopes for a more constructive trade relationship between the US and China acting as one of the catalysts for the move higher. In Asian markets, the Japanese Nikkei 225 and Topix indices both fell by 0.3% on Monday, while Hong Kong’s Hang Seng added 1.3%. At 0712 GMT, futures markets were pointing to a higher open for all major European benchmarks. Meanwhile, contracts on the Dow, S&P and Nasdaq 100 were also suggesting a positive open on Wall Street as well.

COMMODITIES: WTI traded 0.4% lower at $65.84 per barrel. It is notable that the benchmark has retreated in the seven previous weeks. Brent crude was 0.1% down at $71.74/barrel. In precious metals, gold was 0.2% up, trading above its lowest since January 2017 of $1,159.96/ounce hit last week, at $1,186.74. The dollar-denominated metal was suffering lately on the back of the greenback’s strength and also looks unable to attract safe-haven flows stemming from trade and EM uncertainty.

Major movers: Dollar up following the decline late last week; trade, Turkey-related developments eyed

The dollar’s index against a basket of six major currencies was last trading at 96.25, below its highest since June 2017 of 96.98 hit on August 15, but still at relatively elevated levels. The greenback has attracted safe-haven flows recently on the back of trade uncertainty and EM worries largely stemming from Turkey.

Easing concerns on trade, as well as over weakness in the Turkish lira late last week, diverted some funds out of the US currency and threw the dollar index to as low as 96.09, its lowest since August 10. The euro, which has been suffering on the Turkey story due to fears over the exposure of European banks in the country, managed to gain some ground on Friday versus the dollar. On Monday, it is giving back some of those gains, with euro/dollar lower by roughly 0.2% at 1.1418.

Turkish financial markets will be shut for national holidays during August 21-24, which may translate into low trading volumes and large swings in lira pairs. As regards trade, the US and China are now expected to get into talks after holding a largely confrontational stance in previous weeks; August 21-22 were cited last week as the dates for discussions. Markets have been disappointed in the past on this front though and are now perhaps awaiting confirmation that the talks will indeed take place as well as on the nature of such negotiations before taking more aggressive long positions on riskier assets.

It is also noteworthy that there is some speculation in markets for a summit between US President Donald Trump and his Chinese counterpart Xi Jinping in Autumn. The offshore yuan was 0.2% lower against the dollar at 6.8460. Still it held most of its advances from late last week which pushed it away from its weakest since January 2017 of 6.9584.

Dollar/yen and pound/dollar were not much changed. Japan will see the release of inflation numbers during Friday’s Asian session, with safe-haven flows though probably determining the yen’s direction yet again. The UK will not be on the receiving end of important data this week, with any Brexit-developments likely to dictate sterling’s direction.

In the antipodean sphere, the aussie and the kiwi were lower versus their US counterpart after also advancing on Friday; the former was only marginally down. Australia and New Zealand are major commodity exporters and their currencies are sensitive to developments on the trade front.

Elsewhere, dollar/loonie was little changed after retreating considerably on Friday following Canada’s inflation beat. In the aftermath of the data, market participants have fully priced in an additional rate increase by the Bank of Canada in 2018, while they even assign a 13% probability for a second 25bps rate hike according to Canadian OIS.

Day ahead: Trade updates to move markets; US-Turkey political turmoil continues to attract attention

Monday’s economic calendar is light in terms of important data releases, with the trade story remaining on the forefront as investors wait for China and the US to confirm whether they plan to hold lower-level talks this week in Washington, as officials have indicated last week.

According to the Wall Street Journal, the US-Sino trade talks could take place on August 21 and 22 before Washington enforces its tariffs on $16 billion of Chinese imports; Beijing is expected to respond in kind. However, while the meeting could be a sign that the world’s two biggest economies are willing to solve their dispute, the talks could deliver little given that they – at least up to now – are not anticipated to be between high-level officials. Besides, both countries showed no sign of retreating on their demands, a fact that could make tensions difficult to soften.

The confrontation between the US and Turkey, which led the Turkish lira sharply lower against the greenback and spread fears relating to the eurozone’s banking sector, will be also under the spotlight. Relating to this, on Friday, ratings agency Standard & Poor’s downgraded Turkey’s sovereign credit rating further down into junk territory, predicting a recession in the country next year.

In terms of policymakers’ appearances, Bank of Canada Deputy Governor Carolyn Wilkins will be participating in a panel discussion at 1215 GMT, while Atlanta Fed President Raphael Bostic – a voting FOMC member in 2018 – will be speaking on the US economic outlook at 1500 GMT.

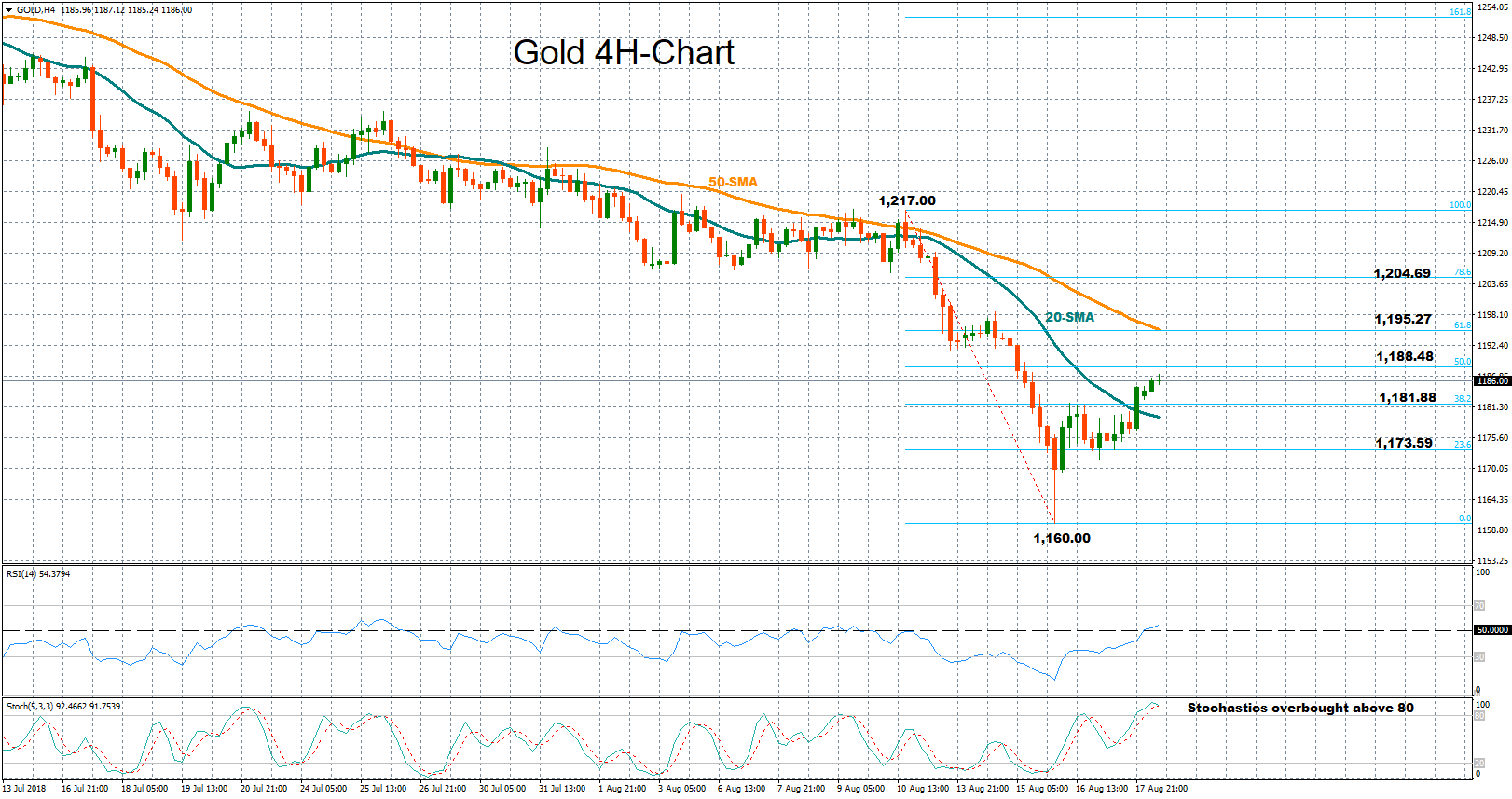

Technical Analysis: Gold appears bullish in the short-term

Gold has risen after touching its lowest since January 2017 of around 1,160 on August 16. The RSI continues to advance in the four-hour chart, having crossed above its neutral threshold of 50. Turning to the stochastics though, they may be cautioning against further gains: the green %K line is looking set to cross below the red %D line (both lines are above the 80 level). Should this materialize, it will constitute a bearish signal in the very short-term.

If the price extends positive momentum, immediate resistance could come at the 50% Fibonacci retracement level at 1,188.48 of the downleg from 1,217.00 to 1,160.00, while further above, the 50-period (simple) moving average and the 61.8% Fibonacci mark, both located at 1,195.27 could also act as a barrier to steeper upside movements. The 1,200 round figure which may be of psychological importance would next come into scope.

On the downside, support could first occur at the 38.2% Fibonacci level at 1,181.88 and then at the 23.6% Fibonacci of 1,173.59, where the market paused for a while last week. More bearish movement would bring last week’s multi-month low of roughly 1,160 into view.