Here are the latest developments in global markets:

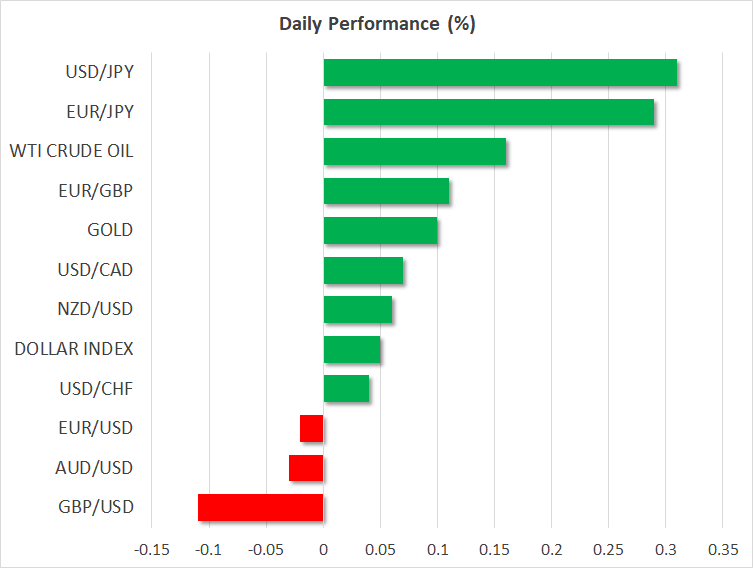

FOREX: The dollar index is higher by a marginal 0.05% on Friday, recouping some of the significant losses it posted in the previous session as risk appetite remained firm and investors pared back more of their safe-haven bets on the US currency. The haven-perceived yen was also on the back foot, performing even worse than the greenback amid this risk-on environment. Meanwhile, the euro and sterling capitalized, both staging a spectacular recovery to touch a three- and two-month high against the dollar respectively.

STOCKS: Both the Dow Jones (+0.95%) and the S&P 500 (+0.78%) closed at fresh record highs on Thursday, with the former finally managing to recover all the ground it lost during the early stages of the year. Trade concerns have taken a back seat for now, with investors breathing a sigh of relief that the latest tariff shots were not as aggressive as feared. The Nasdaq Composite (+0.98%) also surged, though it fell slightly short of reaching its own all-time highs. According to futures, the Dow, S&P, and Nasdaq 100 are all set for a higher open today as well. Asian benchmarks were a sea of green on Friday too. Japan’s Nikkei 225 (+0.82%) and Topix (+0.92%) surged as the yen lost ground, painting a brighter picture for Japanese exporters. In Hong Kong, the Hang Seng climbed by 1.63%. In Europe, all the major benchmarks were set to open higher today, futures indicate.

COMMODITIES: Oil prices are somewhat higher on Friday, with WTI and Brent gaining 0.16% and 0.27% respectively, both attempting to recover the Trump-induced losses they recorded in the previous session. The US President tweeted on Thursday that although the US protects Middle East countries, they continue to push for higher oil prices, concluding that ‘the OPEC monopoly must get prices down now!”. In precious metals, gold is up by 0.10% at $1,209 per ounce, looking set to advance for a third straight session. The dollar-denominated metal has taken advantage of the retreat in the greenback lately, and now looks ready to challenge the upper bound of the sideways range it has been trading in recently, at $1,214.

Major movers: Yen and dollar plummet as risk appetite firms; sterling & euro capitalize

In another session characterized by risk-taking exuberance, major US stock indices like the S&P 500 and the Dow Jones broke fresh records highs on Thursday as investors continued to favor riskier assets, shunning safer ones. Accordingly, the haven-perceived Japanese yen was the biggest underperformer among the G10 currencies, collapsing to a five-month low against the euro. The dollar was the second weakest, as investors continued to unwind safe-haven bets on the world’s reserve currency amid sustained optimism that the Sino-American trade skirmish can still be resolved in a diplomatic manner.

Capitalizing on the weakness seen in the yen and greenback, were the euro and sterling. Euro/dollar surged by over 1 cent in the session to touch 1.1785, a high last seen in early July. Meanwhile, sterling/dollar soared – coming a few pips shy of touching 1.3300 – on the back of strong UK retail sales, though it later gave back some of its gains to settle near 1.3250, as the EU summit in Austria concluded without any signs that a Brexit deal is inching closer. Indeed, EU officials including Commission President Juncker confirmed the UK’s Irish border backstop is not a viable solution, though they maintained a cautiously optimistic tone overall, expressing hopes that common ground can be reached in the coming weeks.

In Japan, PM Shinzo Abe won his third term as the leader of his ruling Liberal Democratic Party. Considering that he’s seen as a major proponent of loose monetary policy, his victory may have signaled the BoJ will continue uninterrupted with its ultra-loose tactics, potentially explaining some of the weakness in the yen. Recall that ‘aggressive monetary policy” is one of the three arrows in Abenomics, the PM’s flagship strategy for fighting deflation.

On the trade front, reports suggest China plans to reduce the tariffs it charges on imported goods from most of its trading partners. Strategically, there was no mention of whether the US will be among these nations, with China likely aiming to use these reductions as a bargaining chip in its forthcoming negotiations with America. Meanwhile, the NAFTA talks between the US and Canada continued, though there was little to suggest a deal is imminent as the unofficial September 30 deadline draws closer.

Day ahead: Eurozone flash PMIs on the agenda alongside Canadian inflation & retail sales

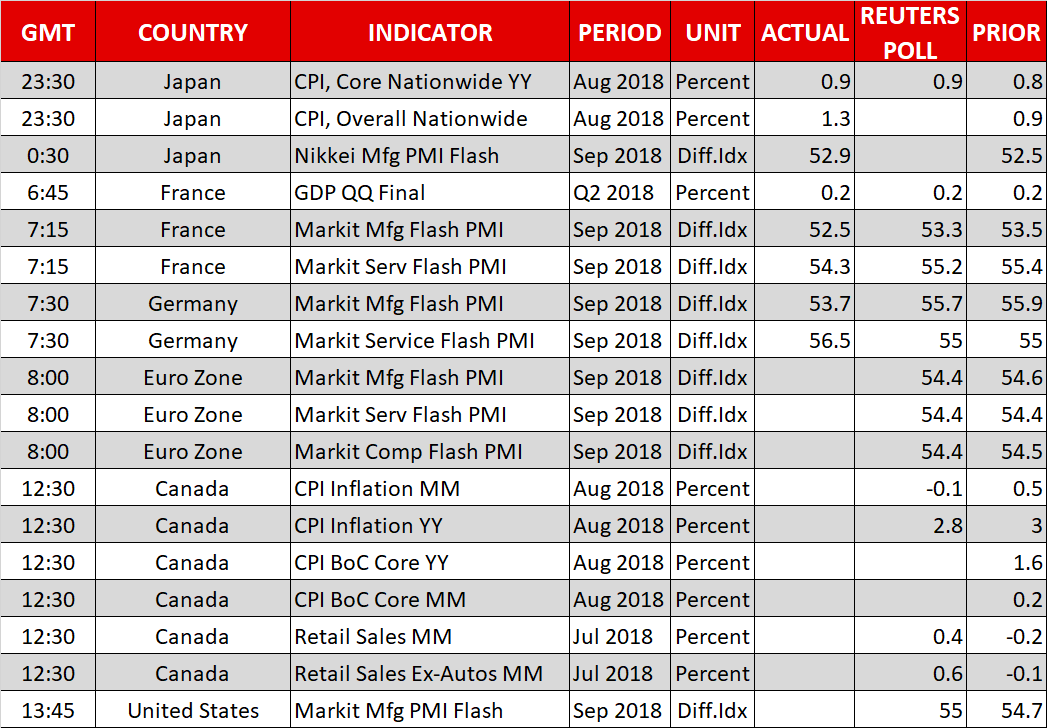

Friday’s calendar includes preliminary September PMI readings out of the eurozone, with the US being on the receiving end of its respective manufacturing PMI print. Elsewhere, important data on inflation and retail sales are due out of Canada which have the capacity to render an October hike by the Bank of Canada a done deal.

At 0800 GMT, eurozone flash manufacturing and services PMIs, as well as the composite PMI that blends the two sectors and which is viewed as a good overall growth indicator for euro area economies, will be made public. The manufacturing PMI is projected to slightly weaken relative to August, maintaining its overall down movement after hitting its highest on record in December last year. Specifically, it is expected at 54.4, its lowest since late 2016. The services PMI is forecast to remain steady at 54.4 and the composite PMI to marginally weaken to 54.4, both standing at a distance to peak levels tracked in January of the current year.

Despite these measures retreating from robust levels recorded in late 2017 – early 2018, it bears mention that they still remain comfortably in expansion territory above 50. Meanwhile, it would be interesting to see whether rising global trade tensions yet again weighed on these gauges.

Germany and France, the eurozone’s two largest economies, saw the release of their respective PMI prints earlier in the day. The French prints dissapointed, declining by more than expected, as did the German manufacturing index, though Germany’s services figure surprised positively.

Canadian inflation and retail sales figures for August and July respectively are due at 1230 GMT. Inflation as measured by the consumer price index (CPI) is anticipated to contract by 0.1% m/m, after rising by 0.5% in July. This would put the annual pace of growth at 2.8%, below July’s 3.0% which was the fastest pace of expansion since September 2011. Core CPI that excludes volatile items including energy which was the primary contributor to July’s rise in headline inflation will be monitored, as well as the core measures of inflation utilized by the BoC in its policymaking (CPI common, median and trimmed); no polls are available for these data.

On the retail sales front, both headline and core retail sales that exclude automobiles are anticipated to re-enter positive territory after contracting in June. Upbeat data out of Canada can even more conclusively put on the table a 25bps rate increase by the Canadian central bank in late October; the odds for such an outcome are already running high according to Canadian OIS (86%).

Also Canada-related, ongoing efforts for a new North American trade deal remain fruitless. Any headlines on this have the potential to move the loonie.

Markit’s September flash manufacturing PMI for the US is projected to show an improvement, with the gauge standing at 55.0, from August’s 54.7. The reading is slated for release at 1345 GMT.

In energy markets, the weekly Baker Hughes report on active oil rigs in the US due out at 1700 GMT will be attracting interest. Beyond this, a weekend meeting between OPEC countries and other allies taking place in Algeria may offer short-term direction to oil prices; oil output will be discussed during the gathering. In the meantime, some Trump Twitter comments managed to weigh on oil prices.

The US equity session might be lively due to ‘quadruple witching”.

Lastly, on Sino-US trade relations, there seems to be some euphoria stemming from the belief that the two sides are getting less confrontational. This is somewhat puzzling to say the least, given no concrete indication pointing to that direction.

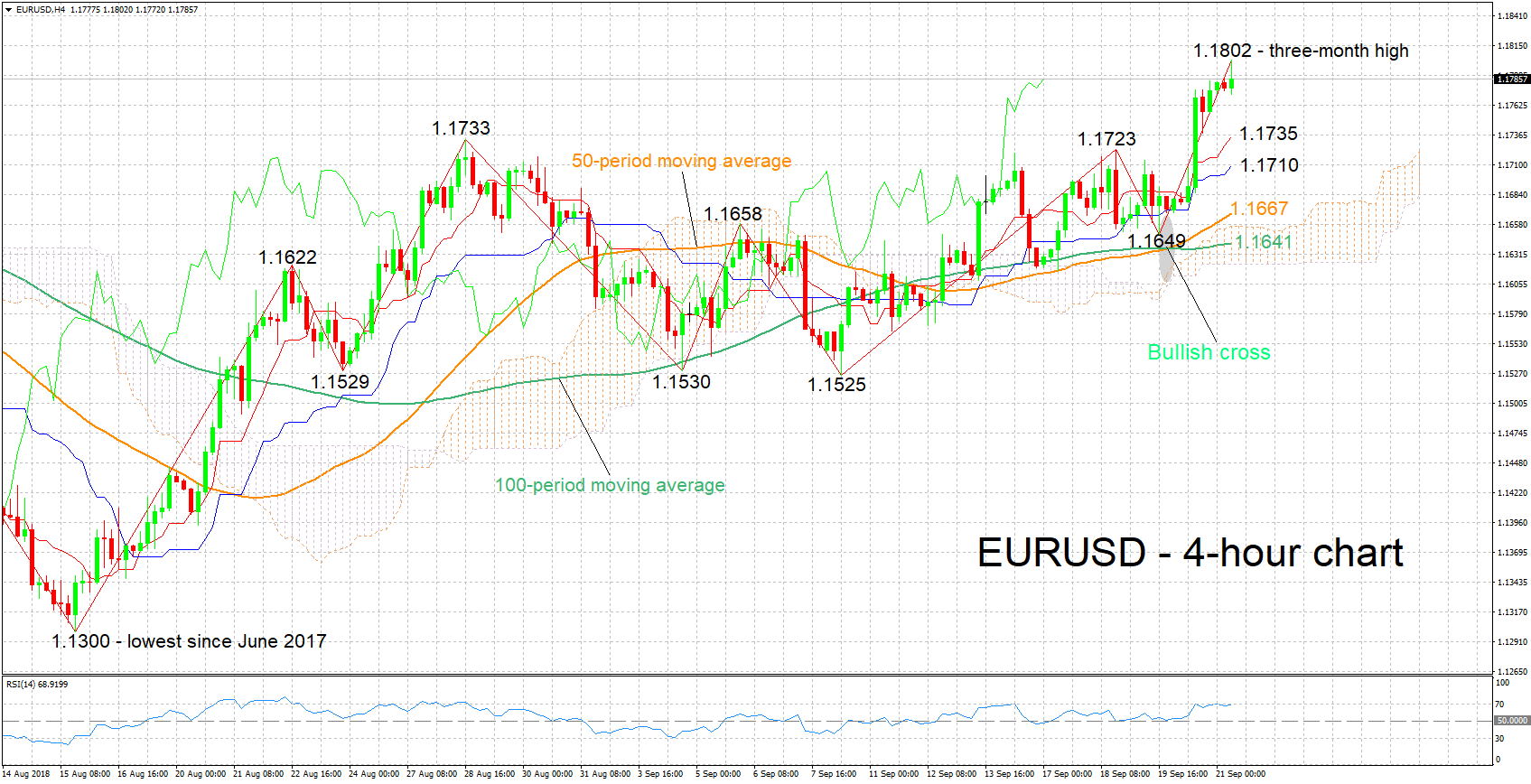

Technical Analysis: EURUSD pierces through 1.18 to hit 3-month high; RSI close to overbought levels

EURUSD hit a three-month high of 1.1802 earlier in the day. The Tenkan- and Kijun-sen lines are positively aligned, in support of a bullish bias in the short-term. The rising RSI lends credence to this view. Notice though as well that the indicator is close to its 70 overbought zone.

Upbeat eurozone PMI figures are likely to push the pair further up. Immediate resistance may come around the 1.802 peak, with the 1.19 round figure increasingly coming into focus afterwards.

On the downside and in case of disappointing numbers, support may come around the current levels of the Tenkan- and Kijun-sen lines at 1.1735 and 1.1710 correspondingly. Further below, the region around the 50-period moving average at 1.1667 would be eyed.

{kind=link}