After touching its highest levels in 2018, the US dollar lost some of its shine in recent weeks, leading one to question whether this is simply a correction in a broader uptrend, or the early days of sustained weakness for the world’s reserve currency. While trade tensions and relative rates could continue to support the greenback for now, a paradigm shift may be in the works heading into 2019, as the Fed approaches “terminal” rates at a period when the ECB prepares to raise its own.

The US currency enjoyed a sweet spot in recent months, gaining ground against all its major counterparts since early April. A fiscally-turbocharged US economy, consistent rate increases by the Fed, and haven inflows by investors seeking shelter for their funds amid escalating trade tensions, all played a large role. Separately, other major currencies like the euro and sterling have been in a “soft patch” of their own. The ECB managed to push the euro lower even while announcing QE tapering, with worries around the Italian budget contributing to the losses, while Brexit risks have been holding the pound down – further pushing investors towards the dollar for a lack of attractive alternatives.

Yet, the dollar’s recent dip has brought this whole narrative into doubt, leading one to question whether this is merely a correction lower in a bigger uptrend, or the beginning of a broader sea-change. So, what factors are currently arguing for weakness in the world’s reserve currency, and what points to a rebound?

US is strong, but most “good news” may be priced in by now

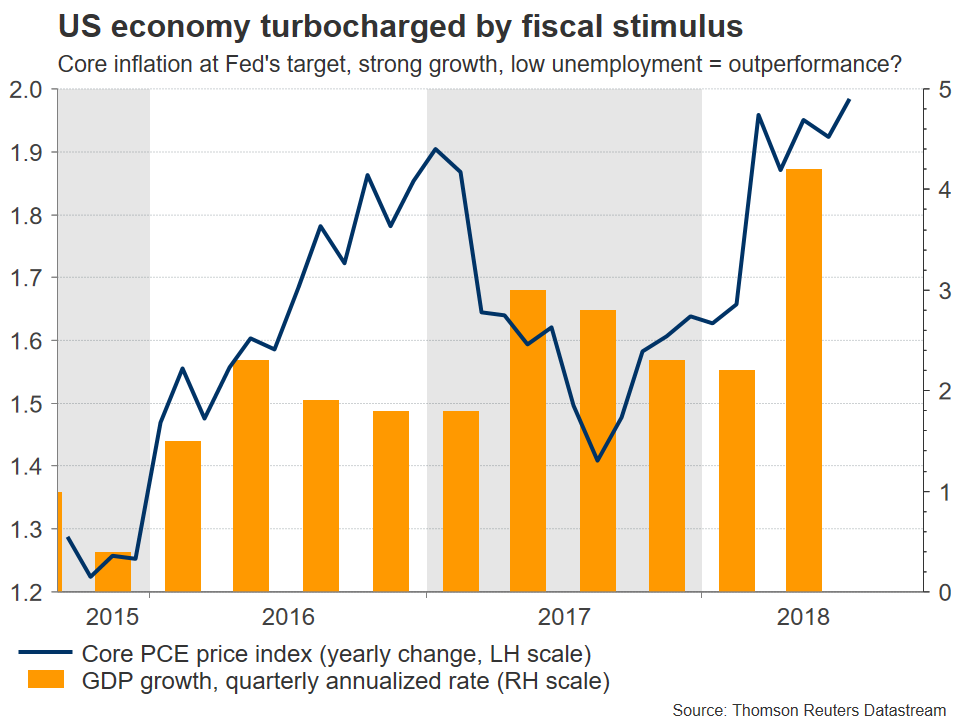

There’s no denying the US economy is robust. Economic growth is above trend and above potential after the recent tax cuts, wage growth seems to be picking up amid a very tight labor market, and core PCE inflation is exactly in line with the Fed’s 2% goal. “Soft data” concur, with NFIB business optimism reaching its highest since records began, consumer morale at 18-year highs according to the CB survey, and both ISM PMIs resting at elevated levels. In the context of financial markets though, it’s fruitful to consider how much of a narrative is already priced into an instrument. In this sense, one could argue most of the “good news” are likely reflected into the dollar’s price already, as the “US outperformance” theme has been dominating for months now.

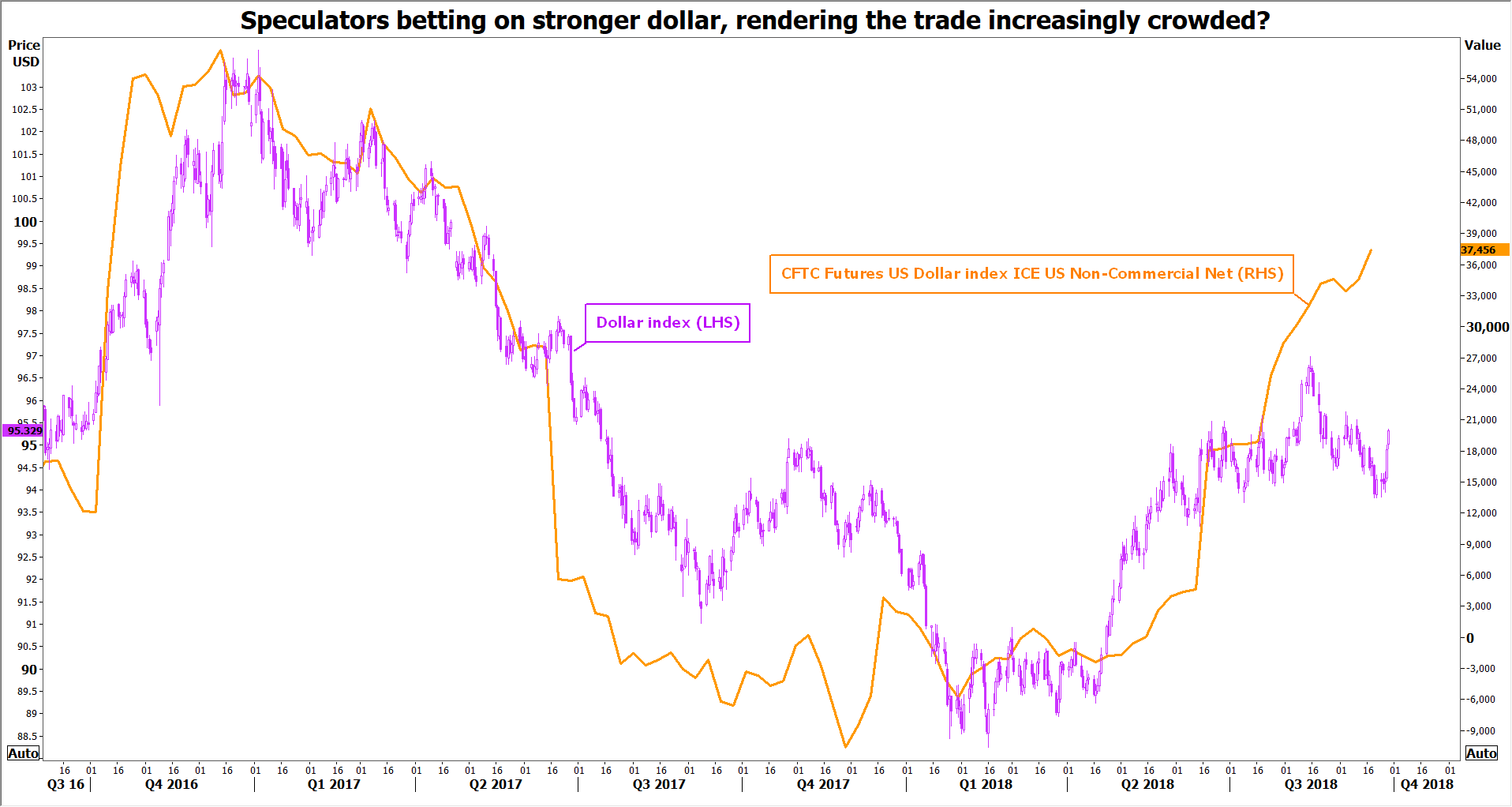

Adding credence to this view, is market pricing around the Fed. Investors currently assign an 80% probability for the central bank to raise rates by a quarter-percentage point in December according to Fed funds futures, while 2 more hikes are largely baked in for 2019 (versus the 3 signaled by the latest Fed “dot plot”). In isolation, this implies the dollar is unlikely to draw too much strength from monetary policy moving forward, even if the Fed proceeds as it expects. Enhancing this concept, is the extent of speculative bullish bets on the currency, which recently touched a one-and-a-half year high, suggesting that long-dollar is becoming an increasingly crowded trade.

Monetary policy divergence nearly run its course

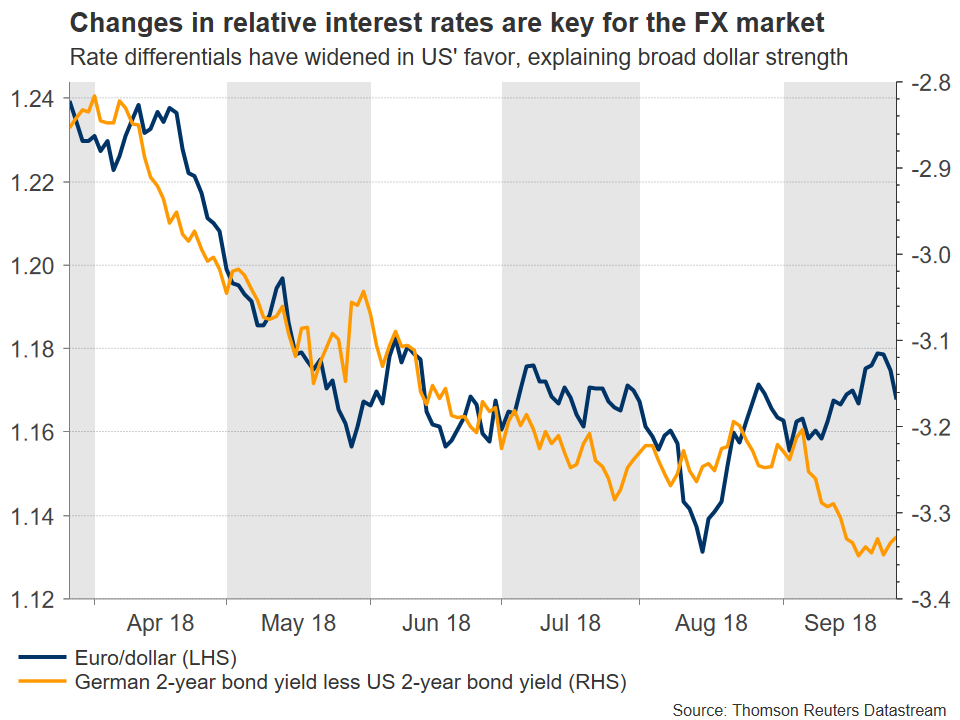

Staying on central banks, it’s worthwhile to consider what other policymakers around the globe are doing. Relative rate differentials between two economies are one of the most important drivers of a currency pair, and much of the dollar’s gains recently were owed to these spreads widening in the US’ favor, as the Fed was among the few central banks raising rates.

Alas, this theme of “monetary policy divergence” may have nearly run its course, giving way to a regime of “policy convergence”, with the likes of the European Central Bank (ECB) announcing rate hikes for next year. In contrast to the Fed, markets haven’t priced too much tightening by the ECB, which suggests the euro may have room to run higher as the first hike draws nearer and markets reprice the rate path. Euro strength typically brings dollar weakness, not least due to the euro holding almost 60% of the weight in the dollar index. While this may be more of a 2019 story, it’s still worth keeping a close eye on.

In the more immediate term, the Italian budget outcome will be key for the euro. Risks surrounding a large budget deficit leading to a “standoff” with the EU have added a significant risk-premium on the euro, dragging the currency lower. While this premium may linger for the time being, should the two sides eventually manage to reach a compromise that avoids a clash, then the single currency could rally in relief.

Other major currencies waiting for a comeback

Beyond the euro, consider the British pound and the yen for a moment, which have been battered by uncertain politics and ultra-loose monetary policy respectively, rendering them quite “cheap” from a long-term valuation perspective. Should UK political risks recede (a Brexit deal) or should the Bank of Japan hint at scaling back stimulus, then these currencies may well stage a comeback – taking demand away from the dollar. Added to these, is the prospect of a rebound in the Chinese yuan, in the (unlikely) event that trade tensions subside sometime soon.

What about upside risks?

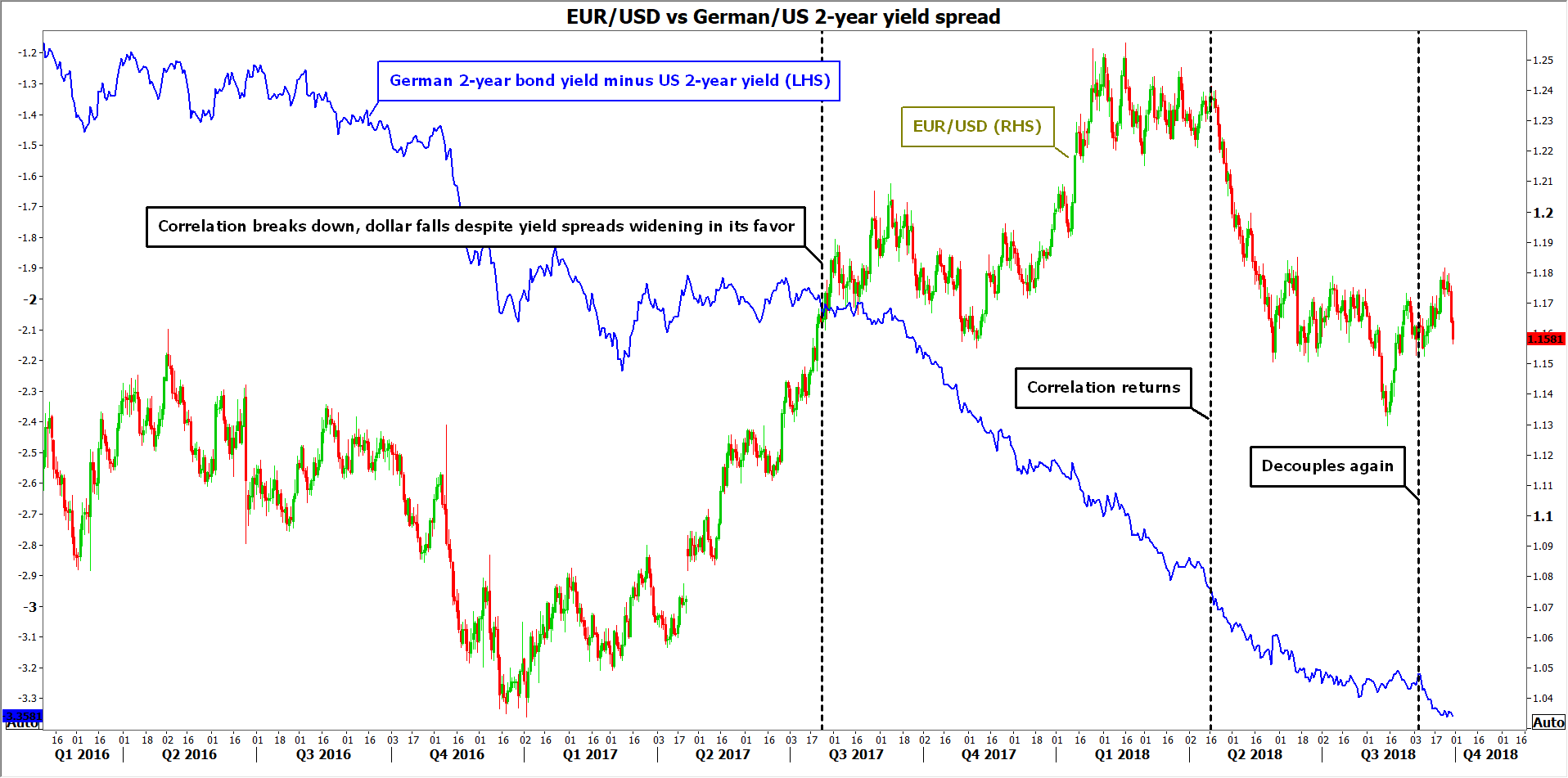

The main one relates to the recent surge in US bond yields, and the potential for that to continue. A rise in Treasury yields is traditionally associated with dollar gains, as higher interest rates make the currency more attractive for foreign investors. Yet, while both short- and long-dated US yields have moved higher over the past month, the dollar has pulled back, similar to what transpired in late-2017.

History suggests the two will eventually recouple. The question is whether it will be US yields that turn lower to meet the dollar, or whether the currency will eventually recover amid a continued upturn in yields. When the correlation broke down in late-2017, it was the dollar that eventually raced higher in April of 2018 to meet elevated yields, though that doesn’t mean the same will play out this time around. Make no mistake, this will probably be the most important driver for the dollar moving forward; the currency is unlikely to remain indifferent to a sustained rise in yields for too long, as much as it is unlikely to escape unscathed in case yields come crashing down.

Another upside risk relates to trade, and the prospect of a further escalation in tensions that diverts safe-haven flows into the dollar. To explain – the greenback has been acting as a haven asset amidst trade worries, benefiting when frictions intensified under the view the US economy is better prepared than others to weather any “trade storms”. Hence, increased concerns around trade could prop-up the greenback, though in similar logic, a potential de-escalation in tensions may equally trigger a rotation away from the currency.

Patches of dollar strength left, but broader tide may be turning

With the Fed being nearly – but not fully – priced in over the next quarters, relative rates could continue to act as a source of support for the dollar in the near-term. A possible heating up in trade tensions could also contribute to periodic “patches” of dollar strength. In a broader context though, especially looking towards 2019, the outlook becomes increasingly clouded as the Fed approaches “terminal” rates and prepares to pause hikes at a period when the ECB will be gearing up to raise its own rates, lessening the dollar’s carry appeal.

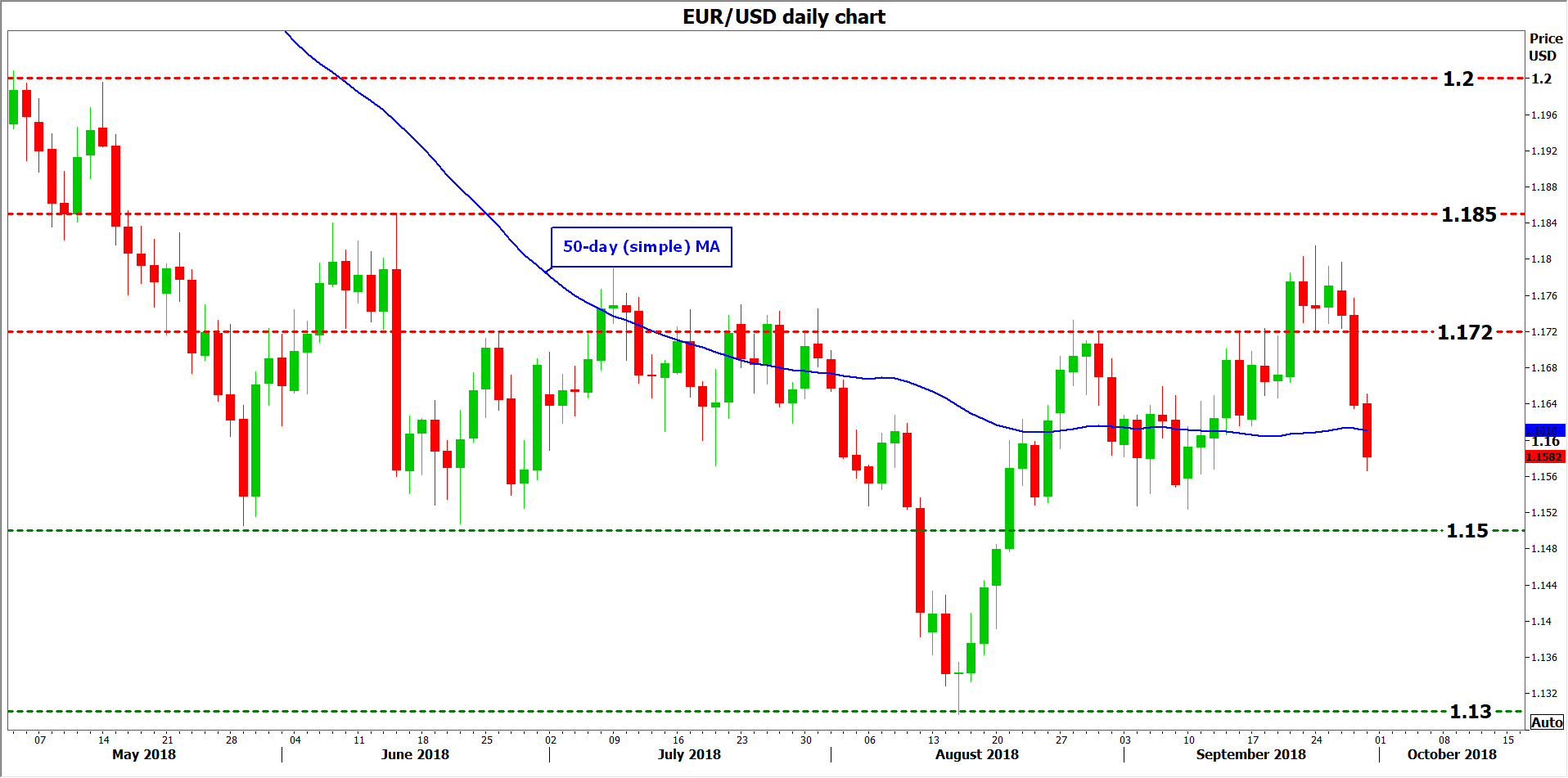

Against this backdrop, while euro/dollar could well challenge the 1.1500 area soon on the back of Italian-budget woes, the risks surrounding the next “large” move seem to be tilted towards the pair eventually visiting the 1.2200 neighborhood again, and not 1.1000. A key level to watch in this respect is the 1.1850 hurdle, which has acted as a significant resistance barrier this year. A break above it is needed to shift the technical outlook to “cautiously positive”, with a move above 1.2000 as well turning it decisively positive. On the downside, a clear break below 1.1500 could be a signal for further declines, initially towards the 1.1300 zone.

{kind=link}