Here are the latest developments in global markets:

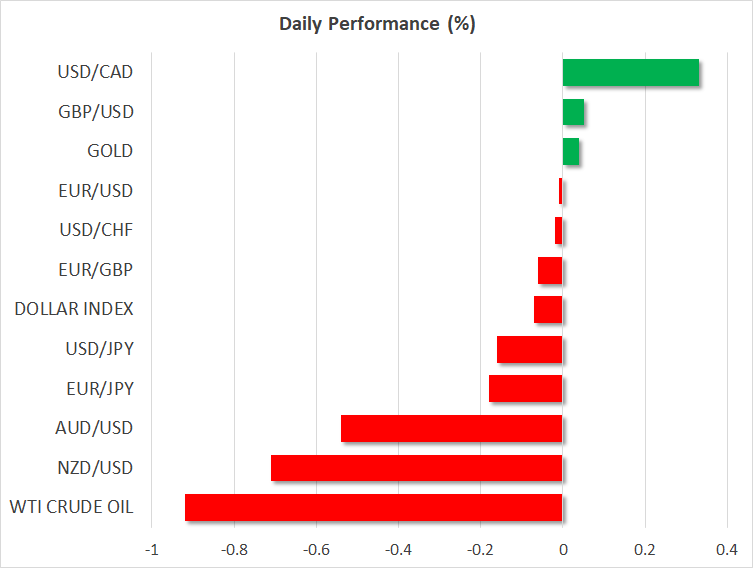

FOREX: The dollar index is little changed on Friday (-0.06%), holding on to the gains it recorded yesterday. Although there wasn’t anything new out of the US, the greenback capitalized on weakness in the euro and sterling (see below), touching fresh two-month highs against both. Meanwhile, the safe-haven Japanese yen is outperforming today, as the recovery in risk sentiment seen yesterday appears to have been short-lived. Consequently, the commodity-linked currencies (aussie, kiwi, and loonie) are all on the back foot.

STOCKS: US markets rebounded on Thursday, with the S&P 500 (+1.86%) and the Dow Jones (+1.63%) recovering some of their recent losses, bringing their year-to-date performance back to positive. Meanwhile, the tech-heavy Nasdaq Composite (+2.95%) outpaced its peers, aided by upbeat earnings from Microsoft (+5.84%). That said, sentiment reversed after US markets closed and Amazon as well as Google-parent Alphabet reported disappointing revenues. Accordingly, futures tracking the S&P, Dow, and Nasdaq 100 are all flashing red again, pointing to a negative open today. The pessimism spilled over into Asia on Friday, with Japan’s Nikkei 225 (-0.40%) and Topix (-0.31%) inching lower, alongside the Hang Seng in Hong Kong (-0.76%). Europe didn’t escape unscathed either, with all the major indices expected to open notably lower today, futures suggest.

COMMODITIES: Oil moved in line with stocks, namely higher yesterday as risk appetite recovered, and lower today amid renewed pessimism. In terms of fundamentals, Saudi Arabia’s OPEC governor said yesterday that oil markets could face oversupply by year-end, something evident by rising inventories. WTI is down by 0.90% today at $66.63 per barrel, and Brent is lower by 0.98% at $76.14/barrel. In precious metals, gold is practically flat on Friday at $1233 an ounce, slowly grinding higher amid the general risk-off undertones in recent days.

Major movers: Stocks bounce, but still on wobbly legs; no love for euro after ECB

US equity markets staged a comeback on Thursday, recovering some of their losses from earlier in the week, without any fresh trigger. That said, sentiment seems to have turned sour again, with Asian markets being a sea of red on Friday, and futures tracking the US indices pointing to a lower open today, following lackluster earnings from tech heavyweights Amazon and Google parent Alphabet. Indeed, the earnings season has been mixed at best so far, lending increasing credence to the narrative that profit growth may have already peaked, and potentially helping to explain the recent weakness across equities. Some reports that the US won’t resume trade talks without a firm proposal from China probably didn’t do risk appetite any favors either.

In FX markets, the euro found no love after the ECB meeting yesterday, even though President Draghi appeared as confident as he could be, given the current landscape. The ECB chief acknowledged the weaker momentum in economic data, but downplayed it as growth merely returning to “normal” levels after being above potential in 2017. He also noted the risks are not dire enough for the ECB to downgrade its balance of risks from “roughly balanced”, hinting that recent developments won’t derail – or even delay – the Bank’s normalization plans. Yet, the euro touched a fresh two-month low against both the dollar and yen in the aftermath. Looking ahead, S&P is expected to announce its review on Italy’s credit rating today; a potential downgrade could keep the single currency under pressure.

Sterling underperformed even the soft euro, tumbling to its own two-month lows against the dollar and yen, in the midst of reports that PM May’s Cabinet cannot agree on a way forward for the Brexit talks to resume. Specifically, over how to avoid customs checks at the Irish border, without the UK remaining in the EU’s customs union indefinitely. The news likely poured cold water on optimism that a deal may be outlined on time for the EU to hold a special summit in mid-November, signaling that the proverbial can may indeed be kicked further down the road to December.

Elsewhere, the commodity-linked currencies aussie, kiwi, and loonie recorded meaningful losses earlier today as sentiment shifted back to “risk-off”. Aussie/dollar touched a fresh 2½ year low. Accordingly, the defensive yen is outperforming.

Day ahead: US GDP growth takes center stage

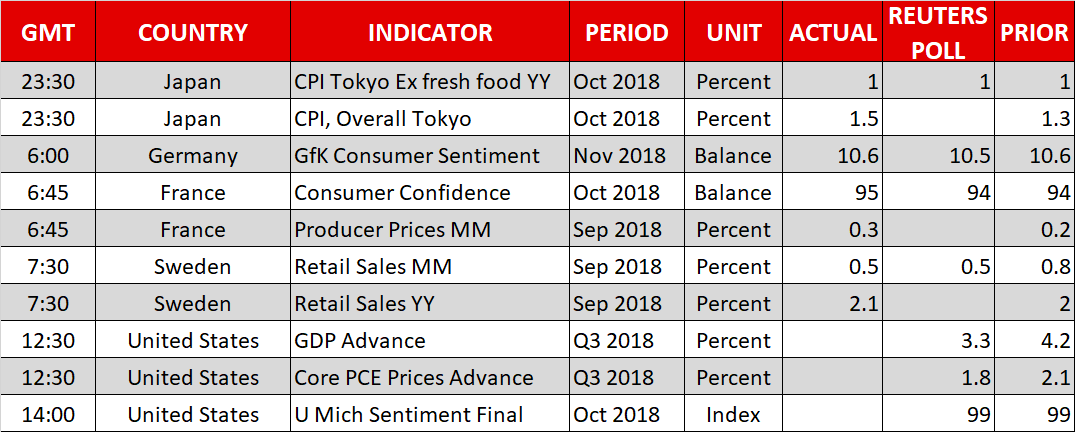

US GDP growth for the third quarter will be the highlight release of the day (1230 GMT) and may prove to be another win for President Trump if the figures surprise to the upside, indicating that the 3.0% growth target set by the his administration is achievable by the end of the year. Better results could also help Trump’s Republicans to gain support in the midterm elections as so far polls suggest they are behind the Democrats.

According to analysts, the world’s biggest economy is said to have expanded by 3.3% in annualized terms in the three months to September, after hitting 4.2% in Q2, the fastest rate recorded in four years and almost twice the 2.2% pace it printed in Q1. Even if forecasts for a slowdown prove accurate on Friday, such an expansion is still a healthy one as long as it is bigger than 2.0% and smaller than 4.0%, which economists consider an optimal range for GDP growth.

As risk aversion grows in FX and stock markets amid disappointing earnings releases and fears about the consequences the US-Sino trade war could have in global economy, an upbeat GDP report out could somewhat calm investors by showing that things are not evolving that bad after all. In such case, demand for dollar could go up, while US stock futures may turn green before the US market open. The core Personal Consumption Expenditure Index for the third quarter delivered alongside the GDP figures will be also eyed for evidence on inflation trends, while the final October University of Michigan Consumer sentiment index will come in light at 1400 GMT.

In equities, Moody’s corporation and Royal Bank of Scotland will be among companies reporting quarterly earnings results prior the market open.

In public speeches today, ECB President Mario Draghi will be presenting at a conference on “Understanding inflation dynamics” at 1400 GMT. A few minutes later at 1415 GMT ECB Executive Board Member Benoit Coeure will be commenting at a session on “Central banks facing a global interdependent financial and monetary environment” during the Euro 50 – CF40 – CIGI meeting in Paris.

After Moody’s downgrade, the S&P will be the next to review Italy’s sovereign credit rating today along with Germany and the UK. The latter will be also rated by Fitch

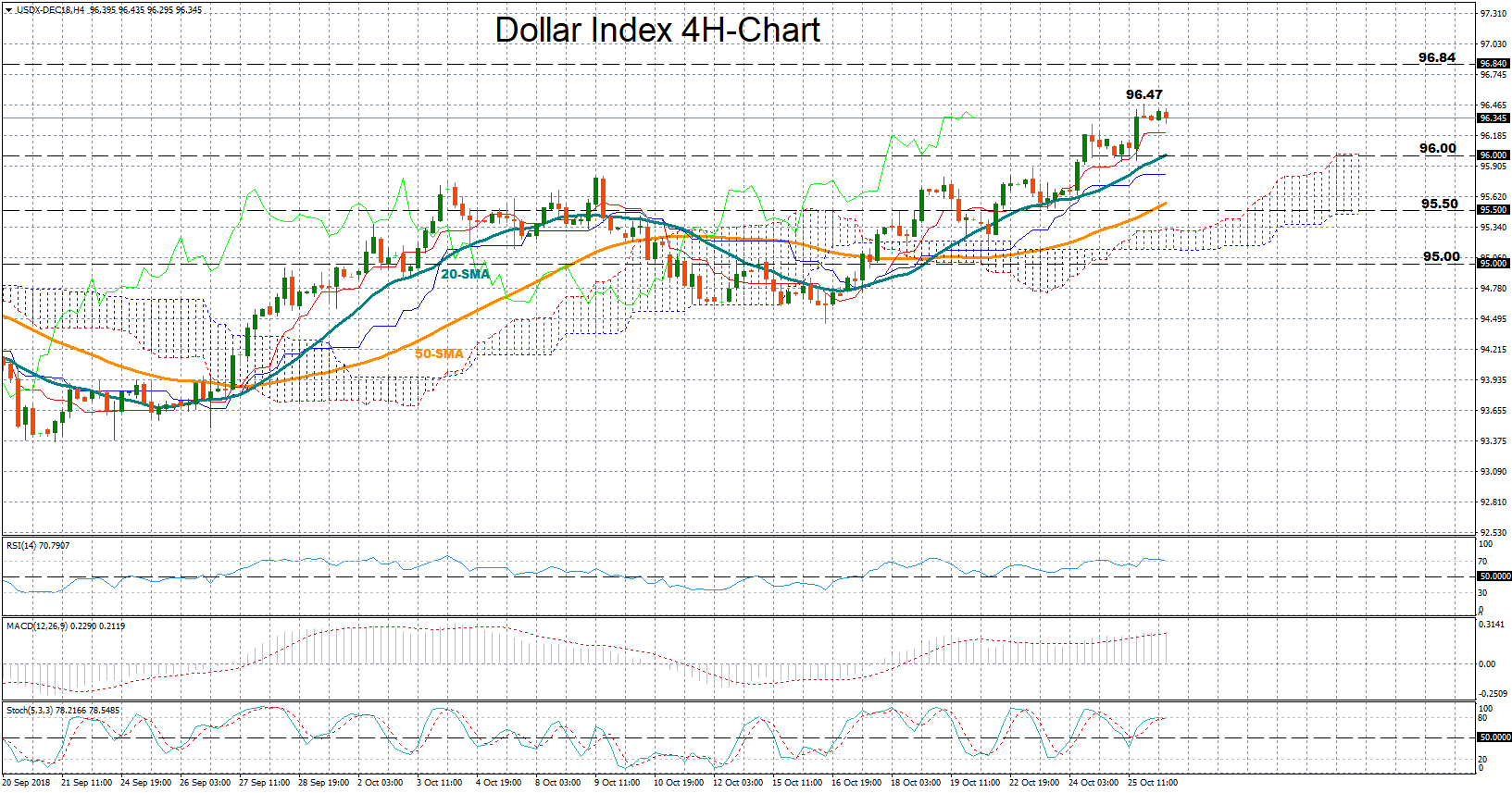

Technical Analysis – Dollar index unlocks fresh 2-month highs; looks overbought

The dollar index which gauges the strength of the dollar versus six major currencies hit a new two-month high at 96.47 on Thursday. Today the index trades sideways around this peak, with the RSI lacking direction above 70 in overbought territory and Stochastics being ready to reverse lower after touching the 80 overbought mark. While this is a signal that the recent rally could be overdone, and the bears may be waiting around the corner, the MACD holds above zero and its red signal line, suggesting that any weakness could be short-lived.

Yet if US GDP growth surpasses expectations, the dollar could pick up steam to retest yesterday’s top 96.47. Above from there, the way could open towards the more-than-a-year high of 96.84 reached on August, while if this proves easy to get through, the next level to watch could be 97.60, a previous resistance area in 2017 and 2016.

Alternatively, disappointing prints would boost risk aversion, sending the index down to the area between 96 and 95.50 where the price paused several times in previous sessions and the 20- and the 50-period moving averages currently stands. Moving lower, the 95 psychological level could be another level to keep in mind.

{kind=link}