Thursday will be a busy day for US data with a slew of releases on the agenda. The delayed durable goods orders report for December, due at 13:30 GMT, could be overlooked in favour of the more up-to-date manufacturing activity indicators for February. The Philly Fed manufacturing index will be posted at 13:30 GMT, followed by the IHS Markit manufacturing PMI at 14:45 GMT. Existing home sale for January will also be watched at 15:00 GMT. The US dollar could swing from the data, especially if there’s any surprises in the manufacturing surveys or home sales, however, with more important numbers coming up next week, the moves are likely to be contained.

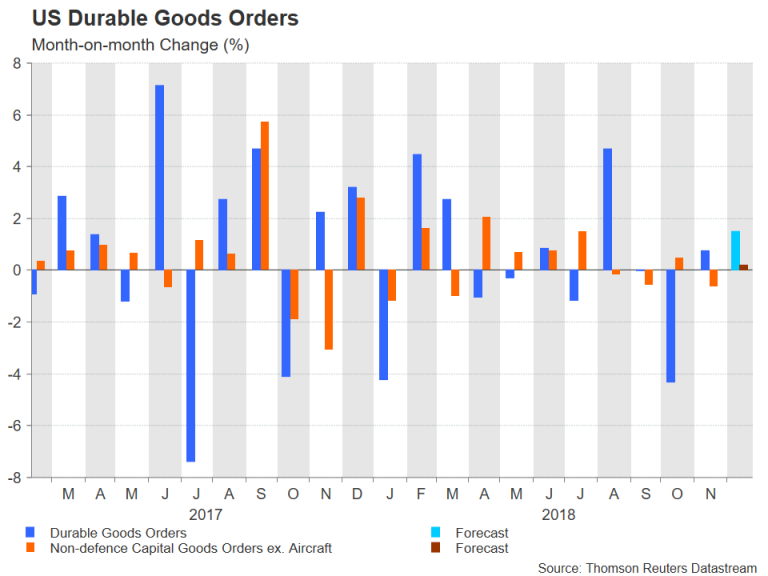

Durable goods orders are forecast to have increased for the second month in a row in December, rising by 1.5% month-on-month after a 0.7% bounce in November. Core capital goods orders, which exclude defence and aircraft orders, are anticipated to have risen by 0.2% m/m, recovering partially from a 0.6% drop in the prior month. A strong reading in the core number, which is used in GDP calculations, would point to a positive end to the fourth quarter. US growth figures for Q4 have yet to be released and are not scheduled until February 28 as they were pushed back due to the government shutdown lasting for most of January.

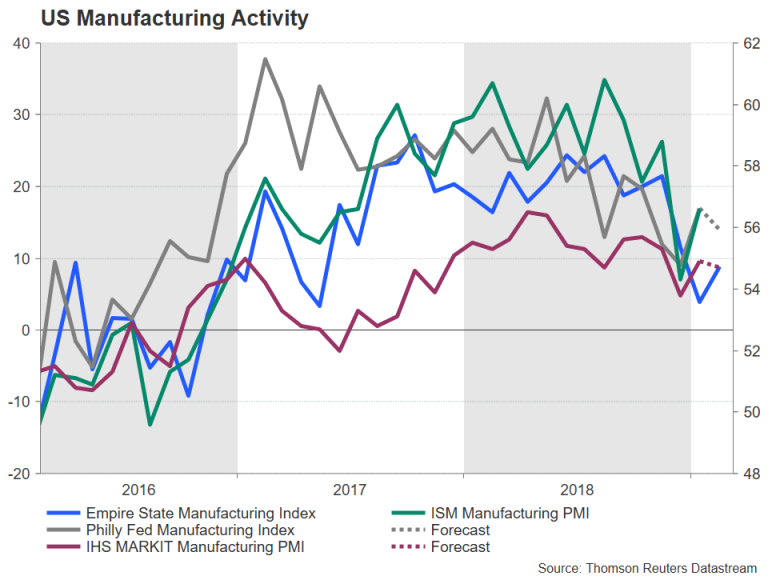

Like in much of the rest of the world, manufacturing activity in the US deteriorated significantly in the final months of 2018, but there was relief when the US indices bounced back in January. That trend might not continue in February as both the Philly Fed manufacturing index and the IHS Markit manufacturing PMI are forecast to have moderated slightly, declining to 14 (from 17) and to 54.7 (from 54.9), respectively. Worse-than-expected figures could revive fears of a sharp slowdown amid a global downturn and ongoing trade uncertainty.

Lastly, existing home sales for January might attract some attention as investors will be looking for a small rebound of 0.8% m/m following a 6.4% plunge in December. The US housing sector has been the most hit by rising Fed interest rates. However, there have been some signs lately that the slowdown in the housing market may have started to ease so a disappointing reading in existing home sales could cast doubt about a possible recovery.

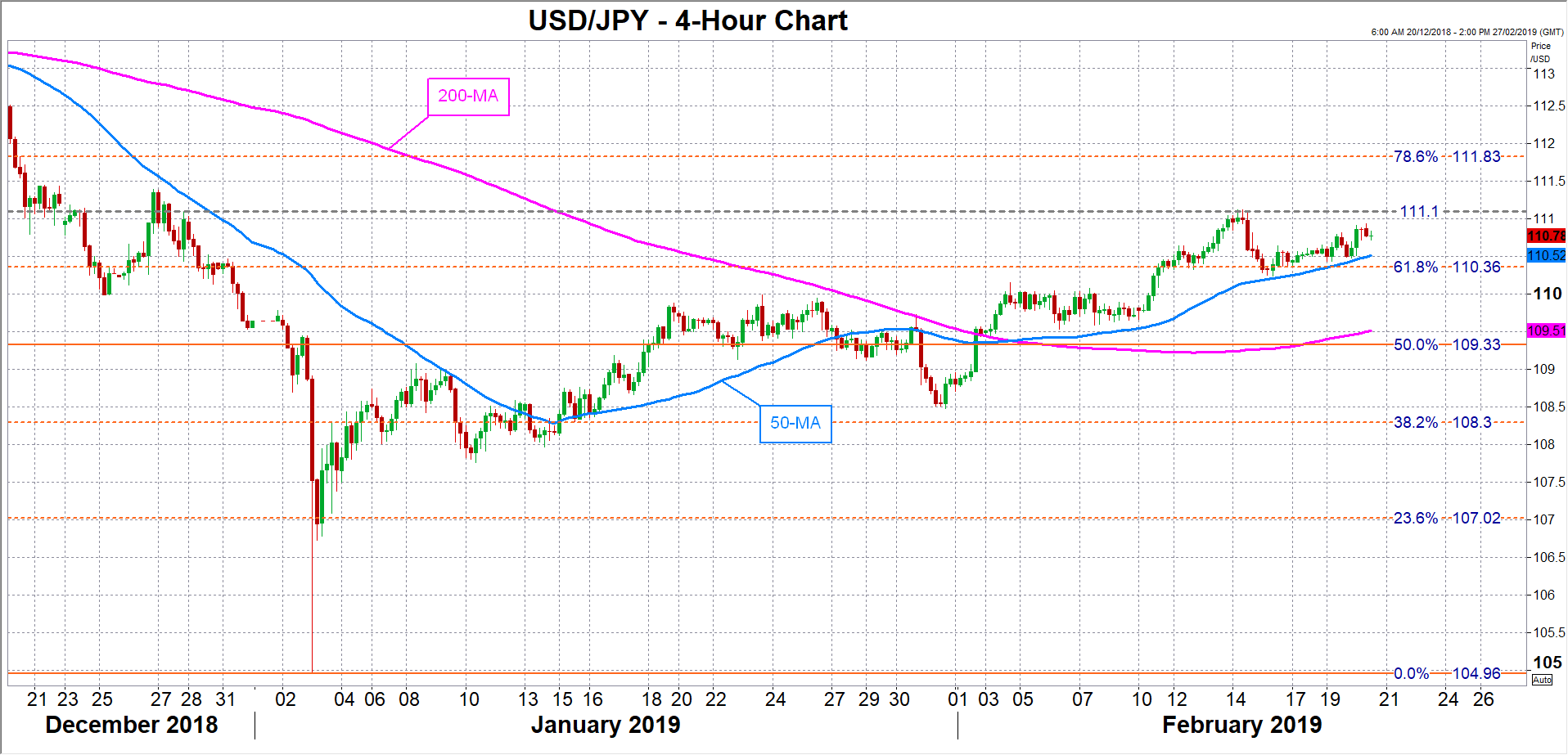

If the data is broadly on the strong side, the dollar could receive a nudge up against the Japanese yen. Dollar/yen could re-challenge the immediate resistance at the 111.10 level, which it failed to break earlier this month. A successful climb above this mark could help the pair clear the next hurdle at the 78.6% Fibonacci retracement of the downleg from 113.7 to 104.96, at 111.83.

If though, Thursday’s numbers point to some weakness in the US economy, dollar/yen could find it difficult to hold above the 50-period moving average (MA) in the 4-hour chart, which has been acting as support over the past week. Not too far below the 50-period MA (currently around 110.50 is the 61.8% Fibonacci, at 110.36. If this support also fails, the pair could stumble towards the 50% Fibonacci at 109.33.

{kind=link}