Wednesday April 24: Five things the markets are talking about

European and Asian equites are/have been under pressure this Wednesday morning, while U.S stocks are pointing to a nondescript open, one day after a new registered record close. U.S Treasuries are climbing, and the dollar is slowly extending its rally to a six-week high.

Note: Both the S&P 500 index and the Nasdaq posted record closing highs yesterday after a plethora of better-than-expected earnings reports eased investor concerns about a U.S economic slowdown.

Elsewhere, sterling is coming under renewed pressure as U.K PM Theresa May is expected to push hard to get some sort of a Brexit deal through Parliament by the end of this month, while emerging-market and oil pegged currencies are on the back foot after a few sessions of gains.

On the Sino-U.S trade front, Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin announced yesterday that they will travel to Beijing for trade talks beginning on April 30.

On tap this week: Stateside, Amazon, Facebook, Twitter, Microsoft and Tesla report earning’s this week. In Europe, bank earnings from Deutsche Bank, UBS, Barclays, Credit Suisse and Swedbank. On the monetary policy front, the Bank of Japan (BoJ), Bank of Canada (BoC) and Sweden’s Riksbank (April 24) set monetary policy. Japan’s Shinzo Abe will meet EU leaders Thursday before flying to the U.S for a summit with Trump. On Friday, advanced U.S GDP should keep markets busy.

1. Stocks lose some of their luster

In Japan, the Nikkei edged lower in choppy trade overnight as investors remain cautious during earnings season, but the index remained atop of its five-month high as sentiment remains somewhat supported by a rally in equities stateside. The Nikkei share average ended -0.3% lower, while the broader Topix dropped -0.7%. With a number of earnings reports due out at the end of the week, don’t expect investors to be taking on large positions ahead of Japan’s 10-day Golden Week holiday starting this weekend.

Down-under, Aussie stocks ended at a 12-year high overnight with banking and healthcare stocks leading the gains, as weak CPI data (+0.3% vs. +0.4% q/q) this week supported the prospects of a Reserve Bank of Australia (RBA) interest rate cut as early as next month. The S&P/ASX 200 index rallied +1% – the benchmark also gained +1% on Tuesday. In S. Korea, the Kospi stock index fell -0.88% overnight as fragile corporate earnings and a weakening currency weighed on the market. KRW lost -0.8% outright overnight.

In China, stocks rallied a tad, recouping early losses, supported by a late rally in tech shares that seems to have offset investor concerns that the PBoC could scale back the scope of further policy easing. At the close, the blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index gained +0.1%. In contrast, in Hong Kong, stocks came under pressure. The Hang Seng index fell -0.5%, while the China Enterprises index lost -0.6%.

In Europe, regional bourses trade mostly lower tracking lower U.S futures and mixed Asian Indices as German IFO missed forecasts (see below).

U.S stocks are set to open in the ‘red’ (-0.7%).

Indices: Stoxx600 -0.04% at 391.20, FTSE -0.40% at 7,493.25, DAX +0.40% at 12,284.39, CAC-40 -0.17% at 5,582.31, IBEX-35 -0.36% at 9,492.85, FTSE MIB -0.37% at 21,815.50, SMI +0.42% at 9,675.50, S&P 500 Futures -0.07%

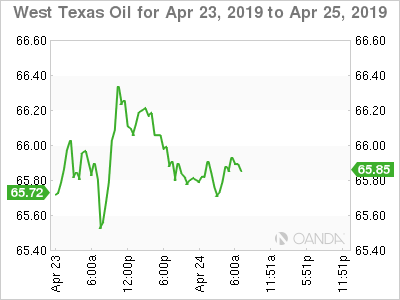

2. Oil falls from six-month high on signs market not tight enough

Oil prices are under pressure this morning on a report that seems to be easing market worries about tightening supply. It has temporarily put an end to this recent rally that has taken prices to their highest level since Q4 2019, driven by OPEC+ output cuts and sanctions.

Brent crude futures are at +$74.18 per barrel, down -33c from Tuesday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$65.89 per barrel, down -41c from their previous settlement.

Putting pressure on the ‘black stuff’ was the IEA statement yesterday indicating that markets are “adequately supplied” and that “global spare production capacity remains at comfortable levels.”

Also weighing on prices was data from the API last week showing that U.S. crude stocks rose by +6.9M barrels last week, more than expected. Expect dealers to take direction from today’s EIA stock data due at 10:30 am EDT.

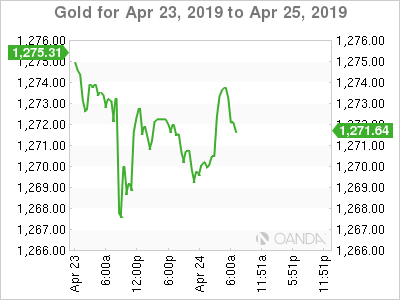

Ahead of the U.S open, gold prices have eased, but remain atop of their four-month low print from yesterday as the ‘big’ dollar remains strong. Spot gold has fallen -0.1% to +$1,270.40 per ounce, having hit its lowest since the end of 2018 at +$1,265.90 on Tuesday. U.S gold futures are -0.1% lower at +$1,272.50 an ounce.

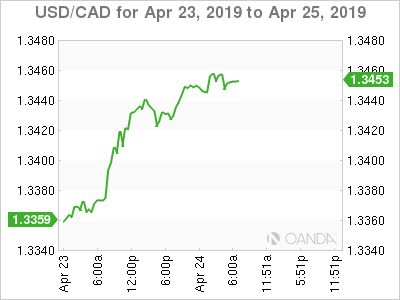

3. Bank of Canada (BoC) to remain on hold

The Bank of Canada (BoC) is expected to keep its key interest rate on hold for the remainder of this year later this morning (10:00 am EDT). Governor Poloz and company are expected to stand pat, leaving the benchmark overnight rate at +1.75%. Dealer consensus is not pricing in another rate change before the end of 2019, as policy makers assess the impacts of ongoing trade tensions and a weaker outlook for domestic growth.

Expect all eyes will be on the accompanying statement, updated forecasts, and Governor Poloz’s tone. Markets seem to be expecting an overly ‘dovish; message, and while the Bank is indeed likely to appear cautious overall, it is unlikely to go as far as abandon its rate-hike plans completely. Currently, the loonie (C$1.3450) is getting very little love from eight-month high oil prices.

Elsewhere, the yield on 10-year Treasuries have fallen -1 bps to +2.55%, the lowest in a fortnight. In Germany, the 10-year Bund yield has dipped -1 bps to +0.03%, while in the U.K the 10-year Gilt yield has fallen -2 bps to +1.204%.

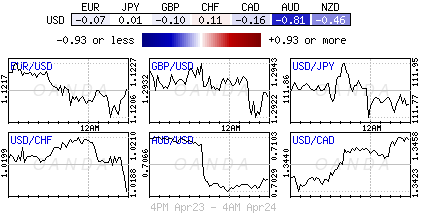

4. Dollar remains the dominant force

The dollar index has jumped another +0.3% in the overnight session to its highest print in nearly two months.

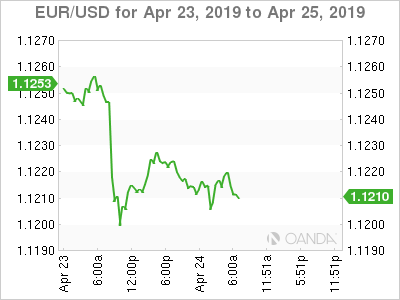

EUR/USD (€1.1213) briefly tested below the psychological €1.12 level (€1.11945) in the aftermath of disappointing German IFO data (see below) which missed expectations across the board as the domestic economy continued to lose steam. Nevertheless, the pair failed to make a fresh new three-week low and has since retraced to above €1.1210.

USD/JPY (¥111.87) is still unable to break above the key ¥112 level with focus remaining on the upcoming Bank of Japan (BoJ) rate decision later this evening.

Overnight, Aussie Q1 CPI data missed expectations and registered its third consecutive reading below the RBA’s target range of +2-3% and matched the lowest level since Q3 2016 (Q/Q: +0.0% vs. +0.2%e; Y/Y: +1.3% vs. +1.5%e). The softer data has a number of analysts revising their outlook for the RBA and now expect a rate cut as soon as next month (A$0.7043).

5. German IFO survey continues the string of disappointing data for region

Data this morning showed that German business sentiment deteriorated somewhat this month as the mood among manufacturers “worsened markedly,” accordingly to the Ifo Institute.

“The German economy continues to lose steam,” said Ifo president Clemens Fuest, after the Ifo business-climate index unexpectedly slipped to 99.2 from a revised 99.7 points in March.

Market expectations were looking for a small increase to 99.9 or 100 for this month.

Note: The German economy has had a weak start to 2019, narrowly avoiding recession in H2 2018, a trend that prompted the government last week to slash its growth forecast for this year to +0.5% from an earlier estimate of +1.0%.

The ZEW research institute’s latest measure of economic expectations, point to towards a “mild pickup” in economic activity in the coming months.

Net, the Ifo survey confirms that “the export-driven industry is in recession, while the domestic economy remains rather healthy.”

{kind=link}