The next highlight for the dollar will be the release of US durable goods orders for April, on Friday at 12:30 GMT. Forecasts point to a soft set of data, possibly due to weakness in demand for commercial aircraft. While a disappointment may hurt the dollar on the news, the broader outlook for the greenback remains positive as long as other major currencies continue to lack appeal.

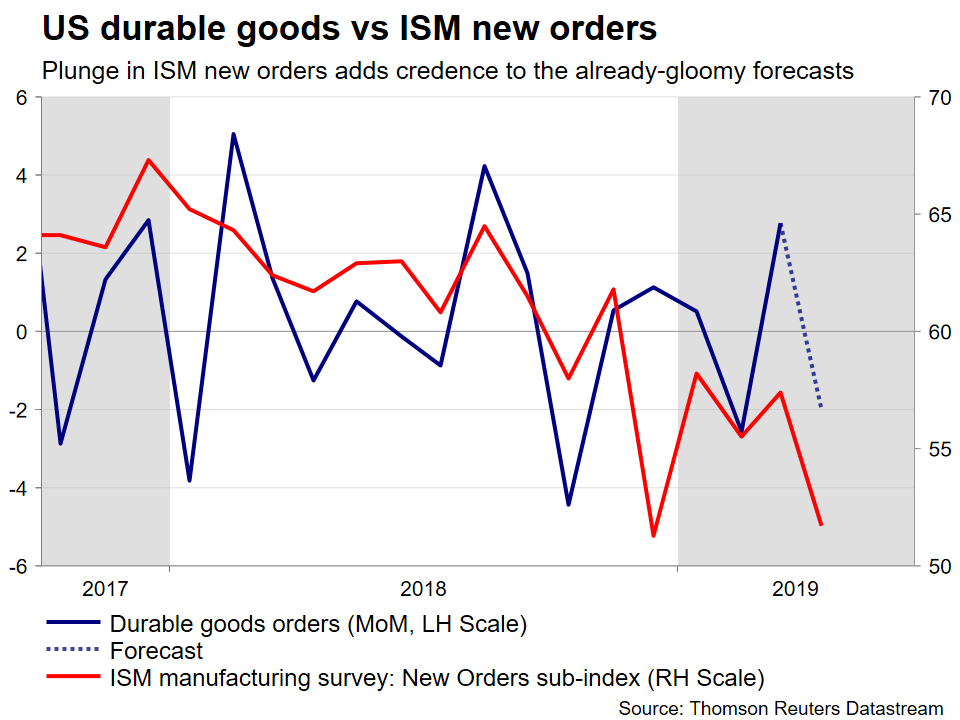

New orders for durable goods are forecast to have contracted by 2.0% on a monthly basis in April, following a 2.8% rise in March. The softness seems largely owed to lackluster demand for transportation equipment, considering that the core figure – which excludes that item category – is projected to have risen by a modest 0.2%, the same pace as in March.

Indeed, US aircraft-maker Boeing reported zero new orders in April for its jets, as the recent scandal with its 737 MAX model kept buyers away, which explains much of the anticipated weakness in the headline print. Adding further credence to the pessimistic forecasts, the new orders sub-index of the ISM manufacturing PMI plunged in April, indicating that orders to manufacturers increased at a much slower pace. In isolation, this may even imply a weaker-than-expected data set.

If the actual prints come in as expected, or weaker, that may signal that capital investment remained fairly soft to start Q2, raising concerns about broader economic growth. Expectations on that front are already quite subdued, with the Atlanta Fed GDPNow model signaling a sluggish 1.2% annualized growth rate in Q2, with the data available so far.

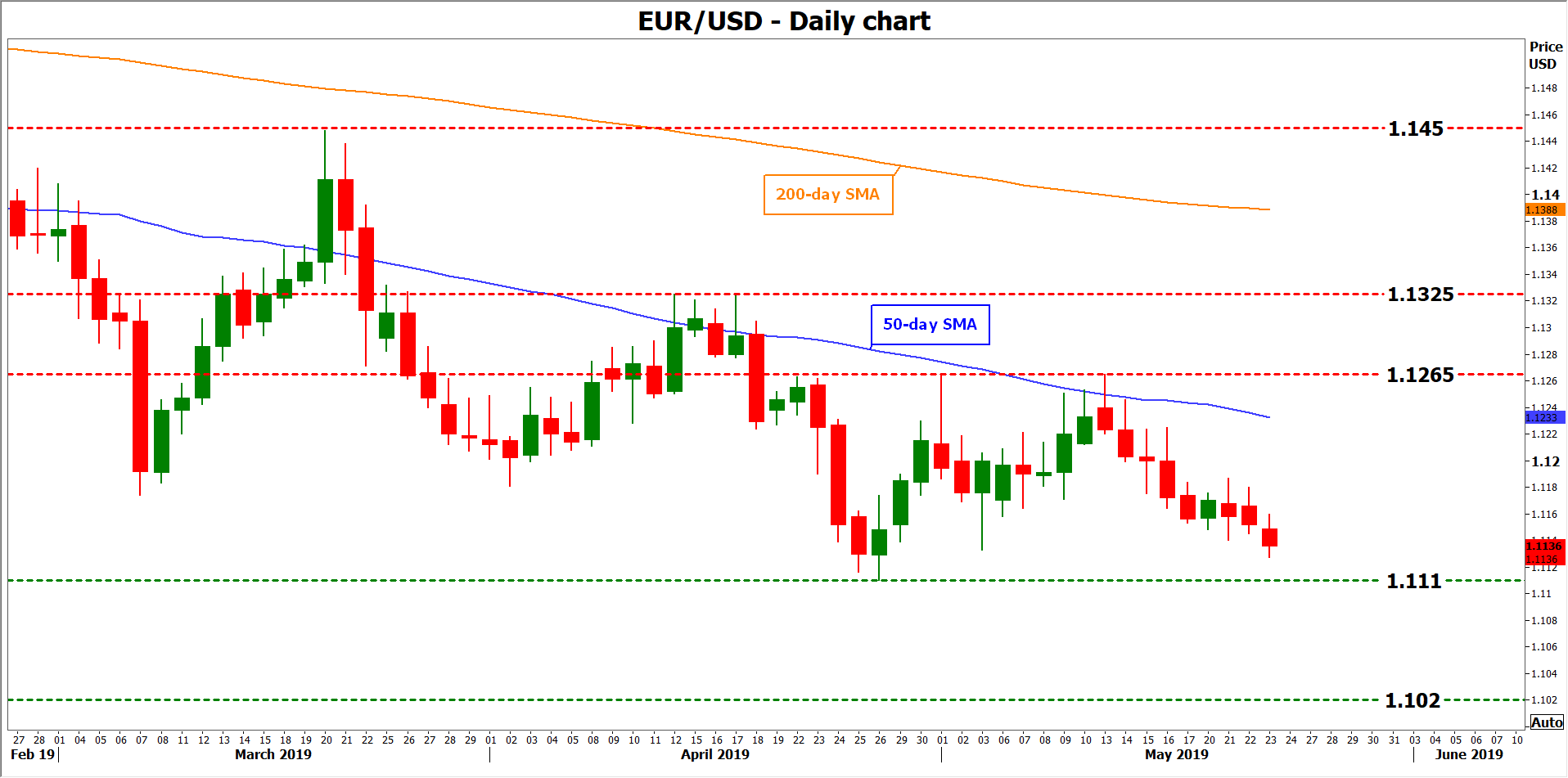

In case of a disappointment, the dollar could come under some selling pressure as expectations for a Fed rate cut this year grow further. Looking at euro/dollar technically, resistance to advances may be found near the 50-day SMA at 1.1236, with an upside break opening the way for 1.1265.

On the other hand, if durables surprise to the upside, the greenback may gain ground as rate-cut bets are unwound. Support to declines in euro/dollar could come at 1.1140, with a bearish violation turning the attention to the 2-year low of 1.1110.

In the big picture, what matters most for the dollar probably lies beyond US borders. The greenback remains the ‘king’ of the FX market for now, mainly due to other major currencies – like the euro, pound, aussie and kiwi – being unattractive. Make no mistake, this is mostly a story about global weakness driving investors to the US, as opposed to the US attracting capital flows purely on its own merits.

Therefore, the outlook for the dollar remains positive, until one of the bleak narratives in the other major economies starts to improve. In this sense, the biggest downside risk for the dollar would be a material rebound in European growth, which as the latest European PMIs showed, is not there yet.

{kind=link}