- All eyes on Fed – Powell may have trouble satisfying the bears

- Euro cruises lower as Draghi signals more stimulus

- Stocks roar higher as Trump-Xi agree to meet at G20

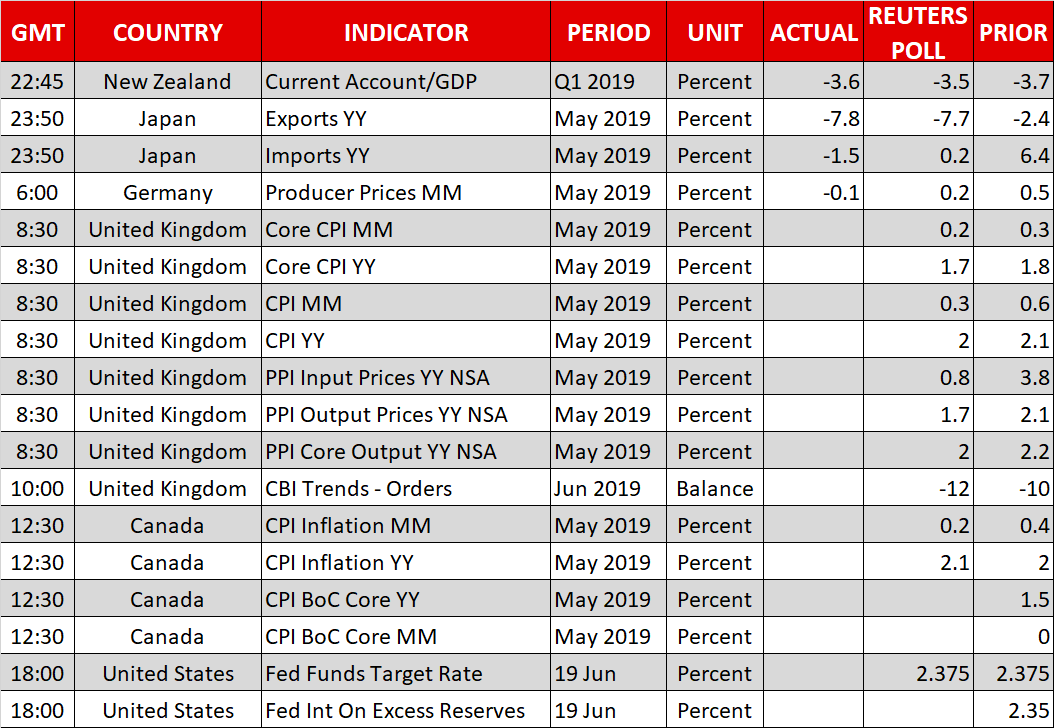

- UK & Canadian inflation data coming up

Fed meeting: Dovish, but enough to appease the market?

The main event today will be the Fed policy decision at 18:00 GMT, followed by a press conference from Chairman Powell half an hour later. A more dovish tone seems almost certain in light of the sharp decline in US inflation expectations and an overall slowing data pulse, coupled with the ongoing trade uncertainty.

The question however, is whether any signals for rate cuts will be enough to live up to the market’s already-dovish expectations, given that two rate cuts are fully priced in for July and October. In other words, much easing is factored into the greenback and equities by now, so anything short of explicit comments for aggressive cuts very soon could trigger a hawkish reaction, sending the dollar a little higher and stocks lower on the news.

Having said that, the broader picture for the dollar is increasingly becoming gloomier, hence even a positive reaction on the Fed today may remain relatively short-lived. Both the Fed and the ECB appear ready to enter an easing cycle in which the Fed will have a lot more room to cut than the ECB does, implying that the potential downside in the dollar would likely be more severe, other things equal.

Euro stumbles as Draghi opens door for more stimulus

In classic fashion, the ECB chief pushed the euro a little lower yesterday, by affirming that more stimulus will likely be needed. Yet, the market reaction was not as large as one would have expected given the gravitas of such an announcement, with the single currency even recovering some of its losses in the following hours.

This highlights that markets think the ECB’s ‘ammunition box’ is limited, as the margin to cut rates further into negative territory is small, and the appetite for restarting QE within the central bank seems even smaller. To be clear, any losses in the euro from further ECB easing are unlikely to be massive, absent a ‘shock’ reintroduction of QE.

Risk sentiment lifted by fresh hopes for trade deal

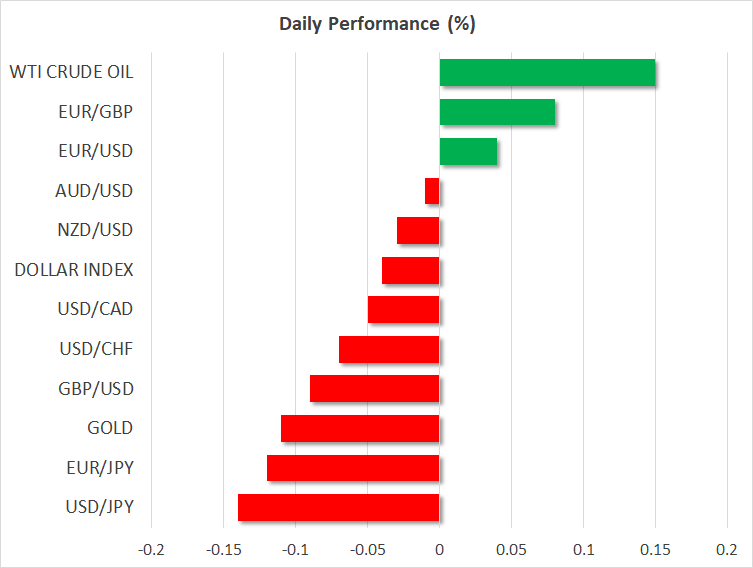

In the broader market, risk appetite improved following news that the American and Chinese presidents spoke on the phone, and that they’ll meet in person at the G20 summit next week in an attempt to break the trade deadlock. Global stocks rejoiced, with the likes of the S&P 500 (+0.97%) and Dow Jones (+1.35%) approaching their all-time highs again, also aided by ECB stimulus hopes. Likewise, commodity currencies such as the aussie, kiwi, and loonie soared – the latter pushed up by rising oil prices too.

UK & Canadian inflation on tap, more Tory leadership votes

Besides the Fed meeting, traders will also be on the lookout for May inflation figures from both the UK and Canada today.

The Canadian prints could prove crucial as forecasts point to a solid set of data, which may underscore that Fed-BoC policies are set to diverge, and thereby lift the loonie.

In the UK, the pound tends to overlook economic data, and the focus may instead be on yet another round of voting in the Conservative leadership race, which Boris Johnson is still leading by a huge margin.

{kind=link}