Quiet end to the week

It may be a relatively quiet end to the week as traders digest the last two days of Powell’s testimony and US data and weigh up the prospects for interest rates this year.

Powell’s appearance Wednesday was extremely well received, with the Fed Chairman giving us as dovish a message as he was ever likely to. There was no attempt to discourage investors from fully pricing in a July cut so that looks as close to a certainty as you can expect to see.

Investors appear encouraged that it won’t be the last as well, with his gloomier assessment of the outlook appearing an indication of future cuts. The CPI numbers on Thursday added a layer of confusion, as weak price pressures are one of the primary factors supporting calls for cuts.

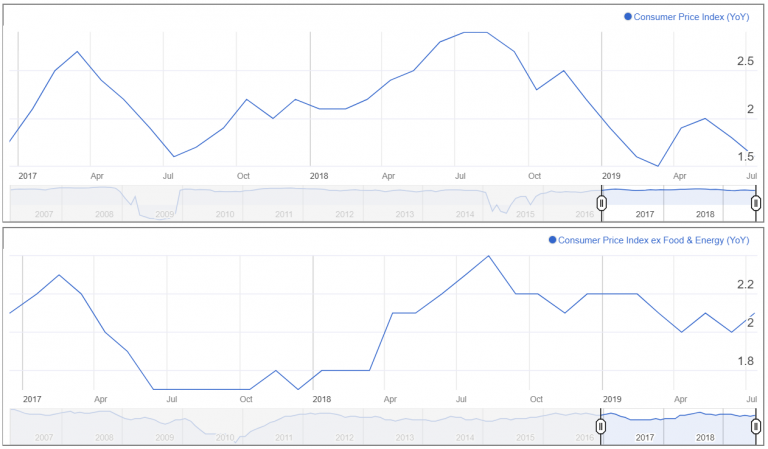

US Inflation (CPI and Core CPI)

A core annual inflation reading of 2.1% may well leave people wondering whether inflation is as lacking as Powell indicated and the Fed’s preferred PCE measure suggests.

Stocks ended the day higher on Thursday and Europe is slightly in positive territory at the open but the data yesterday did take some of the wind out of the sails.

This may put more emphasis on the PPI data today but broadly speaking it’s looking a little thin. Thankfully, Monday marks the start of earnings season so we won’t have to wait long for something to get our teeth into.