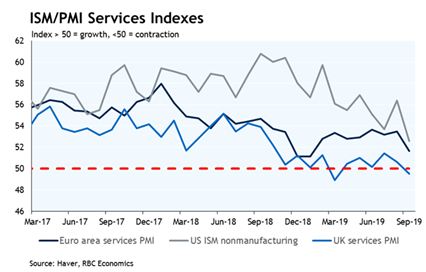

A week ago we noted divergence between the goods and services sectors has become a key theme for many countries. Industrial activity has been (predictably) soft in the wake of escalating US-China trade tensions and Brexit uncertainty in Europe. The question has been more whether the much larger services side of the economy will follow manufacturing lower – and by how much. Against that backdrop, a big pullback in the US non-manufacturing ISM index in September, along with a similar deterioration in services PMI measures in the Euro area and the UK – understandably raised questions about just how resilient the service sector can be, particularly given manufacturing indicators have continued to soften.

Still, deterioration to-date has been more widespread in ‘soft’ survey indicators that can be impacted by negative sentiment than in ‘hard’ economic data. September’s US employment report was broadly better than feared in the wake of earlier ISM data. Employment growth has clearly slowed from outsized gains in earlier years, but to-date there is little evidence that layoffs are increasing. The US unemployment rate hit a new cycle-low. Household income growth still looks solid and borrowing costs have fallen. That should still support the over 70% of the US economy accounted for by household spending. Of course, there is also always an outside risk that trade tensions ease. Indeed, a selloff in equity markets and/or more significant softening in labour markets in the politically important US industrial heartland states could potentially prompt an about-face from a presidential administration that can ill-afford a decline in approval ratings. Markets will remain concerned about recession storm clouds forming off-shore, but to-date we still think the most likely base-case is it won’t ultimately make landfall.

Canada has, somewhat surprisingly, held up relatively well. Canadian manufacturing numbers have also looked soft, but not as soft as in other regions. Net trade data still looks uninspiring, but are not yet flagging a dramatic pullback in external demand. Housing markets have improved alongside lower interest rates and still-solid labour market numbers. We expect housing starts remained strong in September. But as a small open economy, external growth headwinds will ultimately spill over more significantly into the Canadian industrial sector. Like elsewhere, the net impact on the economy will depend on how weak the manufacturing sector might get – and how resilient the service-sector remains. On that front, next week’s September Canadian employment numbers will be watched closely for signs that household demand growth will be supported going forward.