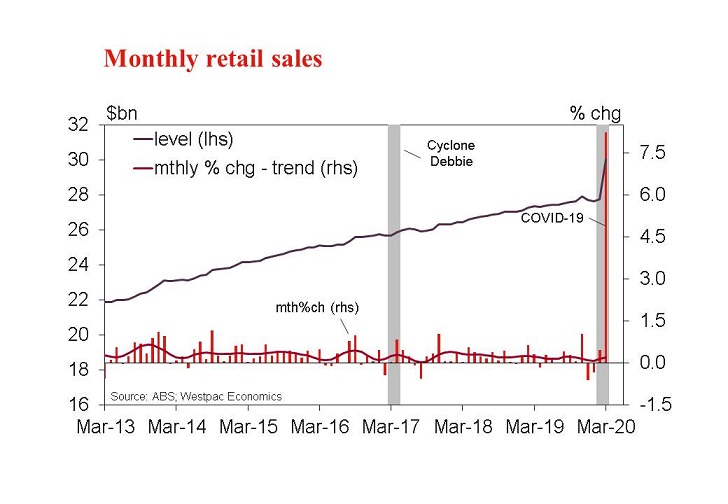

Mar prelim sales: +8.2%mth, +9.9%yr. Spectacular stockpiling surge offsets initial virus hit to exposed segments.

The ABS has released a preliminary estimate for March retail sales showing a huge 8.2% rise in the month as a spectacular stockpiling-driven surge in segments like basic food more than offset weakness in segment hit hard by the Coronavirus shutdown.

Note that this release is part of an effort to provide more timely information on the impacts of the Coronavirus. Preliminary figures are based on returns covering 80% of the sector but are subject to revision once final survey estimates are released on May 6. This release will also include more detailed figures by sub-category, sales channel, state and business size and a wash-up for Q1 as a whole including estimates for real retail sales (i.e. ‘volumes’) that remove the effect of price changes.

Recall that retail was coming off a mixed run, posting a 0.5% gain in Feb after back to back declines in Jan (–0.3%) and Dec (–0.6%) that was largely an unwind of a 1% gain in Nov that was a pull-forward associated with the Black Friday event.

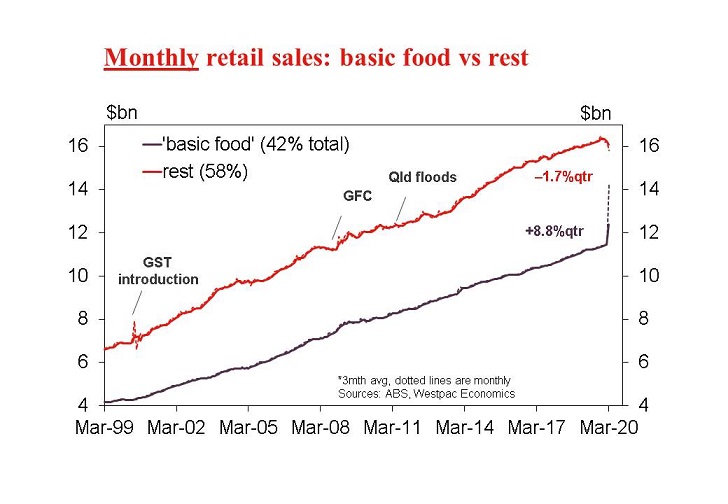

The Feb gain was anchored by a solid 0.8%mth lift in basic food that looked to be an early effect from ‘stock-piling’ demand as consumers prepared for tightening restrictions on movement. That effect became ‘parabolic’ in March with a phenomenal 23.5% surge in basic food retail in the month. Toilet paper, tissue paper, flour, rice and pasta sales all reportedly doubled month to month. The stockpiling rush reportedly levelled out over the second half of the month and the ‘catered’ and non food retail segments reportedly recorded big falls but clearly not enough to counter the big gain in the large ‘basic food’ segment (worth 42% of total retail sales).

To put this into perspective, the monthly rise in basic food retail in March was more than four times larger than the next biggest monthly rise recorded in history – a 5.8% jump around the time the AUD was being floated and when basic food retail price inflation was running at 5-6%yr.

While the preliminary release does not provide the full sub-category information, the detail provided does allow us to estimate retail sales excluding this basic food component – overall, sales in this combined segment declined 2.6%mth to be down 1.8%yr – the biggest monthly decline since 1989 (excluding the wild swings around the GST introduction in July 2000, noting that basic food products were GST exempt and unaffected by these variations).

Overall, the update is clearly interesting but does not provide much guidance for assessing the economic impact of the virus on the wider economy. The impact of a bigger stockpiling boost to Q1 consumption for example is likely to be counterbalanced in GDP growth terms by a rundown in inventories and an influx of imports, all of which will likely see bigger corresponding pull backs in Q2. As such, the main message is that March marked the beginning of what will clearly be some wild swings in the domestic economy moving in several different directions

{kind=link}