Sunrise Market Commentary

- Rates: Fed’s expected message largely discounted?

We expect the Fed to keep its policy unchanged tonight. Announcing the start of balance sheet tapering is a wildcard, but September might be the better fit. Subdued inflation could get more attention, but shouldn’t keep the Fed from hiking its policy rate one more time this year. Such message should be rather neutral for markets and by and large discounted. - Currencies: Dollar decline slows going into the FOMC decision

The dollar traded volatile yesterday, but finally rebounded on a rise in US yields. Today, focus turns to the Fed’s policy statement. The Fed will probably show its concern in the recent easing in inflation. However, the dollar already discounts quite some bad news. Is the time ripe for some USD bottoming?

The Sunrise Headlines

- Wall Street trading ended positive yesterday, supported by strong earnings figures. Overnight, Asian equities are trading more mixed with China and Korea in the red. US Treasuries stabilize ahead of the FOMC outcome later today.

- The Australian inflation increased by 0.2% Q/Q (1.9% Y/Y) in Q2, less than the expected 0.4% Q/Q (2.2% Y/Y). RBA chief Lowe said moves of other central banks to withdraw stimulus “has no automatic implications” for RBA policy.

- The US Senate rejected McConnell’s health proposal at the start of several days of debate. The Senate will now vote on an amendment similar to a 2015 repeal bill passed by the Senate and vetoed by Obama. The vote is expected to fail.

- The IMF warns for significant downside risks to the EMU’s economic outlook and urges the ECB to keep stimulus in place amid weak price pressures. ECB’s Nowotny added the ECB shouldn’t set a timetable for ending its bond purchases.

- Oil extended gains from the highest close in seven weeks as industry data showed U.S. crude stockpiles plunged, easing a glut. The Brent oil price is now around $50.60/barrel.

- The US House of Representatives overwhelmingly passed legislation to impose new sanctions on Russia, North Korea and Iran. The bill imposes new sanctions on Russia in response to the alleged meddling in the 2016 US election.

- The main event on the eco-calendar is the Fed FOMC meeting. Will the FOMC announce the starting date of the balance sheet tapering? The first estimate of the UK GDP for Q2 is the only data of importance

Currencies: Dollar Decline Slows Going Into The FOMC Decision

Fed statement a tipping point for the dollar?

The dollar traded volatile yesterday, but finally rebounded. A rise in core (US & EMU) yields supported USD/JPY. In US dealings, EUR/USD jumped temporary above 1.17, but a real test of the 1.1714/35 resistance didn’t occur. A further rise in US yields after strong consumer confidence finally tilted the balance in favour of the dollar. The start of the debate on Obamacare was maybe also a minor support for the dollar. EUR/USD closed the session little changed at 1.1647. USD/JPY ended the session at 111.89, well off the sub-111 levels traded earlier in the session.

Asian equities trade mixed to slightly lower overnight. Japan and Australia outperform on a decline of their currencies. USD/JPY maintains yesterday’s gain and trades just below 112. The rise of the oil price and of other commodities supports (US) yields and indirectly the dollar. The Aussie dollar doesn’t profit from higher commodities. On the contrary, AUD/USD returned to the 0.79 area. Australian headline inflation unexpectedly dropped from 2.1% Y/Y tot 1.9% Y/Y (2.2% Y/Y expected). RBA governor Lowe also hinted that the RBA shouldn’t join the tightening from other central banks. EUR/USD trades around 1.1635. The dollar maintains yesterday’s rebound against the euro.

Markets will keep their focus on the Fed’s policy statement this evening (see above for analysis). The Fed will keep its policy rate unchanged. Markets will closely monitor the central bank’s assessment on the recent softer inflation data. We expect the Fed to be more concerned on inflation, but to keep the door open for a December rate hike. The FOMC might give more information on the start of the balance sheet tapering, even as an announcement in September is most likely. The market implied probability of a December rate hike is currently less than 50%. We don’t expect to Fed to be that soft that markets reduce expectations further. If (ST) US interest rates bottom, one might assume that there is also quite some negative news discounted for the dollar. Especially USD/JPY might find some support if US rates bottom out. The story for EUR/USD is different as markets ponder the next steps of ECB policy normalisation to be announced in autumn. The jury is still out, but yesterday’s price action of the dollar overall and of EUR/USD in particular suggests the dollar decline has already gone quite far. There is more really good US eco news needed to trigger a sustained USD rebound. However, assuming that the Fed statement won’t be overly soft, we expect no sustained break of the key 1.1714/35 resistance already now

USD: technical picture remains fragile, but …

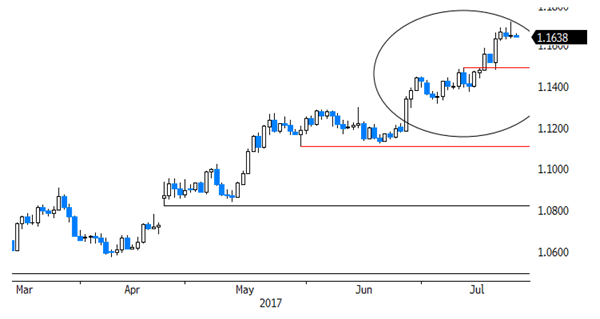

EUR/USD rebounded above the 1.1300/66 resistance at the end of June. Recent US data were not good enough to trigger a sustained USD rebound. Finally EUR/USD broke beyond a first important resistance at 1.1489/1.15, paving the way to the LT-correction tops at 1.1616/1.1714. A sustained break would end the long consolidation that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area is not easy to break. We don’t preposition for a break, but the pressure is mounting. Return action below 1.13 would be a first indication of a loss in upside momentum.

USD/JPY rebounded in the 108.13/114.37 range after the June 14 Fed meeting. The pair regained interim resistance at 112.13, but follow-through gains remained modest. USD/JPY 114.37 resistance was tested, but rejected. The pair drifted lower in the broader consolidation pattern between 114.50 and 108.83/13. Yesterday, this correction halted. The jury is still out, but a short-term test/break of the key 108.83/13 support is becoming less likely. We look out whether the bottoming out process will be confirmed after the Fed decision/statement.

EUR/USD: top MT consolidation pattern under heavy strain, but no break yet

EUR/GBP

UK Q1 GDP data in focus for sterling trading

Sterling showed no clear directional trend yesyterday. EUR/GBP hovered in the mid 0.89 area, stabilizing within reach of the recent low against the euro (EUR/GBP 0.8994). Cable initially rebounded on USD softness but declined as the USD staged a comeback later in the session. UK eco data/stories were mixed and had no lasting impact on sterling trading. EUR/GBP closed the session little changed at 0.8943. Cable finished the session at 1.3025.

Today, the first estimate of the UK Q1 GDP will be published. UK growth is expected at 0.3% Q/Q and 1.7% Y/Y (0.2% Q/Q and 2.0% Y/Y in Q1). We don’t have strong arguments to take a different view from the consensus. A figure in line with consensus (or softer) is probably enough for the BoE to maintain its waitand- see approach at next week’s BoE meeting. In theory, this might be slightly negative for sterling. That said, before EUR/GBP make further progress beyond 0.90, a further rise of EUR/USD is probably needed. Assuming that the Fed won’t be overly soft this evening, a sustained break higher for EUR/GBP is currently not that likely.

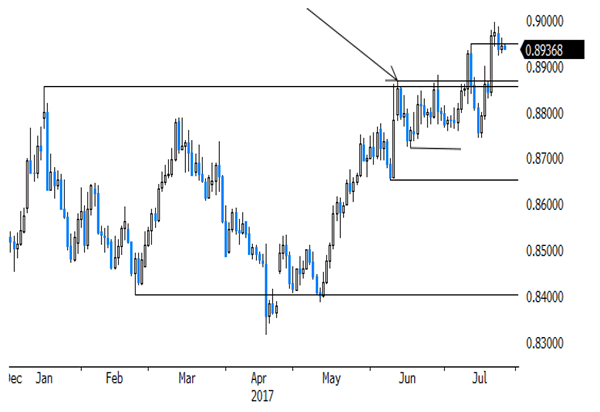

From a technical point of view, EUR/GBP broke above the 0.8854/66 resistance (2017 top) to set a new correction top north of 0.89, but the rally slowed at the end of last week. A break below 0.8720 would suggest that upside momentum is easing. For now, we don’t see a trigger for a sustained rebound of sterling against the euro. We still look to buy EUR/GBP on more pronounced dips. For that to happen, EUR/GBP probably needs some help from a correction in EUR/USD

EUR/GBP: consolidation near recent top