Despite the mention of balance sheet reduction beginning ‘relatively soon’ markets sent the Dollar to fresh lows as they continue to doubt fed’s ability to raise once more this year.

Summary of the July meeting (read full statement)

- The labour market has continued to strengthen and that economic activity has been rising moderately

- Market-based measures of inflation compensation remain low

- Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term

- but to stabilize around the Committee’s 2 percent objective over the medium term.

- Near-term risks to the economic outlook appear roughly balanced

- The stance of monetary policy remains accommodative

- the federal funds rate is likely to remain

The Committee expects to begin implementing its balance sheet normalization program relatively soon

The US Dollar extended declines as the potential for a hike seemed diminished. We thought that was the case going into the meeting anyway as inflation has continued to soften and data overall has been soft. The biggest change to the statement was the point of normalising the balance sheet ‘relatively soon’ which puts the September meeting in full focus for the implementation to take place. Previously it was thought they would reveal plans for the tapering in September, yet they now speak of action. It is therefore possible we’ll hear more details at the Jackson Hole symposium at the end of this month. It remains widely debated as to what effect this will have on markets, although we see it as a form of tightening. Therefor we may see yields move higher if bonds do sell-off although the Fed learned their lesson with the taper tantrum so lots of forward guidance is expected on this subject.

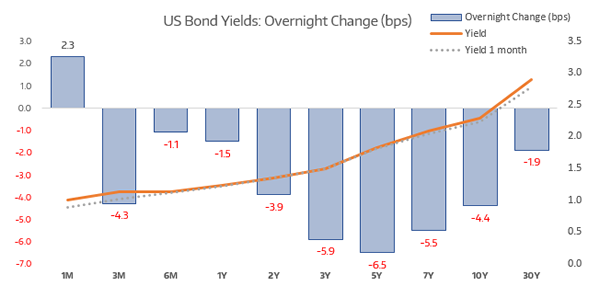

The dovish meeting saw money flow back into bonds which pressured yields from 3 months right through to 30 years decline. It was the centre of the curve which attracted the heaviest flow back into bonds as the 3, 5 and 7-year yields dropped by -5.9, -6.5 and -5.5 bps respectively. With policy remaining accommodative little hope of a raise or even balance sheet reduction soon, yield may continue to come under pressure as bonds remain supported. It is the threat of tightening which weakens bonds as the act is done to fend off inflation (which erodes the value of bonds). If there is no inflation, there is less need to hike and bond markets flourish. With inflation and inflation expectations all pointing lower, yields may indeed come under pressure and the stock market is more likely to continue its bullish trajectory.

The US Dollar Index printed a bearish outside day which provides a prominent swing high at 94.28. We are now firmly below the monthly S2 and the prior low to assume a resumption of the bearish trend. We only expect minor pullbacks from here so we’d consider fading into rallied below monthly S2. This only adds yet further support for EUR, AUD, NZD and the like which continue to rise against their central banks wishes. Unfortunately for the smaller, latter two, they have less sway in the direction of their currency if USD is in freefall.

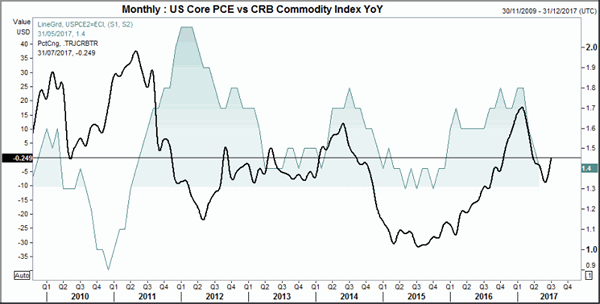

Next week the US release personal consumption expenditures. Whilst it looks at the consumption side of the economy, therefor a measure of consumer confidence and spending, it is the preferred inflationary measure of the Fed. It shares a relationship with commodity prices too, although the correlation between commodities YoY and inflation does vary and go out of syn. Yet since 2012 the correlation has been decent enough to call turning points, which is why we’re highlighting the uplift of the CRB commodity index YoY. This does not necessarily mean we will see an uptick next week but it is possible we’ll see one in the next couple of months or so if the gains on commodities are at least sustained or extended. This seems to be a viable outcome given the extended drop in the US Dollar.