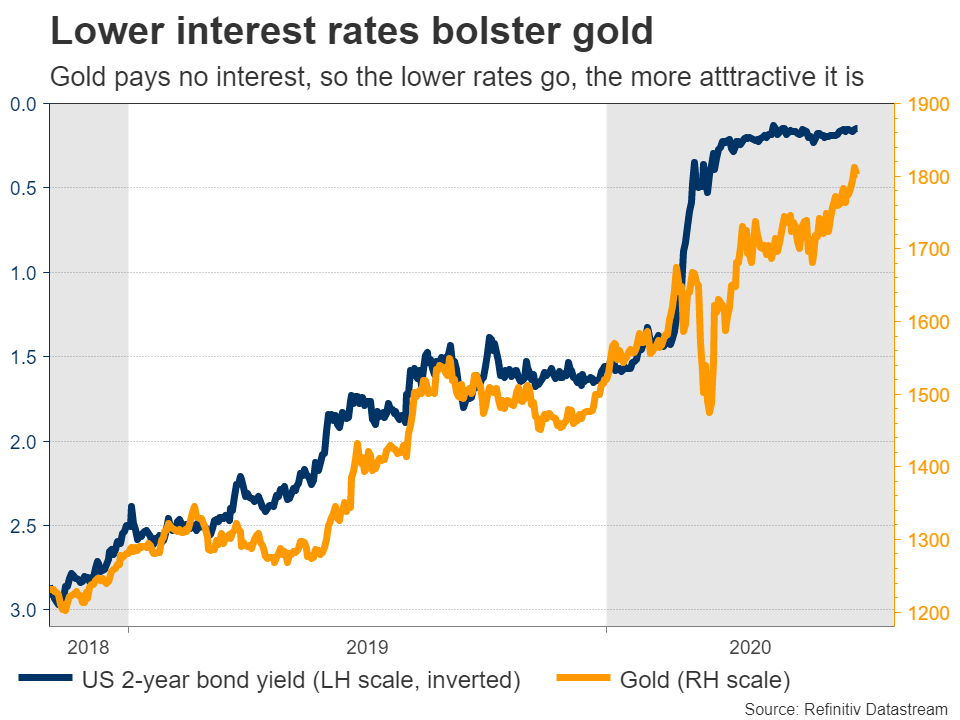

Gold prices keep rising, powered by a trifecta of uncertainty among investors, runaway government spending, and rock bottom interest rates for years to come. Even though the metal has already come a long way, there’s not much to stop it from grinding even higher to new record highs. Any more stimulus from the Fed for instance, like an introduction of yield curve control, could sink the dollar and turbocharge bullion. The main downside risk is a successful virus vaccine. Central banks and fearThe gold train keeps on rolling. Prices crossed above the $1800/ounce region this week for the first time in nine years as investors look for safe havens to hedge their riskier bets, amid mounting concerns around the economic recovery. The resurgence in infections across the globe and especially in the US is threatening to put the breaks on the economy’s comeback, as businesses close again in several states to bring the outbreak under control.It’s not just uncertainty and haven demand though. The primary fuel behind gold’s ascent is interest rates hitting zero or negative around the world, and expectations that central banks will keep them there for a long, long time. Gold pays no interest to hold, so it becomes more attractive compared to interest-bearing assets like bonds the lower rates fall and the longer they stay low.

Consider this: would you buy a German bond that pays negative interest for 10 years, or gold that pays zero? Even American bonds that still pay out positive yields are unattractive, because once you account for inflation over a long period (real rates), they are also negative-yielding.

This is crucial because bonds are the largest asset class in the world, so with central banks making most bonds ‘uninvestable’, fund managers looking for decent returns are forced to find other alternatives. This also explains why stocks have recovered so powerfully.

Debt and geopolitics in the mix too

Then, there’s fiscal policy. Government deficits are exploding due to the massive rescue packages, and higher national debts benefit bullion. A massive spike in debts typically raises concerns about whether governments will meet their obligations, and if so, whether they will do so by debasing fiat currencies.

The final leg of this bullish gold story is geopolitical uncertainty. Tensions between the US and China continue to flare, but beyond that, a more recent development is the clash between Indian and Chinese troops that left dozens dead. While that situation seems to be de-escalating, it’s a very dangerous game, as military skirmishes between two nuclear-armed powers is the last thing the global economy needs.

Can the rally continue?

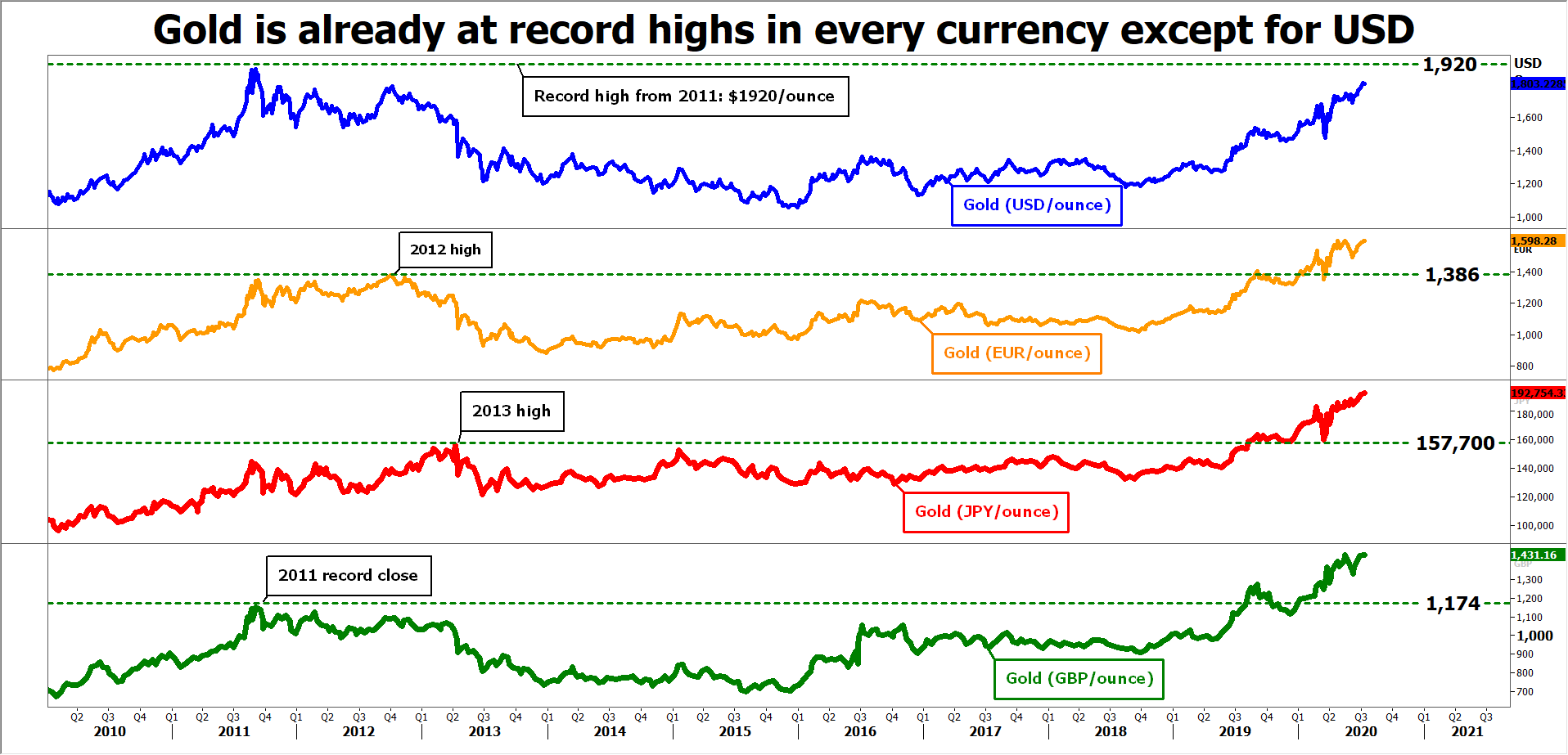

Most definitely. That doesn’t mean there won’t be corrections on the way – nothing goes up in a straight line – but eventually, we might see new all-time highs above the record peak of $1920, maybe much higher.

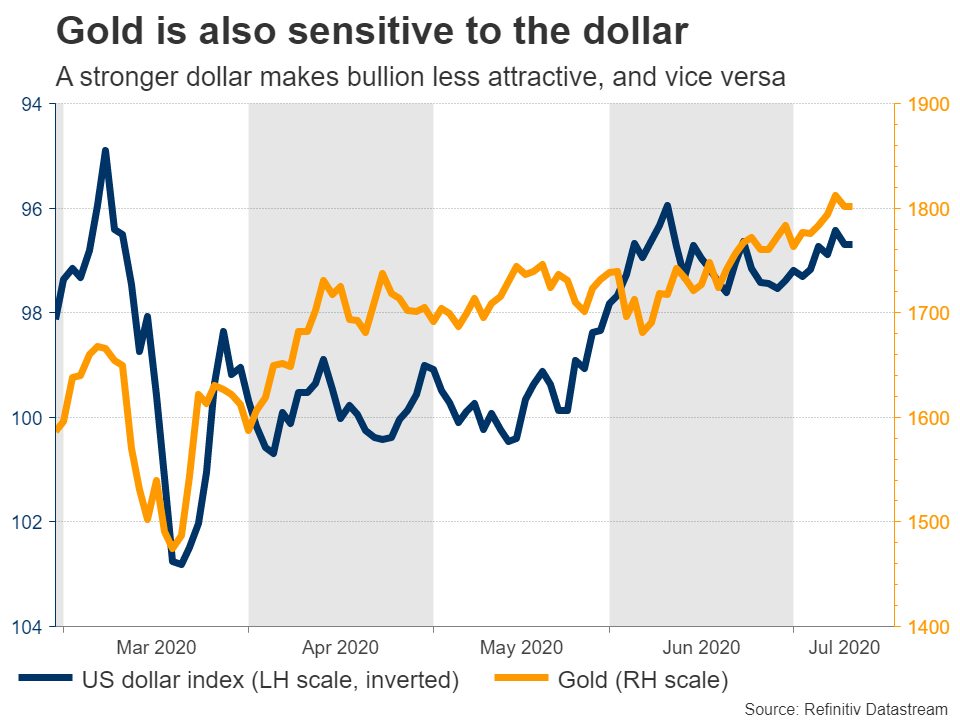

In fact, gold already hit new records this year if measured in any currency other than the dollar. Let’s explain. Since gold contracts are denominated in dollars, bullion and the greenback have an inverse relationship. When the dollar appreciates, it becomes more expensive for investors using foreign currencies to buy gold, putting downward pressure on bullion.

This implies that the dollar’s strength is the main obstacle keeping gold from cruising even higher. Yes, the greenback has fallen a little lately, but it remains quite elevated from a historical perspective. In other words, the missing ingredient that could accelerate gold’s gains is a further drop in the US currency.

Fed playNow in terms of what could ignite such a move, look no further than the Fed. The US central bank has already done a lot to revive the economy, from slashing interest rates to zero, to even buying junk corporate bonds. But this doesn’t mean the Fed is done.

As the spike in virus cases threatens to derail the recovery, the Fed will be under pressure to act again. The next step will probably be to strengthen the forward guidance, for instance by committing not to raise rates until inflation reaches 2.5%. This would send a strong signal that rates will be kept low for many years and would likely push gold higher, not just because of the ‘low rates for longer’ theme but also by hurting the dollar. It could happen as early as this summer.

After that’s done, any further hiccups in the economy might call for more drastic measures. That would be yield curve control, meaning the Fed setting a target for yields on bonds of some maturity, say 3-year Treasuries. This would simply be a more extreme form of committing to low rates for longer.

Now to be clear, the Fed doesn’t want to go down this route, as this policy also carries several risks. For example, it could be very difficult to exit from, and if investors doubt the Fed’s commitment to keeping yields low and start dumping bonds, the central bank might need to buy absurd amounts of Treasuries to keep yields steady.

But that doesn’t mean it won’t happen. It just means the situation has to worsen first, leaving policymakers little choice but to implement it. In fact, the Fed might be forced into this if bond yields spike higher for any reason, tightening financial conditions. If this happens some time later this year, it could sink the dollar and light a fire under gold prices.

What about the risks? There are two key downside risks. The obvious one is a virus vaccine being developed, or at least some effective treatment that leads investors to dump safe assets like gold. Alas, it’s anyone’s guess whether that will happen in a few months, next year, or beyond. Even in this case though, the downside for gold may not be massive, since the other legs of the rally will still be there. Rates won’t rise for many years, and government deficits will likely stay enormous.

The other key risk is the virus situation spiraling out of control, leading to a repeat of the March meltdown where investors dash into the safety of the dollar, hurting gold. But that’s unlikely too. Investors are more familiar with the virus risks by now, so even if the situation worsens, any selloff may be more ‘orderly’ than the panic we saw in March.

In other words, unless a vaccine is found or full-blown panic takes hold of markets again, the path of least resistance for gold is probably higher.

{kind=link}