Monday August 14: Five things the markets are talking about

Last weeks geopolitical worries sent investors scampering for safe havens.

However, the fears of an escalation of tensions between the U.S and North Korea is showing signs of easing this Monday morning as equity markets in Europe follows Asia higher and U.S stock futures are in the black. Gold prices have slipped with U.S Treasuries and the yen.

Nevertheless, the dollar gains seem somewhat capped by the tensions on the Korean peninsula and doubts that the Fed will hike interest rates again this year.

Stateside this week, U.S consumer spending gets things rolling on Tuesday with U.S retail sales (08:30am EDT). The market is looking for it to rebound in ‘moderate’ strength.

From a manufacturing data perspective, there is Tuesday’s Empire state manufacturing index (08:30 am EDT), Thursday’s industrial production (09:15am EDT) and the Philly Fed (08:30am EDT) which all are expected show some moderate strength to keep the market ticking over.

The highlight of the week will be Wednesday’s FOMC minutes from last month’s meeting which produced no action and no hint on when balance sheet unwinding begins.

Friday winds up with August’s consumer sentiment (10:00am EDT), a report that is running well behind its rival consumer confidence report, which has been holding steady at massive highs.

That aside, geopolitical risks are expected to remain a key theme for the global markets in the near term – North Korea celebrates Liberation Day tomorrow to mark the end of Japanese rule.

The market should also be bracing itself for tensions ahead of August 21, when an annual joint U.S-South Korean military exercise is due to begin.

1. Stocks see the light of day

Global equity markets have retraced some of last week’s pullback, as robust Asian corporate earnings and reduced fears of imminent military conflict between the U.S and North Korea lifted buying interest.

In Japan, the Nikkei share average fell -1.0% to a 3-month low following a holiday weekend (Japan markets were closed Friday and investors were basically playing catch up), as North Korean tension drove investors to lighten up on riskier assets. The yen’s gains last week overshadowed data showing Japan’s economic grew at a much stronger pace than expected in Q2 (see below). The broader Topix index finished -1.1% lower.

In South Korea, stocks rebound Monday after ending down for four consecutive sessions on geopolitical fears. The Kospi closed up +0.6%.

Down-under, Australia’s S&P/ASX 200 Index rallied +0.7%, while in Hong Kong, the Hang Seng Index gained +1.3%, while the Shanghai Composite Index rose +0.9%.

In China, stocks closed higher on a tech-fuelled rebound. The blue-chip CSI300 index rose +1.3%, while the Shanghai Composite Index gained +0.9%. Investors were unperturbed by data overnight showing that China’s factory output slowed more than expected last month, while investment and retail sales also disappointed (see below).

In Europe, easing geopolitical concerns is helping support risk sentiment – all sectors are moving higher, lead by financials and automakers. Lower oil prices are not dragging on energy stocks enough to pull them into negative territory.

Note: Tomorrow sees several European markets closed due to a holiday (France, Greece, Poland and Italy).

U.S stocks are set to open deep in the black (+0.6%).

Indices: Stoxx50 1.1% at 3,441, FTSE +0.6% at 7,347, DAX +1.1% at 12,141, CAC-40 +1.0% at 5,110, IBEX-35 +1.2% at 10,409, FTSE MIB +0.9% at 21,556, SMI +1.2% at 8,995, S&P 500 Futures +0.6%

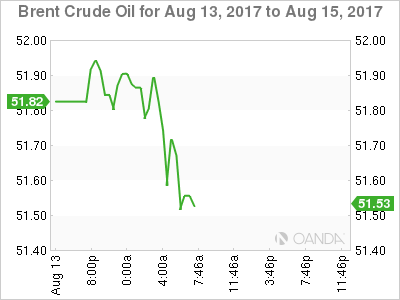

2. Oil prices dip on weak Chinese refining activity, gold lower

Ahead of the U.S open, oil prices are a tad softer as a slowdown in Chinese refining activity growth is casting some market doubts over its crude demand outlook, while rising U.S shale output suggests supplies would likely remain high.

Brent crude futures are at +$51.92 per barrel, down -18c or -0.4% from Friday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$48.70 a barrel, down -12c or -0.3%.

Note: Chinese refineries processed +0.4% more crude oil in July y/y at +45.5m tonnes, or about +10.71m bpd – the lowest amount on a daily basis 10-months.

Despite the possible slowdown in China, the IEA indicated last week it expects 2017 oil demand growth of +1.5m bpd, up from a previous expectation of +1.4m bpd.

On Friday, Baker Hughes energy services firm said U.S drillers’ added 3-rigs looking for new oil in the week to Aug. 11 bringing the total count up to 768, the most since April 2015.

Expect the usual inventory reports from API and EIA to shape the oil futures curve.

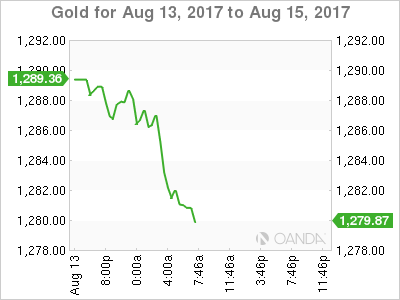

Gold starts the week under pressure (down -0.2% at +$1,286.39 per ounce) as the dollar inches away from last week’s lows, but continues to trade atop of its two-month highs touched last week as the market keeps an eye on developments in the North Korean peninsula.

3. Global yields back away from their recent low

U.S Treasury yields fell further on Friday on the soft U.S. consumer prices data (+0.1% vs. +0.2%e). The 10-year Treasury yield touched +2.182% intraday, its lowest since late June, before pulling back a little to trade +2.204% ahead of this morning’s session.

In Europe, government bond yields have rallied +2-3 bps across the board, bouncing from their recent lows following stronger-than-expected Japanese growth.

Note: Stronger G7 data further supports expectations that the global economy is on the mend and central banks can start to unwind extraordinary monetary stimulus.

The yield on Germany’s 10-year Bunds is up +3.5 bps to +0.42%.

In contrast, Japanese government bond prices mostly edged higher; shrugging off the stronger data to catch up to global market moves after Tokyo markets were closed on Friday. The 10-year cash JGB’s yield inched down -0.5 bps to +0.050%.

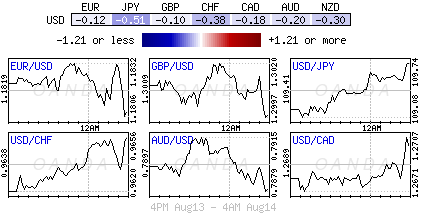

4. Dollar gains some traction

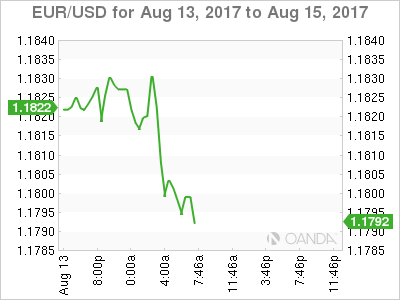

The mighty dollar trades a tad higher this Monday as tensions between the U.S and North Korea calm down a tad. This is keeping the EUR (€1.1800) down outright. However, the market remains a better EUR buyer on dips despite the fact that eurozone June industrial production came in worse-than-expected (see below).

Sterling (£1.2975) has dropped back below the psychological £1.3000 handle. Overall global equity strength has helped the USD/JPY (¥109.70) to strengthen. The pair has rebounded +100 pips from Friday lows.

The People’s Bank of China (PBoC) strengthened the yuan to its strongest setting outright since September 2016. It was a fifth consecutive increase in the daily fix today by the PBoC amid continued dollar softness. The daily trading midpoint was put at ¥6.6601 as authorities try to guide market expectations of a firmer yuan.

5. Japan, China and Eurozone data

Overnight, Japan’s economy grew in the Q2 at the fastest pace in more than two-years as consumer spending and capital expenditure both rose at the fastest in more than three years, highlighting stronger domestic demand. GDP expanded an annualized +4.0% in April-June, more than the median estimate for +2.5%.

In China, July industrial production came in lower than expected at +6.4% vs. +7.1%e – coal and power output all rose; while oil output fell. Other data showed that retail sales were also a bit weaker at +10.4% vs. +10.9%e.

In the Eurozone, industrial production for June was lower than expected, a hint that H2 may be slightly weaker than H1. Eurostat says the output of factories, mines and utilities was -0.6% lower than in May, while up +2.6% from the same month a year earlier. The market was looking for a -0.4% drop.