- US stocks close at new records, oil roars higher, gold melts down

- Markets in an ecstatic mood, without any major new drivers

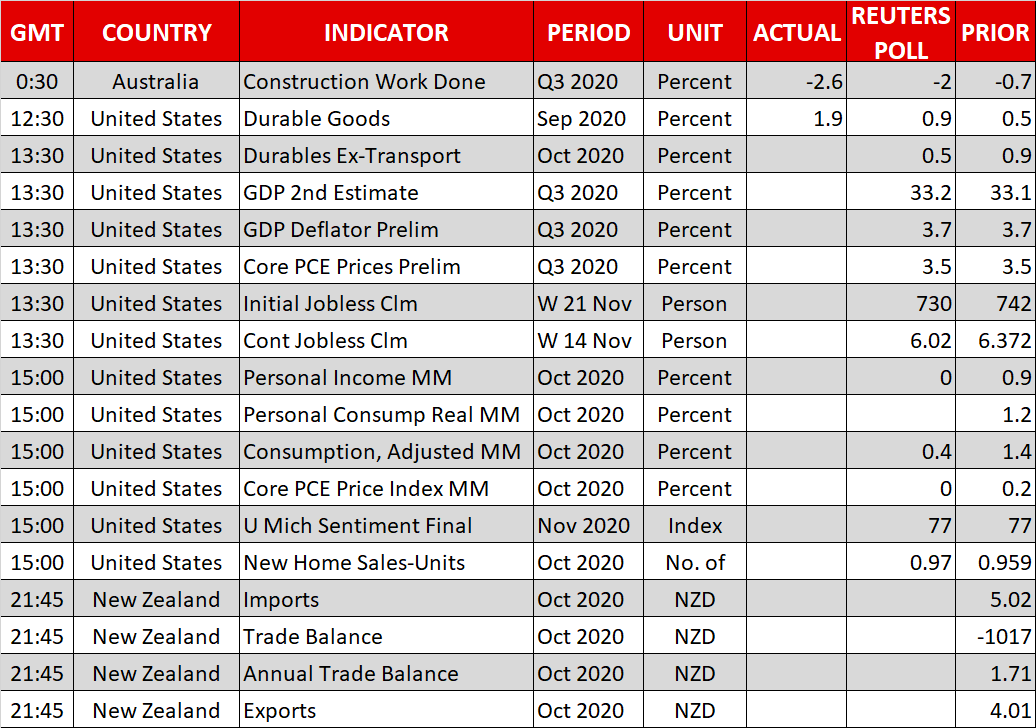

- Avalanche of US data and Fed minutes in the spotlight today

Vaccine enthusiasm continues to steer the ship

The party in global markets continues. Investors have thrown caution to the wind and have gone all-out in their hunt for returns, with exuberance around the post-vaccine world and an abundance of liquidity thanks to the world’s central banks powering the rally in riskier assets. The coronavirus may be airborne, but it is euphoria that is in the air right now.

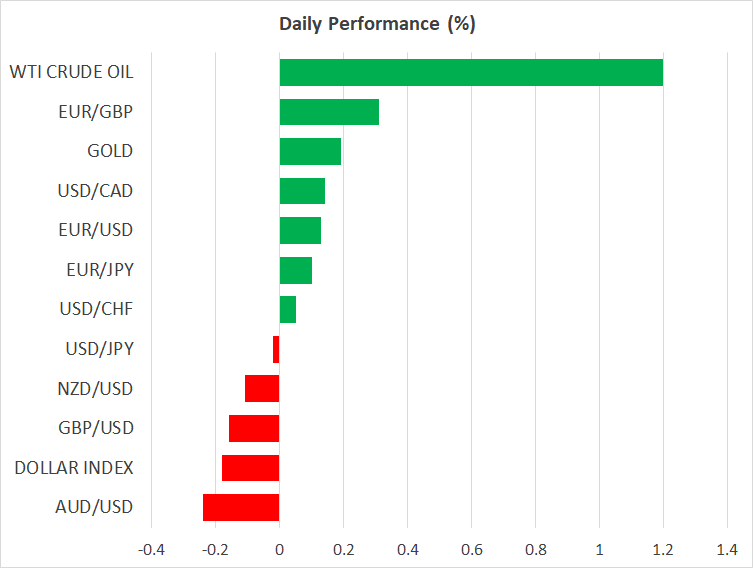

The main US stock indices all closed at fresh record highs on Tuesday, aside from the Nasdaq, which lagged a little as investors rebalanced towards vaccine-sensitive names and away from tech heavyweights. It was a similar story in the FX spectrum, where the commodity currencies powered higher alongside the euro and sterling, at the expense of defensive plays like the dollar, yen, and Swiss franc.

The catalyst for all this? Virtually none. The popular narrative is that investors took heart from the formal start of Biden’s transition to the White House, but admittedly, that seems more like an excuse to justify why the market is racing higher rather than an actual driver. Instead, a more plausible explanation may be that France and England announced a gradual relaxation of their national lockdowns, spurring hopes that other virus-stricken countries will follow in their wake.

In the grand scheme of things, sentiment across markets is sizzling hot right now. While that is natural considering the gravitas of the vaccine news and the cheap-money policies worldwide, there is a real risk that investors are running ahead of themselves. The near-term risk/reward picture for riskier assets doesn’t look very attractive here and the risk of a retracement seems elevated, though it is difficult to argue with the cheerful longer-term outlook.

Crude oil takes no prisoners, gold reels

The risk-on tide lifted all ships yesterday, but the real beneficiary was crude oil, which surged to levels not seen since the storm in March. WTI crude is currently trading above $45/barrel, buoyed by the vaccine joy and the gradual easing of lockdowns in Europe painting a brighter picture for demand, while chatter that OPEC will extend its production cuts next week is supporting the supply outlook.

Admittedly, a three-month extension of the current OPEC supply cuts seems almost fully priced in at this stage, so if the cartel wants to boost prices further, it needs to deliver something bigger. Of course, that is easier said than done considering the growing divisions within OPEC, with Libya and Iraq for instance wanting to ramp up their production.

Staying in the commodity sphere, gold prices continued to suffer yesterday even though the US dollar was broadly weaker. That is an ominous sign for bullion, which has fallen out of favor on speculation that vaccines imply higher real rates going forward. That is debatable given that inflation may be in the pipeline already and central banks are unlikely to allow bond yields to move much higher, but for now, the bears are in control.

The battle for the crucial $1800 region is in full swing, and if sellers slice through this barrier too, their next target may be the $1750 zone, where the 50-week moving average also resides.

Big day ahead for data

As for today, there’s a flood of US data coming up alongside the latest FOMC minutes at 19:00 GMT. Admittedly, most of these data points are for October, so they might be viewed as a little outdated. The same may be true for the minutes, considering that US covid infections were still running low when the Fed met in early November.

Still, investors will scrutinize all of this for hints on whether the Fed will deliver another round of QE in December. That is perhaps the biggest variable for markets at the moment.