The Federal Reserve will begin its first policy meeting of the year on Tuesday and will announce its decision on Wednesday at 19:00 GMT. No change is expected in the Fed’s monetary policy settings nor in its vast array of emergency programmes. The sweeping shakeup at the White House and the recently passed virus relief package by Congress likely bought the Fed a few months before policymakers need to start thinking about the next course of action. However, with so much optimism pinned on fiscal stimulus and the successful rollout of vaccines, does the Fed have a Plan B if things go awry?

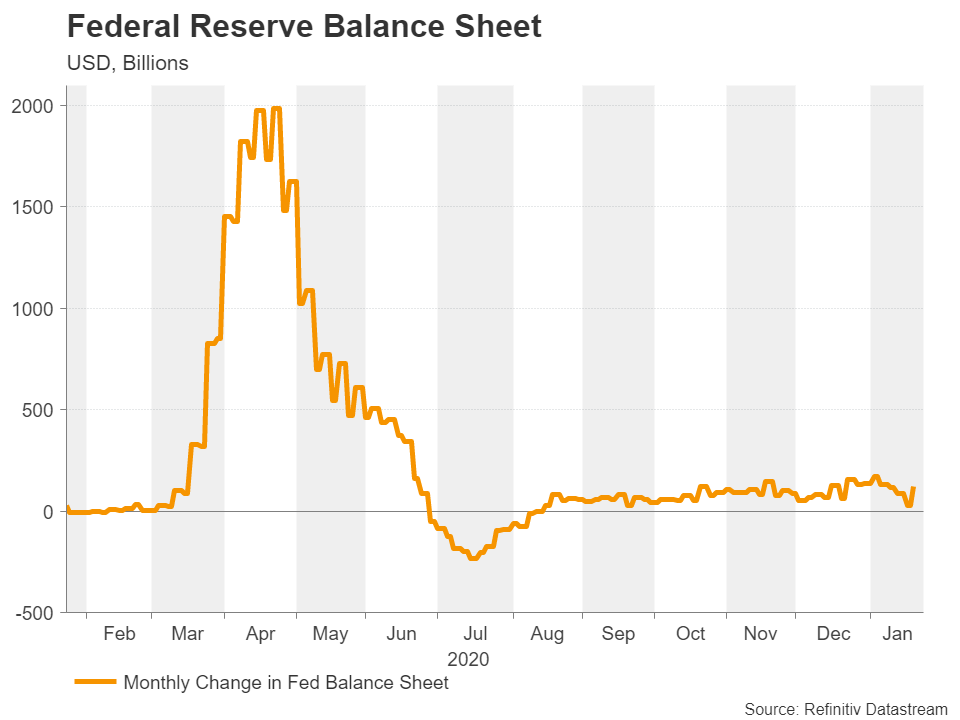

Fed has been in the backseat since March

Just under a year ago, the outbreak of the coronavirus left the Fed no choice but to take unprecedented steps to safeguard the US economy. The central bank’s swift and bold response likely averted a deeper crisis in financial markets. Since then, however, the Fed has said a lot but in actual fact, has barely lifted a finger policy-wise. The announcement last summer of a new inflation targeting regime was certainly a historical one. But from a practical perspective, it was nothing more than formalizing what the Fed has been doing all along: letting inflation run higher when the economic costs of higher interest rates outweigh those of temporarily letting loose some inflationary pressures.

Even December’s decision to provide forward guidance for its asset purchases hardly qualified as a significant change given how vague it was. However, when policymakers have already thrown everything but the kitchen sink at the problem and the barrage of stimulus and market intervention have worked in easing financial conditions, why do more?

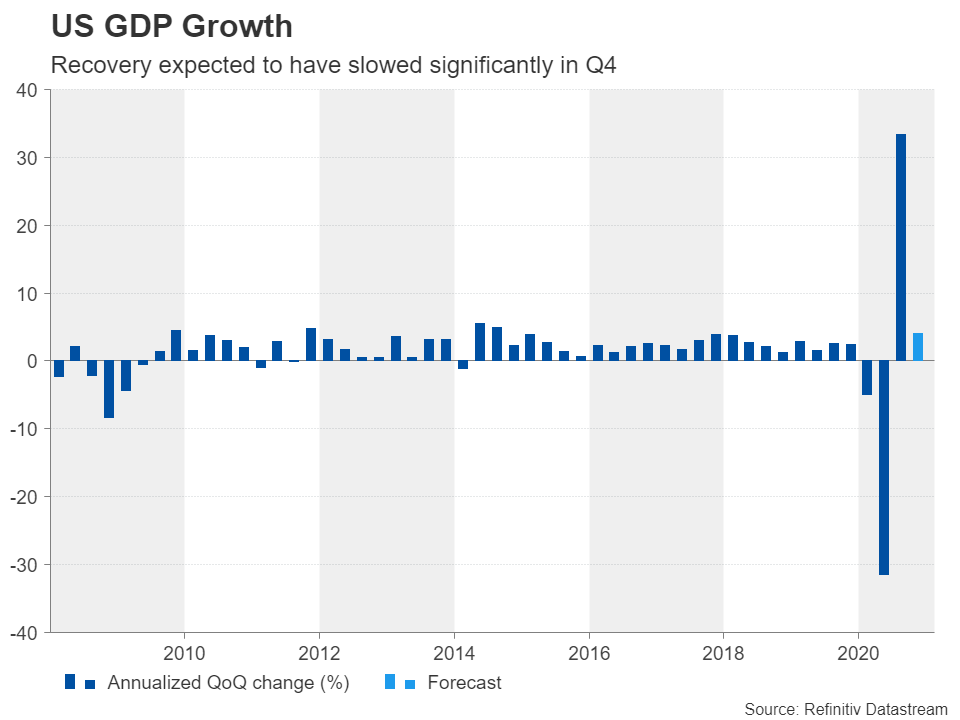

US economy: slowing or gathering steam?

Of course, another important element in this equation has been having a dovish chief at the helm. Chair Jerome Powell has not hesitated to reassure investors that ultra-low rates are here to stay and there are no plans to scale down the $120 billion a month bond buying plan anytime soon. Powell will likely reaffirm those pledges when he briefs reporters at 19:30 GMT. But while the press conference is usually the highlight of uneventful meetings, the January statement might be just as telling as to what to expect from the Fed in the coming months if there are any tweaks in the wording.

For one, there are conflicting signals on the strength of the US economy as jobs growth and consumption evidently slowed down at the end of 2020 even as manufacturers enjoyed bumper orders. The labour market is a key metric for the Fed and if the broader hard data fails to match the rosy business surveys over the coming weeks, policymakers might need to consider additional stimulus, especially if there’s a delay as to when the next fiscal package arrives.

December and GDP data eyed

Investors may be overestimating the odds of how easy it will be for the Biden administration to push its spending plans through Congress. Should fiscal stimulus begin to dry up just as economic indicators take a turn for the worse, the Fed might find itself in a tricky spot. The first batch of the latest hard data is due this week, starting with durable goods orders for December on Wednesday. The first estimate of Q4 GDP growth is out on Thursday and personal consumption expenditures will round up the week on Friday.

The American economy is expected to have expanded at an annualized rate of 4.0% in the fourth quarter, returning to more ‘normal’ levels after Q3’s V-shaped bounce. Whether this will be enough to sustain the recovery in the labour market is another matter. Personal consumption likely fell in December and this is bound to have dampened job openings. However, high-frequency data already point to a pick-up in credit-card spending in January as the new stimulus checks start to be disbursed so it may be too soon for the Fed to have to worry just yet.

Is there overoptimism about vaccines?

Another potential problem for the Fed is that markets may be putting too much hope on vaccines saving the day. There’s a danger that vaccination may only be the beginning to ending the pandemic rather than the magic bullet everyone is hoping for. Aside from the slow rollout in most countries, scientists keep discovering new mutated variants of Covid-19, which existing vaccines may be less effective against.

This again poses the question of how willing the Fed is to pump more liquidity or even maintain the existing pace of QE beyond 2021? Some hawkish FOMC members have already sparked talk of tapering and policymakers seem reluctant to keep a lid on rising long-term Treasury yields. It’s possible the Fed is keeping this option for a rainier day as switching bond purchases towards long-dated Treasury notes is the last powerful tool that it has left. Ten-year Treasury yields have already risen above 1% and further increases could push up mortgage costs, which could then weigh on the housing sector – the one true bright spot in the economy.

But perhaps the biggest complication that could disrupt the Fed’s current plan is unexpectedly high inflation. One closely watched gauge of inflation expectations – the 10-year breakeven inflation rate – has shot up to more than two-year highs to above 2.0%. Can the Fed stay so dovish if inflation expectations strengthen further?

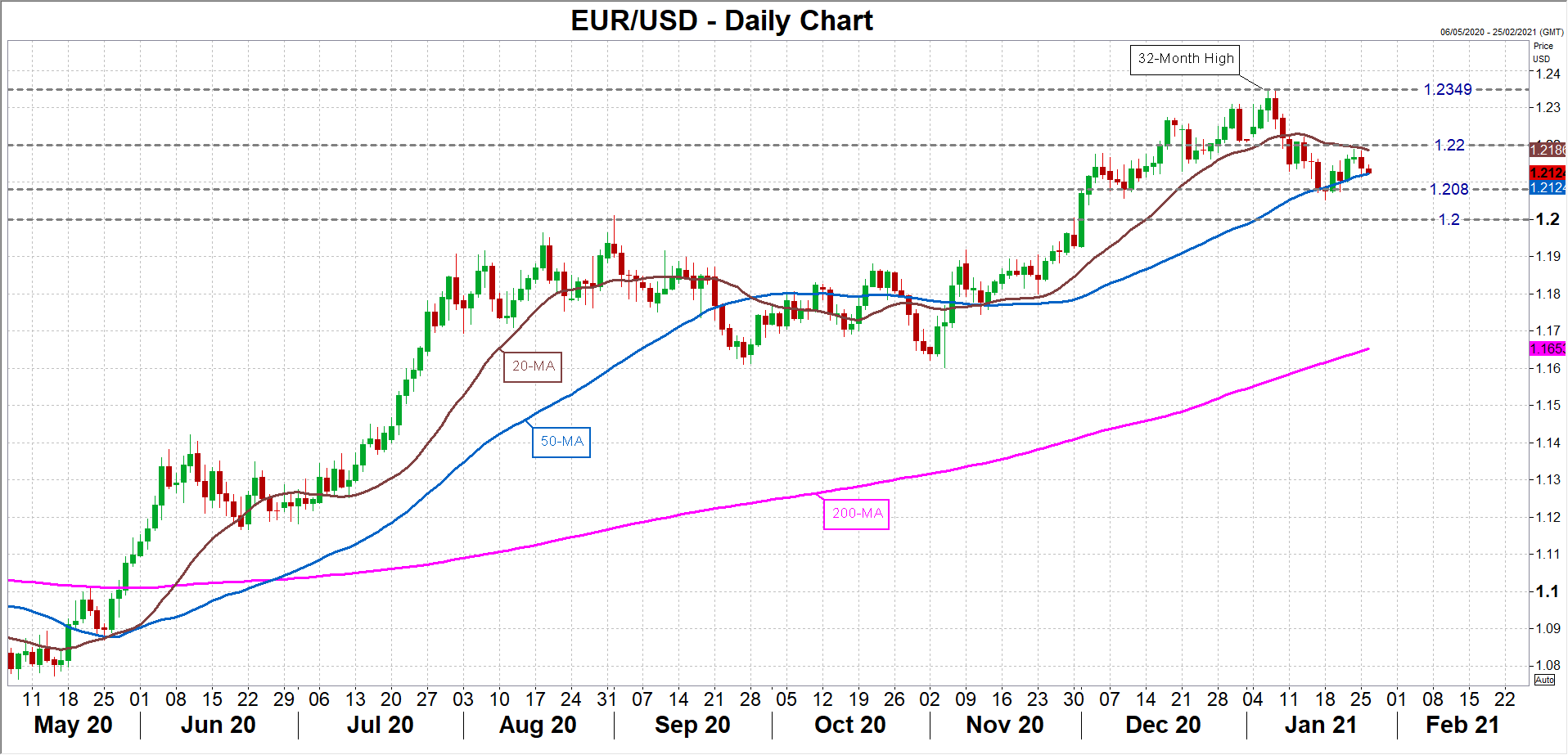

Fed meeting could trigger euro/dollar breakout

Should investors smell the slightest hint of resistance towards additional monetary stimulus from the Fed, the US dollar is likely to attract some fresh buying bids. Looking at the euro/dollar pair, a break below the 50-day moving average ($1.2124) and the $1.2080 support is possible if the Fed isn’t dovish enough on Wednesday. Although for a bigger selloff that would endanger the $1.20 handle, traders would need more specific clues about an early unwinding of asset purchases, which is not very likely.

If, though, Powell feels that markets are becoming too complacent about the risks to the outlook and is unhappy about the rising yields, he may try to reinforce the Fed’s dovish stance, pushing yields lower. Euro/dollar could then climb above the immediate resistance of the 20-day moving average, just below the $1.22 level, paving the way for another attempt at January’s 32-month peak of $1.2349.

Ultimately, the significance of the January meeting may only come to light when the minutes are published in three weeks’ time and investors are able to get a better insight on the latest FOMC views against the backdrop of a Democratic-controlled Congress, particularly those of the new voting members.

{kind=link}