Policy announcements from the Bank of Japan (BoJ) have been mostly boring over the past five years in the sense that investors blindly trusted that Governor Kuroda would never lift his foot off the easy-money pedal until he finally meets his inflation targets. On Friday, the Bank is largely expected to keep the same course when it reveals the results of its policy review at a tentative time. But given the growing rumours that some relaxation could be applied in its yield curve control, it would be interesting to see if the Bank can allow its benchmark yield to fluctuate in a wider range, likely helping the battered yen to recoup some lost ground.

Yield rally is not a problem so far

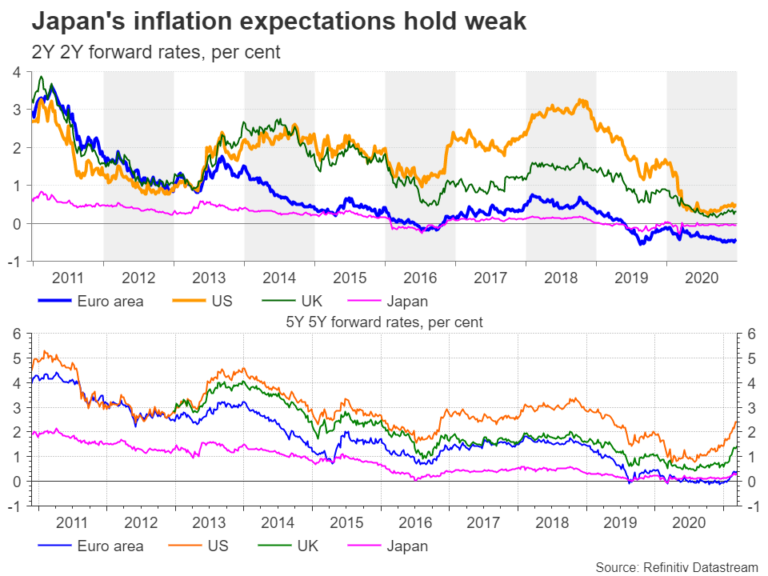

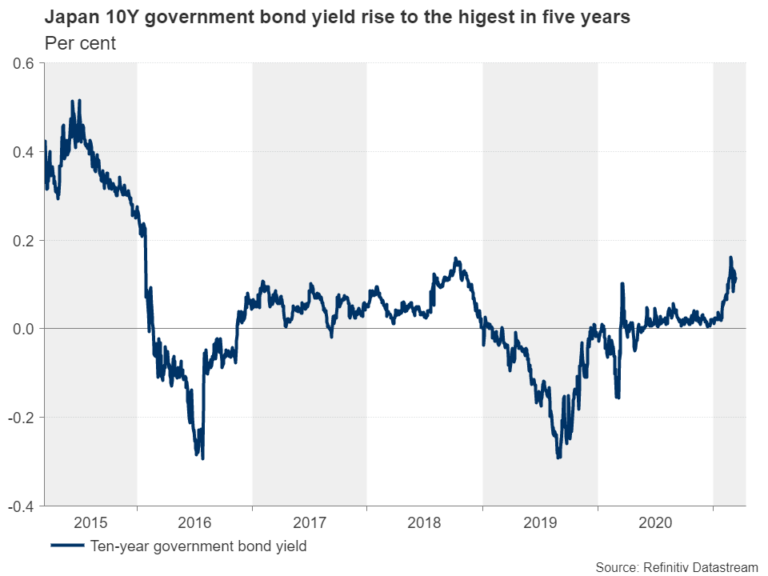

The prospect of a strong economic rebound and the stimulus euphoria in the US kept inflation expectations well above those in other key economies and raised speculation for an earlier monetary policy tightening, triggering a steep rally in US Treasury yields. While the yield rally spilled over into Europe and Asia, Japan could not take part in full force as the BoJ’s yield curve control has set a tight limit around 0% for the 10-year bond yield. Hence, the increasing gap between the US and Japanese 10-year bond yields has relatively benefited the dollar more, squeezing the yen to a nine-month low.

A weaker currency is not a problem during unpredictable pandemic times. On the contrary, it could be a relief for exporting businesses, especially for an economy such as Japan, whose safe haven currency is in high demand in times when negative shocks weigh on the global economy. Also, if the boost is driven by market forces as the Fed chief argues, the rise in yields should be more than welcome in this case. On the other hand, if the rise continues to pace up, the central bank may be forced to engage in heavier unscheduled bond purchases, which could become more costly for the Bank to sustain. Note that the overall monetary stimulus launched in 2013 means that the BoJ owns government bonds amounting to more than 130% of GDP and ETFs accounting for 7% of the equity market.

BoJ could pull the rabbit from its hat

The BoJ governor has notified in advance that he will continue to peg the 10-year yield around 0%, therefore the yield curve control policy will largely remain in place this week, with the central bank avoiding any actions which could give the impression of a tighter or looser monetary policy. The persisting reflation trade, however, may not be fully ignored, and as the ECB did, the BoJ could still pull a rabbit from its hat, although it has very limited tools at its disposal. Particularly, the Deputy governor said during his speech last week that changes to the range of bond yields are under consideration and could still keep ultra-loose monetary policy efficient, although they are neither necessary nor appropriate at the moment. His comments raised speculation that the Bank may allow for a wider range of fluctuations if the yield rally steepens in the coming months. Any comments on equity purchases may also gather interest following rumours that the Bank could remove the annual average band of 6 trillion yen and leave the upper limit of 12tln intact.

Market reaction

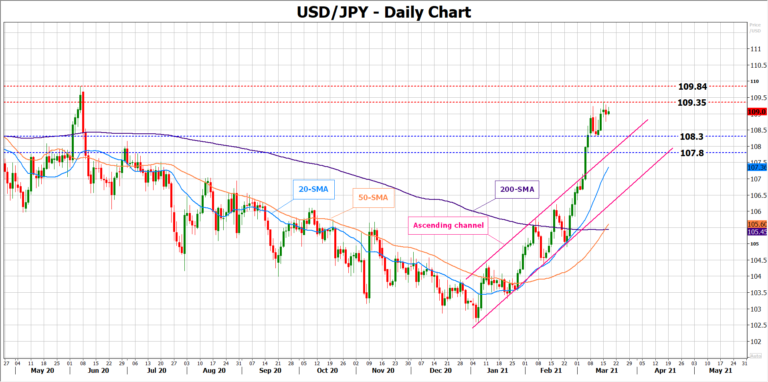

As regards the market reaction, the BoJ’s policy meetings have been barely causing any volatility over the past few months, but this time the Bank will also unveil its first policy review since 2016. Hence, the event may be worthy to watch as questions remain about whether the current aggressive monetary easing is enough to help the bank achieve its prolonged inflation goal of 2.0%. If the Bank indeed signals a more flexible approach towards its bond and equity purchases, the yen could recoup some of its losses, likely driving dollar/yen down to 108.30. A sharper decline could bring the surface of the broken channel under the spotlight around 107.80.

In the event the BoJ refrains from any policy adjustments, disappointing those who expect some tweaks in the yield curve control, the sell-off in the yen could continue, with the focus turning to the 109.84 peak from June 2020 if the 109.35 resistance area gives way.

{kind=link}