- New lockdowns in Europe dampen risk sentiment, bolster dollar and yen

- Stocks slip back but rumours of massive US infrastructure package lend support

- Kiwi slumps on steps to cool house prices, oil tumbles too, euro and pound muted

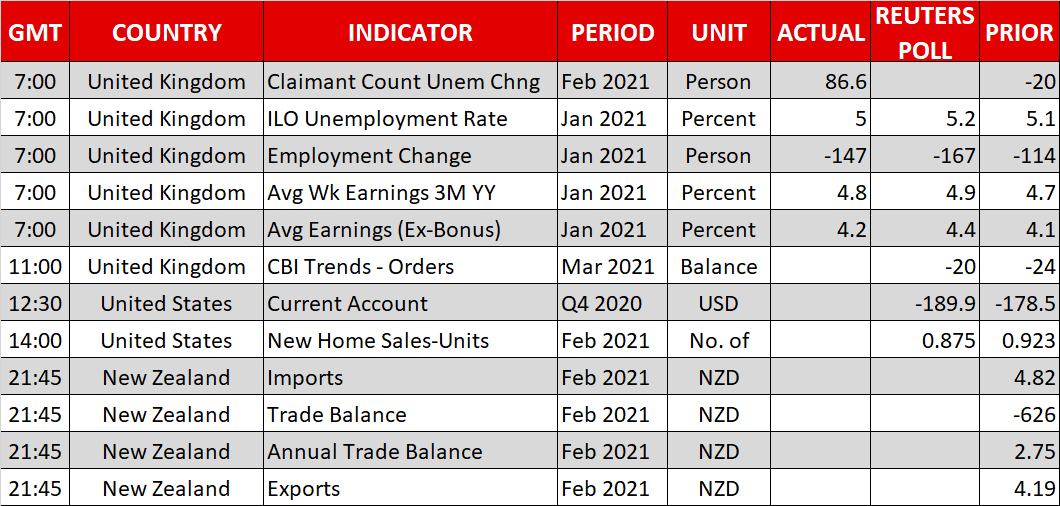

Dollar up amid fresh lockdown worries

Renewed fears about extended lockdowns in Europe are undermining risk assets again as a summer reopening of the continent’s economy is looking increasingly unlikely. Germany became the latest country today to delay a planned easing of virus restrictions, with Chancellor Angela Merkel announcing tough rules on public gatherings for the crucial long Easter weekend between April 1 and April 5. Other EU states such as France, Italy and Poland have also imposed tighter measures in recent days.

European nations are not only facing a major resurgence in Covid infections, but the EU has yet to get a grip on its chaotic vaccine rollout as the bloc is badly lagging in the global vaccination race. Supply issues have prompted the European Commission to threaten to ban exports of the AstraZeneca vaccine even as the public are shunning the jab on safety concerns.

Such a move would not only hurt the rollout in non-EU countries such as Britain but could escalate to a full-blown vaccine trade war if London decided to retaliate by blocking the export of a key UK-manufactured component of the Pfizer vaccine.

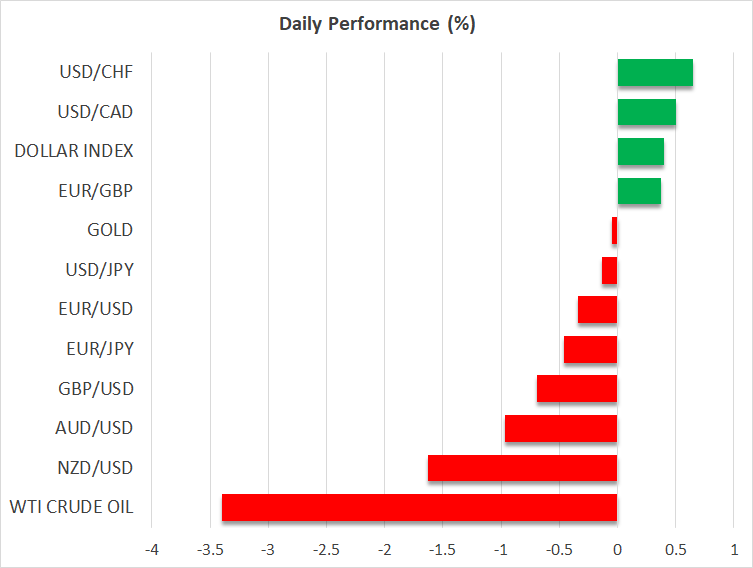

The growing risk of a serious disruption to the vaccine supply chain weighed on the euro and pound, while boosting the US dollar. The greenback stood about 0.4% firmer against a basket of currencies at the European open as the euro fell back below $1.19 and the pound plunged below the $1.38 level. The yen also powered ahead, rising across the board, including against the dollar.

Stocks hit by lockdowns, vaccine and geopolitical tensions

The darkening outlook over Europe pulled global equity markets lower. Travel stocks were the hardest hit as hopes of summer holidays abroad have been dashed for 2021. Meanwhile, bank stocks still reeling from yesterday’s Turkish lira crisis came under pressure from the falling yields of major government bonds.

In China, the country’s main stock indices slid close to 1% after the US, EU, Britain and Canada slapped sanctions on the country for human rights abuses in Xinjiang. Although there doesn’t appear to be a huge amount of concern in the broader markets, the concerted action by the United States and its allies could be a sign of more tough policies to come and suggest relations between China and the West could worsen under the Biden administration.

Losses in Europe moderated, however, through the course of the session, as US stocks futures were steady, holding narrowly in negative territory.

Investors have already begun to speculate the size of the next stimulus package in Capitol Hill, with some reports putting a price tag of $3 trillion. The White House has played down the reports, but markets are pinning their hopes on a big infrastructure bill that will boost growth beyond the expiry of the last virus relief package. Thus, stimulus chatter is here to stay and could be what’s shoring up the tech sector lately as the Nasdaq Composite posted its second straight day of strong gains on Monday.

A plethora of Fed speakers eyed; kiwi leads the losers

Another comfort for investors yesterday was fresh reassurance from Fed Chair Jerome Powell. In prepared remarks for today’s hearing before the House Financial Services Committee on the CARES ACT, Powell said the Fed will continue to support the economy “for as long as it takes”. He is due to testify at 16:00 GMT together with Treasury Secretary Janet Yellen. A number of other Fed officials will also be making public appearances today and so some volatility in bond markets is possible later in the day, especially as there’s another round of Treasury auctions coming up.

Treasury yields have pulled back somewhat in recent days, but Australian and New Zealand government bond yields have dropped even faster. The Australian dollar skidded by around 1% versus the greenback as oil and other commodity prices have come under pressure from the fresh round of lockdowns that are threatening the recovery timeline. WTI futures plunged by more than 3%, though the loonie was down just 0.45% against the US dollar.

The biggest loser, however, was the New Zealand dollar, which tumbled by more than 1.5% to around $0.7050 – a 3-month low. The selloff comes after the New Zealand government announced several measures aimed at cooling the country’s red-hot property market. If the government is able to bring house prices under control, there would be less of a need for the Reserve Bank of New Zealand to begin raising interest rates sooner rather than later, hence the slide.