U.S. Highlights

- Inflation fears have taken a breather in recent weeks, but the jury is still out on how temporary price pressures are.

- Today’s jobs report showed further solid progress. While better employment and wage gains may reinvigorate inflation fears, it would ultimately mean that the labor market is catching up with the economic expansion.

Canadian Highlights

- Canada got some good economic news to kick off the summer. Its economy was not as hard hit from the third wave of the pandemic as previously feared. GDP in April only declined by 0.3%.

- Still, April’s contraction was the first since April 2020 and Statistics Canada estimated another 0.3% decline in May. Weakness was concentrated in high-touch and manufacturing industries.

- The recent setbacks are likely to be temporary. Restrictions are being lifted and the vaccination rollout is progressing at an impressive rate. The Bank of Canada is monitoring developments as it considers reducing monetary stimulus in July.

U.S. – Employment Growth Is Catching Up

The last week of the quarter started in a risk-off mood as the Delta variant forced Australia and some Asian countries impose stricter controls. In the U.S. the spread of the variant seems to be isolated to several counties, but regions with lower vaccination rates may still face renewed restrictions should more cases translate into higher hospitalization rates. By mid-week, however, markets brushed aside the remaining shreds of gloom, pushing stocks to close higher for the fifth consecutive quarter and a strong start to the new month.

Inflation fears, too, seem to have taken a breather. Inflation expectations as measured by 10-year break-even rates pulled back in the last a few weeks (Chart 1). For the time being, markets seem to have adopted the view that price pressures are mostly temporary, and will reverse next year.

Yet the jury is still out on how temporary these price pressures are. In this week’s post, economists of the Federal Reserve Bank of Dallas provided an outlook on their trimmed mean PCE inflation rate, which excludes the most extreme price changes. In their view, the imbalances in a small set of PCE items have the potential to seep into a broader range of goods and lead to an upward move in prices. If this were to happen, the trimmed mean PCE inflation would increase to 2.4% by year-end 2022 and remain at that level through mid-2023. (Although relative to past periods of high inflation, this is fairly benign, particularly since Fed is targeting an average)

Meantime, prices paid by producers continue to climb. The June’s reading of the ISM manufacturing price sub-index jumped 4.1 percentage points, registering 92.1 – the index’s highest reading since July 1979 (93.1). Yet, the overall index declined with a 3.7-point drop in the supplier deliveries index driving the decrease. Furthermore, the backlog of orders index dropped by 6.1 percentage points, suggesting supply chain disruptions might be finally abating. A more sustained downward trend in these two sub-indexes may push the prices index lower in the coming months.

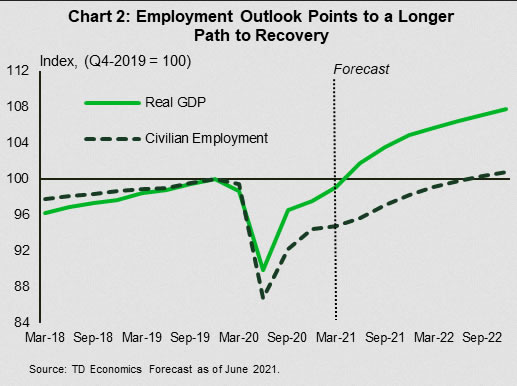

Another reason for markets’ recent tepid view of inflation is that investors are paying a closer attention to labor slack. Measured by employment, economic weakness is more apparent. While real GDP is expected to surpass its pre-pandemic peak in the second quarter of 2021, employment is on a much longer path to recovery (Chart 2). In this context, today’s report shows further progress. TD Economics expects continued gains through the third quarter as schools return to in-person learning and supplementary unemployment benefits expire. The economy added 850K jobs in June, above market expectations, while data revisions added another 15K, lifting the employment gap to 4.4% relative to its pre-pandemic level.

Should the pace of job creation remain strong over the summer, and could reinvigorate inflation fears in the coming months, but ultimately, this would mean that the jobs growth is finally catching up with the economic expansion..

Canada – Pleasant GDP Surprise For Canada’s B-Day

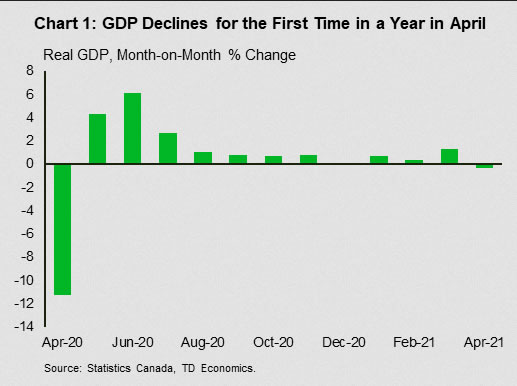

Canada received good economic news in the week of its 154th birthday. Real GDP growth, which markets expected to decline by 0.8%, only fell by 0.3% on the month. Moreover, Statistics Canada revised up growth in March, resulting in a solid starting point for the second quarter. Indeed, even though Statistics Canada’s advance estimate for May pointed to another 0.3% decline, quarterly growth is now tracking in the range of 2.5% to 3%, almost a percentage point above our June forecast.

Still, it’s hard to ignore the fact that GDP did decline for the first time in a year in April, and will likely fall further in May (Chart 1). The impact of the third wave of the pandemic and tighter restrictions dampened economic activity during these months, with high-touch services sectors (retail, accommodation and food services, arts, entertainment, and recreation, and other services) once again the hardest hit. Collectively these industries lost 4% of output (m/m) in April alone.

Weakness was not only concentrated in high-touch services industries, the manufacturing sector also took a tumble, declining by 1% in April. Unlike services, however, manufacturing was held down by the global semiconductor chip shortage. In particular, motor vehicle and motor vehicle parts subsectors bore the brunt of the impact with output declining by 20.9% and 13.4%, respectively. As the semiconductor shortage is likely to persist, production could remain weak in this area of the economy for some time.

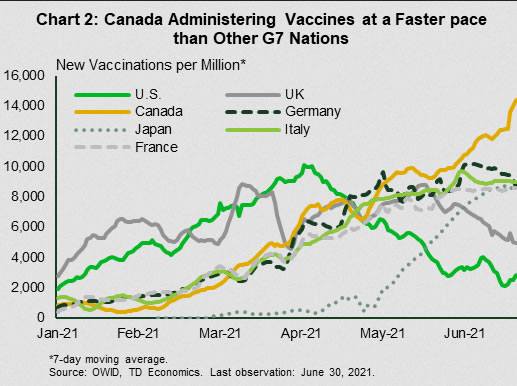

On the whole, however, the setbacks in April and May are likely to be temporary. Restrictions are being lifted across the country, and COVID-19 cases and hospitalizations are falling. This would not have been possible without the extraordinary vaccine rollout in Canada. The country stands well above other G7 countries in terms of the pace of vaccinations (Chart 2), and is on track to have 75% of the eligible population fully vaccinated by the end of July. This impressive speed may even help lessen the downside risks posed by the more contagious Delta variant.

The Bank of Canada is paying close attention to these developments. In a speech in early June, Deputy Governor Timothy Lane noted that the Bank’s Governing Council will monitor how the economy is responding to reopening measures, and that this will inform them on the future of monetary stimulus. Specifically, if reopening spurs a solid bounce back in economic activity, the economy will not need as much stimulus from the quantitative easing program. Assuming provinces ease restrictions as planned, the Bank could reduce the pace of asset purchases as early as July.

In terms of the overnight rate, it’ll take more than a successful reopening of the economy to force the Bank into rate hikes. Unemployment is considerably higher than what it was prior to the pandemic, and it may take several quarters for people to find new jobs. The Bank currently sees this happening sometime in the second half of 2022, and that’s probably when we’ll see the first rate hike.

{kind=link}