ECB today announced the outcomes of its long-awaited monetary strategy review, see here. The results were originally only expected to be unveiled by the end of the summer, however, after intensive discussions the Governing Council (GC) members reached unanimous agreement on the review results sooner than expected.

Below we summarize the key outcomes:

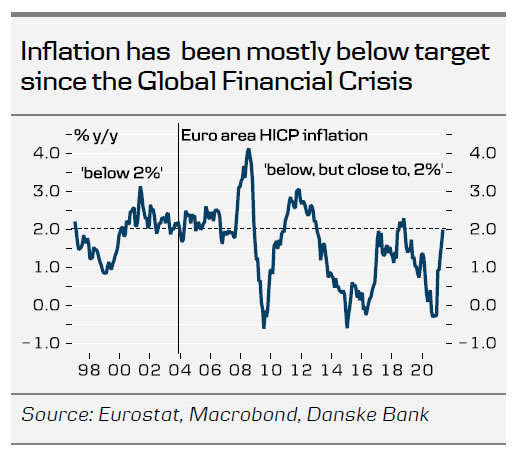

- Price stability objective: The primary objective of the ECB remains price stability, as established in the Treaty on the Functioning of the European Union. In recent years, ECB has faced growing criticism of an asymmetric understanding of its ‘inflation rates below, but close to, 2%‘ formulation of price stability that was adopted in 2003. Going forward the ECB will therefore define its price stability objective as a simple symmetric 2% inflation target over the medium term. This also includes a flexible understanding that inflation will not always be on target, but fluctuate around the 2% level. This should provide the ECB with sufficient flexibility and leeway to calibrate its monetary policy in a holistic way, still focussing on inflation, but without being ‘locked’ due to a specific rule. This also implies a more flexible inflation targeting regime than the Fed’s average inflation targeting (AIT), which explicitly requires making up for any past inflation misses. In that sense, the new symmetric ECB target is somewhat less aggressive than the Fed’s AIT, by tolerating, rather than targeting an inflation overshoot. We do not expect the new symmetric inflation target formulation to have much implication for monetary policy in the short- to medium-term, explaining the muted market reaction to the announcement. Despite an accelerating recovery and growing cost-push pressures in manufacturing, the outlook for underlying inflation is still muted in the euro area and we remain sceptic that core inflation is about to return to the highs preceding the Global Financial Crisis on a sustained basis (read more in Research Euro Area – Mind the inflation gap, 8 June). Over the long-term, the new price stability target could on balance imply a more patient stance with regard to any future monetary tightening, with inflation overshoots more explicitly allowed.

- Inflation target measure: Despite the symmetric price stability target, the inflation target will continue to be formally defined by the Harmonised Index of Consumer Prices (HICP) or headline inflation. That said, we expect ECB to continue to effectively base its monetary policy decisions on the developments in underlying inflation, i.e. ‘core’ inflation with excludes volatile items such as food and energy prices.

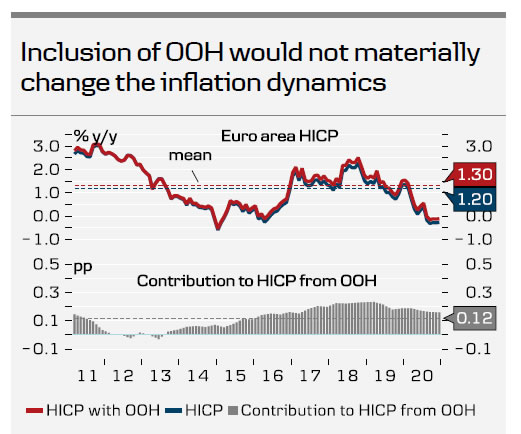

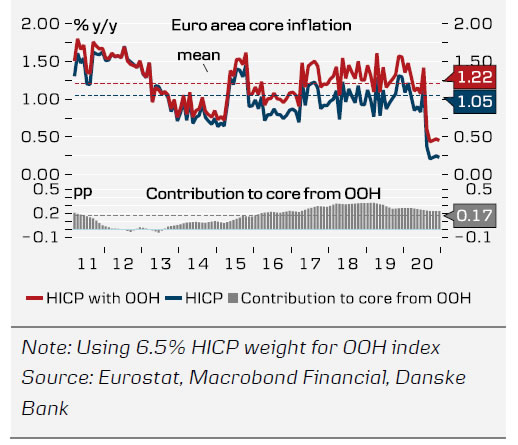

- HICP composition: Sharp increases in house prices and rents in recent years have reinforced the gap between official inflation measures such as HICP and the cost of living perceived by consumers. In light of this there has been a growing debate to include the cost of owner-occupied housing (OOH) in the HICP basket. While the decision on the exact computation of HICP ultimately rests with Eurostat, the ECB has now explicitly recommended the inclusion of OOH in HICP over time. However, even if Eurostat follows the ECB’s recommendation, the actual implementation into HICP will likely take a few years to materialize, not least due to data quality issues. Until this is achieved, estimates of costs of OOH will play a supplementary role in the ECB’s inflation assessment. Overall, the inclusion of OOH would however not dramatically change the inflation picture, lifting HICP inflation by ca. 0.1pp and core inflation by ca. 0.2pp on average (read more in Euro Area Research – Housing inflation: Opening Pandora’s Box, 6 February 2020). In that sense, the inclusion of OOH costs alone will not solve the problem of reaching the inflation target. Indeed, it could turn out to be a Pandora’s box: With housing being more responsive to cyclical swings, its inclusion could well introduce an added element of volatility in HICP. This could make the ECB’s task even harder, not only with regard to containing deflation risks during downturns, but also in terms of accurately deciphering and predicating the medium-term inflation outlook.

- Climate: Since Lagarde took office, the climate change agenda has seen increasing focus by the ECB and markets. To further incorporate climate change considerations into its policy framework, ECB has now adopted a climate change action plan. This involves expanding analytical capacities in macroeconomic modelling, statistics and monetary policy with regard to climate change and including climate change considerations in monetary policy operations in the areas of disclosure, risk assessment, collateral framework and corporate sector asset purchases. The ECB will introduce disclosure requirements for private sector assets as a new eligibility criterion or as a basis for a differentiated treatment for collateral and asset purchases, with a detailed plan announced during 2022. ECB will also start conducting climate stress tests of the Eurosystem balance sheet in 2022. With regard to corporate sector asset purchases, the ECB will adjust the framework guiding the allocation of corporate bond purchases to incorporate climate change criteria.

Will ECB now meet its inflation mandate?

As the ECB strategic review resulted neither in the development of new monetary policy tools that could foster the achievement of the inflation target, nor changed its explicit target variable of HICP inflation at 2%, we do not see the probability of ECB meeting its inflation objective altered by the strategic review. For ECB the conundrum remains that underlying inflation pressures remain anchored at a too low level and without the support from other policy areas (namely fiscal policy), ECB will continue to face challenges in living up to its inflation target in our view, be it defined as below, but close to, 2% or just 2%.

{kind=link}