Summary

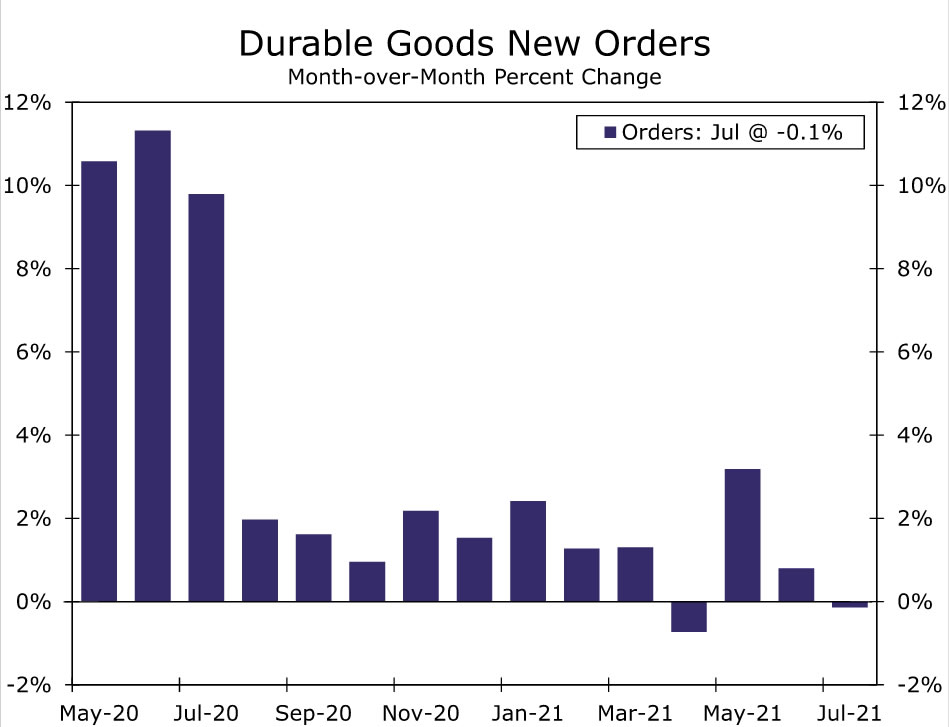

The scant 0.1% decline in durable good orders in July is not as large a dip as had been expected. The not-as-bad outcome is due in part to surging orders for autos and many old-line manufacturing categories. Core capital goods shipments rose 1.0%, pointing to another incremental step in the right direction for supply chain pressures.

This Just In: Auto Dealers May Actually Have Vehicles to Sell

This is only the second time since the initial reopening of the economy in May of last year that durable goods orders posted a decline. We were braced for a larger one. The scant 0.1% dip in orders for durable goods is remarkable after accounting for the fact that civilian aircraft orders fell by about half during the month.

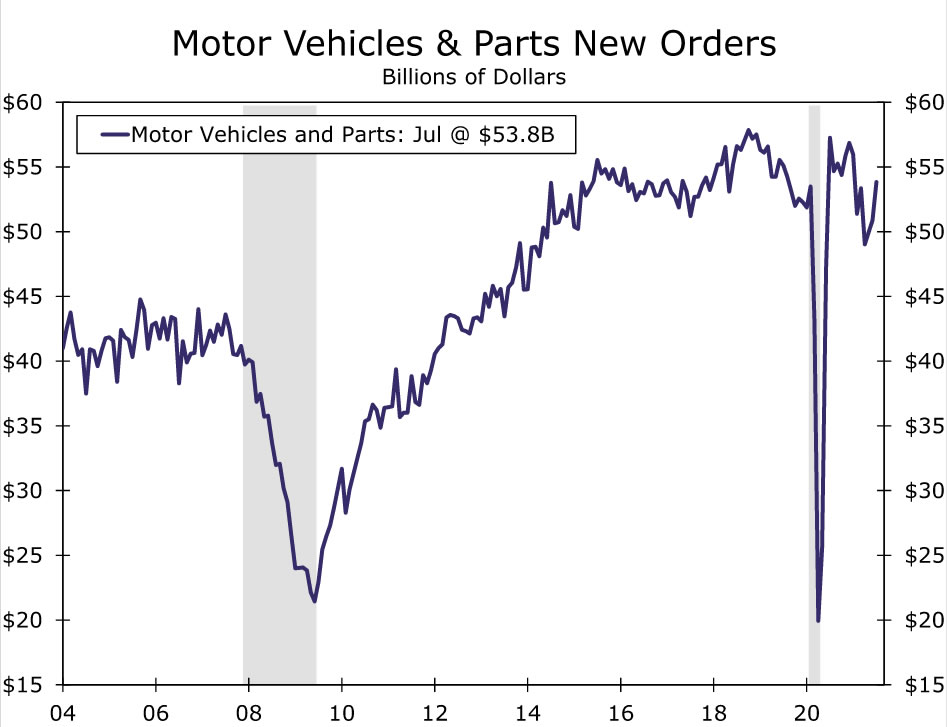

It is still mad times in the auto market, but there are some signs of improvement. Orders for vehicles and parts shot up 5.8%. Aside from the reopening of auto plants last summer, that is the biggest monthly gain in more than six years. As anyone who has been in the market for a vehicle in the COVID-era can tell you though: taking the order is easy, delivering on it is what is tough. But in a welcome development, shipments of vehicles and parts rose a slightly larger 5.9% in July. Auto dealers may gradually begin to refill nearly empty lots. But make no mistake, auto-production is still struggling to keep up with demand.

Elsewhere, spending was a mixed picture. After increased spending on tech over the past year or so, some pullback was evident in July. Electrical equipment orders fell 1.8% and computers and other electronics products slipped 0.4%

But old-line manufacturing continues to flex its muscles with orders for fabricated metals adding 0.3%, primary metals orders up 2.7% and bookings for machinery up 2.9%. Machinery orders have done nothing but rise since April of last year. The level of orders today is up 12.2% from where it was at its 2018 peak before the trade war began a trend decline through 2019 and early 2020.

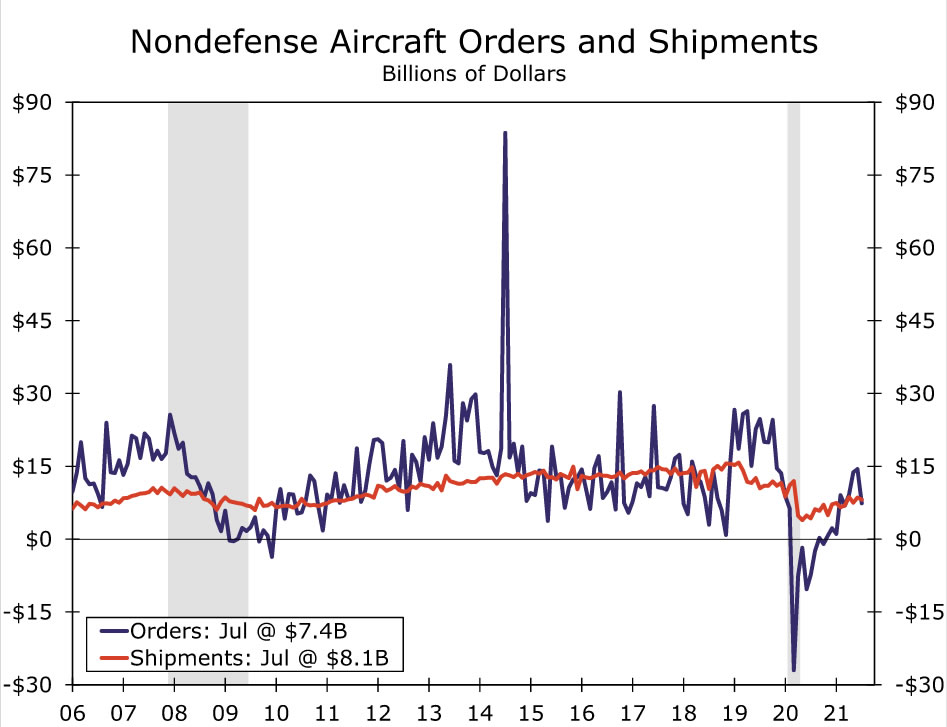

A bulk of the weakness in orders therefore came from nondefense aircraft orders, which tumbled nearly 50% in July. Excluding transportation, durable goods orders rose 0.7%. Based on our calculations from Boeing’s publicly available data, there were only 14 net new orders during the month after accounting for cancellations, a considerable pullback from the 146 net orders last month.

Civilian aircraft orders had been rebounding in recent months but amid renewed concern about whether the pandemic has permanently changed demand for business travel. Even before accounting for cancellations Boeing’s 31 gross monthly orders were less than half what we’d see in a typical July; that month’s average gross increase since 2000 is 75 orders.

Another Step in the Right Direction for Core Shipments

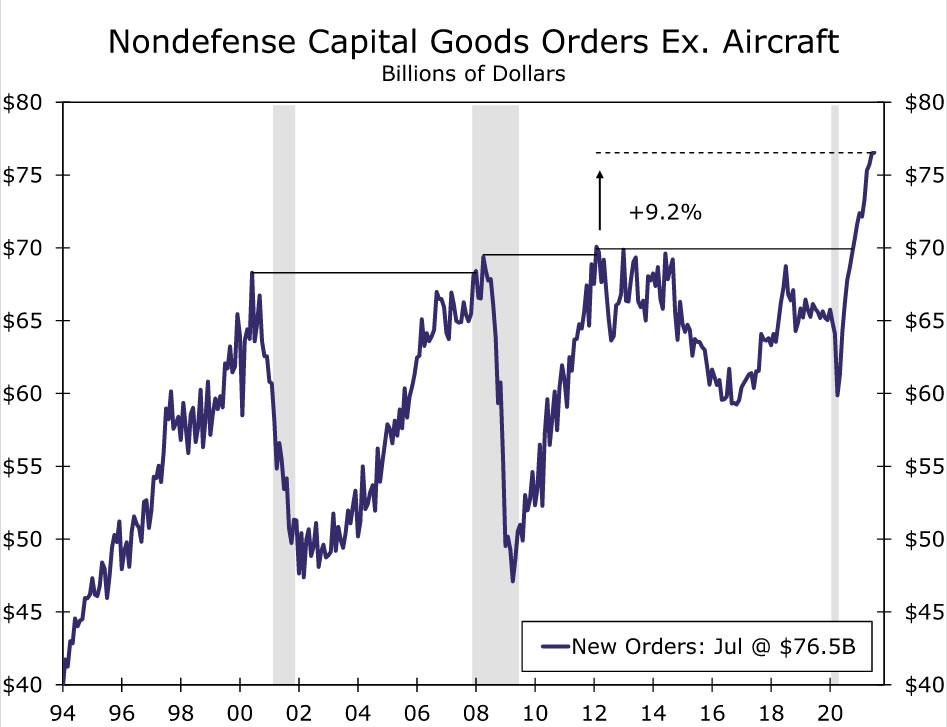

Core capital goods orders were flat in July, but the run-up in goods consumption during the pandemic has resulted in a speedy rebound in orders to date. An upward revision to June data suggest orders are 9.2% ahead of their prior cycle peak through July. With some business demand being pulled forward last year to facilitate work from home and consumer spending transitioning back to services from goods, some weakness in demand is understandable. But we expect the need for businesses to replenish scant inventory levels to keep orders strong in coming months. Still-constrained supply chains will weigh on fulfillment as unfilled orders continue to rise at a decent clip, suggesting some weakness in July may be due to bottlenecks rather than weak demand. The value of unfilled orders for motor vehicles, for example, increased to a fresh record as the sector struggles to get the inputs in needs to produce.

Shipments did pick up during the month with core capital goods shipments up 1.0%, which brought the three-month annualized growth rate of the three-month moving average to 12.1%. This is a positive indication of strong equipment spending in the third quarter, but as we’ve cautioned in recent months, the true pace of real equipment spending will likely be less impressive as orders and shipments are reported in nominal dollars. The recent run-up in prices, therefore will likely eat into some of the gain. Increases in shipments were broad based with all core shipment categories rising last month.

{kind=link}