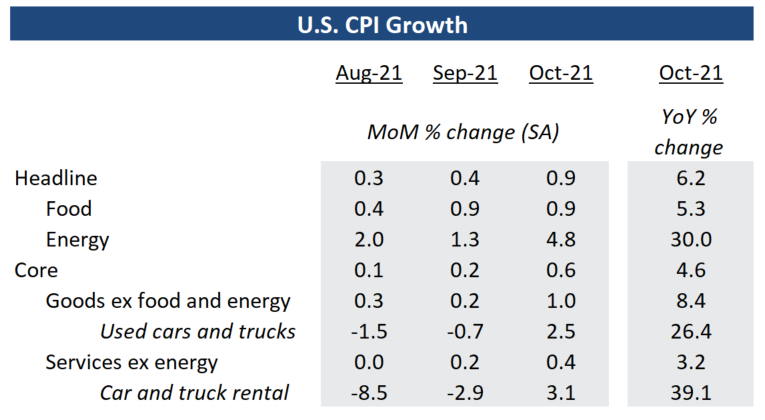

- Headline inflation rose to 6.2% from a year ago, 0.9% on a seasonally adjusted basis from September

- Core prices (ex-food and energy) grew a faster 0.6% month over month

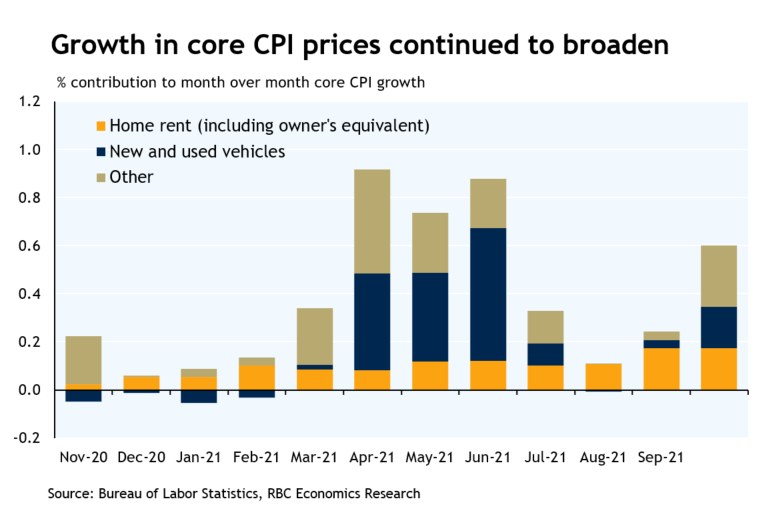

- Price growth expected to continue to broaden, as higher costs filter through to consumer

Headline inflation rate in the US reached 6.2% in October, up from 5.4% in September supported by already broadening price growth in almost all categories. That’s the fastest pace of annual CPI growth the US has seen since the early 1990s. Those year-over-year growth numbers continue to be in part inflated by lower year-ago price levels when the economic impact of the pandemic was much more significant, but excluding base effects, inflation was still around 3.7% each year relative to pre-pandemic 2019 levels. Used car prices rose again from already high levels after a surge in prices in the spring and were up 26.4% from last year. That together with growth in new vehicle prices contributed to over a fifth of the headline increase in October, and will continue to distort the headline figure in coming months as the global semiconductor shortage persists. On a month over month seasonally adjusted basis, headline prices rose 0.9% from September, boosted by pricier food (+0.9%) and energy (+4.8%) products, the prior driven mostly by more expensive meat products and the latter tied to higher prices at pump.

Outside of food and energy products, core prices were up 0.6% on a seasonally adjusted basis from September, with more signs that the pace of price growth is broadening outside of auto products. Prices for rent and owners’ equivalent rent, for example, both continued to rise at faster rates (+0.4%) from already stronger readings in September. Our base case view remains that surging input and labour costs, supply chain disruptions, and elevated household purchasing power will keep a floor under near-term price growth. We also expect pressure to continue to broaden across the consumer basket away from pockets like auto that have disproportionately impacted pandemic inflation trends to-date. In terms of expectations, consumers have been dialing that up for the near-term and longer-run expectations have also increased but remained closer to levels just above Fed’s 2% target. With labour markets continuing to improve, and inflation running hot, the Fed is expected to begin hiking rates next year, with earlier rather than later hikes more likely the longer inflation pressures continue to broaden.

{kind=link}