Summary

- Prior to Friday, June 10, we shared the universal consensus that the FOMC would hike rates by 50 bps its June 15 policy meeting. But the higher-than-expected inflation print for May now has us looking for a 75 bps rate hike.

- This expectation was reinforced by press reports on June 13 that seem designed to re-calibrate market expectations regarding the potential magnitude of the rate hike.

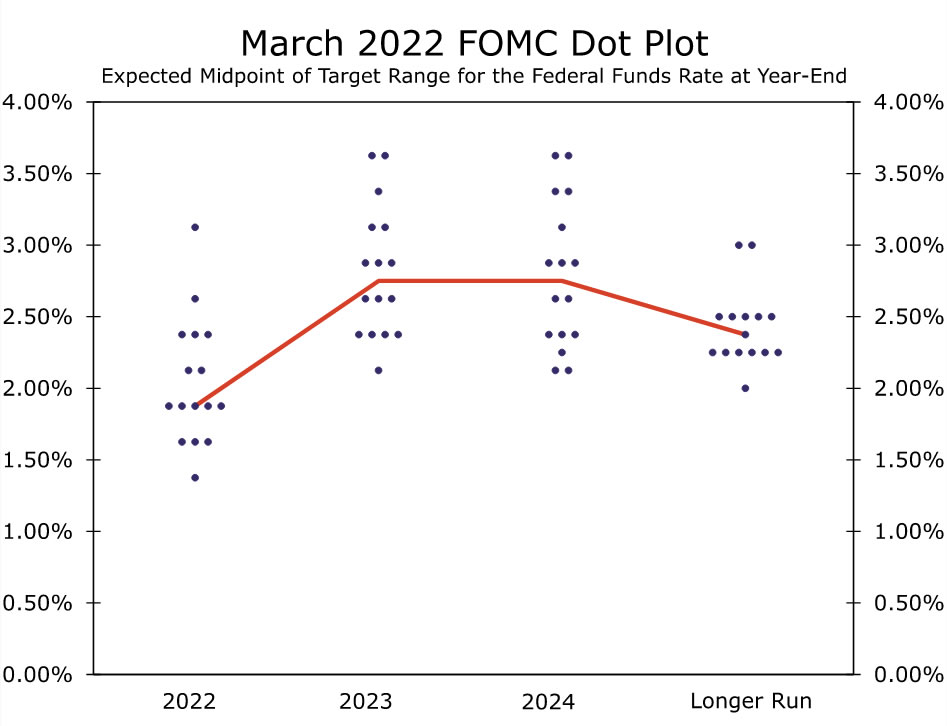

- We also look for a meaningful upward shift in the so-called “dot plot,” which would indicate that Fed policymakers believe even more monetary tightening is appropriate in coming quarters.

- We look for the median dot to shift up to 3.375% at the end of this year and to 4.125% at the end of next year.

- We also expect the FOMC will raise its inflation forecast for 2022 while also paring down its GDP growth forecast for this year.

Source: Federal Reserve Board and Wells Fargo Economics

We Now Look for a 75 bps Rate Hike

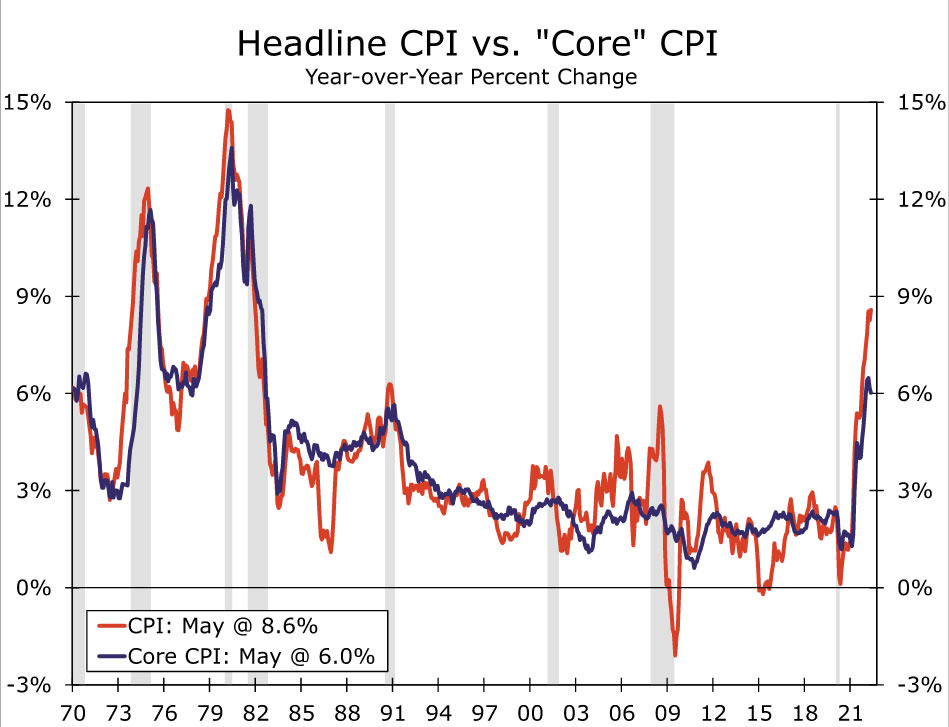

In the preview report we wrote on June 6 that outlined our views about the June 15 FOMC meeting, we made the case for why a 50 bps rate hike was all but assured. But, that report was written before the May CPI data were released on June 10,which showed that inflation was once again higher than expected. Specifically, the overall CPI rose 1.0% in May, which boosted the year-over-year rate of inflation to 8.6% (Figure 1). Furthermore, the data were disheartening because they showed broad-base price pressures in the economy. In short, the Federal Reserve appears to be further “behind the curve” in its efforts to reduce the rate of inflation.

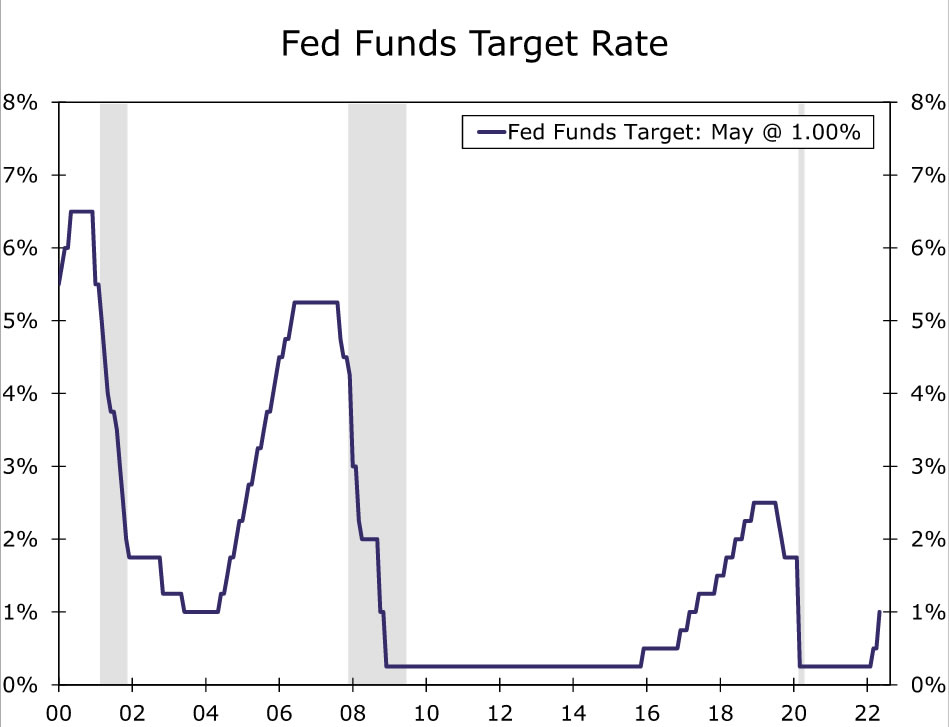

Consequently, we now believe it is likely that the Committee will opt to hike rates by 75 bps, which would take the target range for the fed funds rate to 1.50% to 1.75%. This expectation was reinforced by press reports on Monday, June 13 that policymakers would consider “surprising” markets with a 75 bps rate hike. Because we are now in the 10-day “blackout” period that usually precedes FOMC meetings, Fed officials are not scheduled to give any speeches. However, these press reports, which likely were confirmed by off-the-record comments by Fed officials, serve the useful purpose of re-calibrating market expectations in a rapidly changing environment.

That said, the Committee could still opt for 50 bps, although we think 75 bps is much more likely. In the event that the FOMC hikes by only 50 bps, we believe it would signal more aggressive tightening ahead via Chair Powell’s post-meeting press conference and/or a significant shift higher in the so-called “dot plot.”

Summary of Economic Projections: Higher Dots and Inflation, Less Growth

The dot plot (Figure 2) to be released on Wednesday likely will signal even more monetary policy tightening than we previously envisioned. In our previous FOMC preview report, we looked for the median dots for year-end 2022 and 2023 to rise to 2.875% and 3.375%, respectively. In light of last week’s economic data, we now believe these projections are too low. We look for the year-end 2022 dot to be 3.375%, which would imply 175 bps of additional tightening at the four remaining FOMC meetings of the year (or 200 bps if the FOMC only hikes by 50 bps at the June 15 meeting). For 2023, we look for a year-end dot of 4.125%, which if realized would imply a target range of 4.00% to 4-25%. For 2024, we think the dot plot will signal that rates are steadily declining back toward the “neutral” rate of 2.50% or so. Accordingly, we look for the median dot for 2024 to be 3.125%.

On the inflation front, the Fed’s projections will almost certainly move higher, particularly for headline inflation. Our June 8 forecast looked for the PCE deflator to increase 5.8% year-over-year in Q4 of this year, and the risks to that forecast lie to the upside after the CPI release on June 10. The median projection in the March Summary of Economic Projections (SEP) was 4.3%, and we would not be surprised if the June SEP has a median projection north of 5%. We doubt headline inflation projections for 2023 and 2024 will increase all that much as we suspect the FOMC will implicitly assume that food and energy prices decelerate and perhaps even decline somewhat in 2023 and beyond. The median projection for core PCE inflation may also tick up a tenth or two for 2022 and 2023.

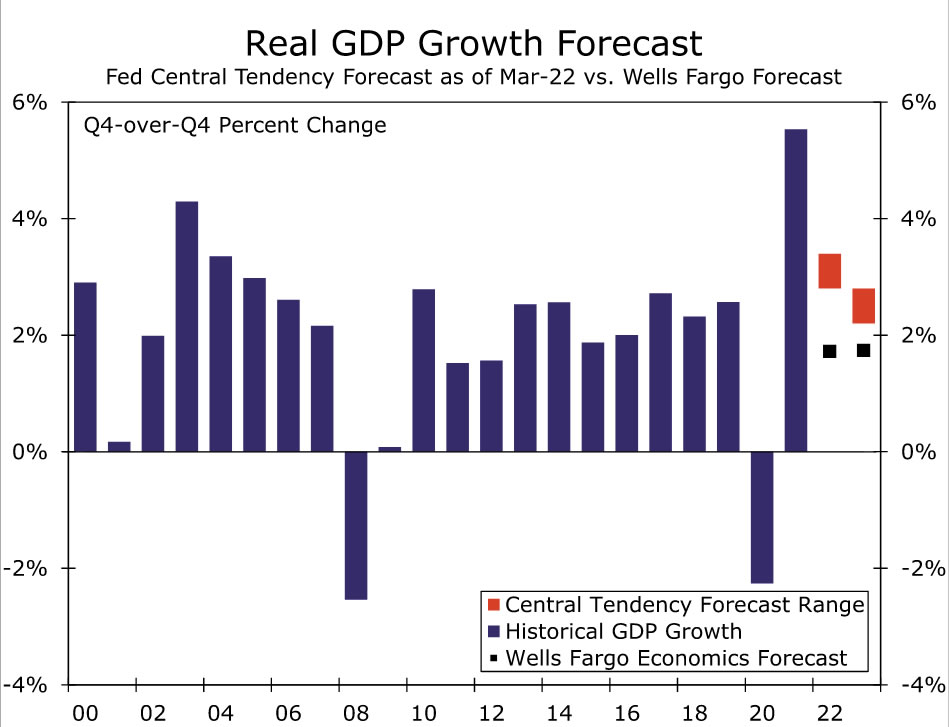

Although the FOMC’s projections for the federal funds rate and inflation are likely headed up, the same cannot be said for the Committee’s growth forecasts. The March SEP looked for 2.8% real GDP growth year-over-year in Q4-2022, whereas our most recent forecast looks for 1.7% (Figure 3). We doubt the FOMC will revise its forecast down that much, but a median projection of between 2.0% and 2.25% seems plausible to us. The FOMC’s trend-like projections for economic growth in 2023 and 2024 may fall modestly, but we doubt that they will fall substantially.

Similarly, the Fed’s March projections for the unemployment rate were flat in 2022 and 2023 at 3.5%, with just a modest uptick to 3.6% in 2024. A small increase in the median unemployment rate projection strikes us as plausible for 2023 and 2024. The “longer-run” projection for the unemployment rate was 4.0% in March, so the Fed could signal slightly higher unemployment while still tacitly signaling that it believes a soft landing is in the cards.

{kind=link}