The latest CPI inflation data will be scrutinized on Tuesday (12:30 GMT) as it will be the last before the Fed’s September policy meeting. Last month’s report offered the first hope in months that price pressures have started to abate, but Fed policymakers were quick to dash expectations that this would equate to an immediate shift in policy towards a more dovish path. Another consideration for the Fed will be Thursday’s retail sales figures as the series of rate hikes have yet to significantly dampen consumer spending. The US dollar has gotten off to a softer start to the week ahead of the data, amid speculation that September’s rate rise will be the last three-quarter point move.

Inflation seems to be on the way down

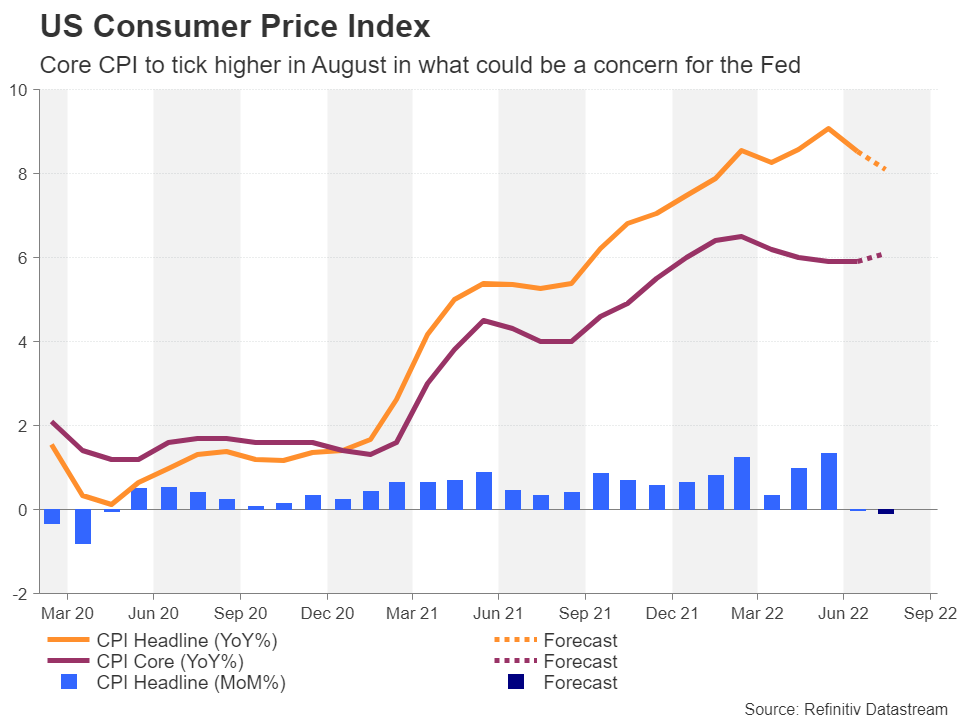

There was widespread relief when America’s consumer price index stood flat in July, marking the slowest monthly change since May 2020 when the economy was just coming out of lockdown. On a year-on-year basis, CPI rose by 8.5%, slowing from June’s four-decade peak of 9.1%. Much of the slowdown was attributed to the drop in gasoline prices that came on the back of the decline in crude oil prices during the summer. However, prices either fell or grew at a weaker-than-expected rate in other categories too, in an encouraging sign that inflation may finally be peaking on a broader level.

Fed wants to see more evidence

Not so fast, says the Fed. Far from even acknowledging that the inflation picture could now be at a turning point, policymakers have been unequivocal in their message that they need to see several months of moderating price pressures before easing up on rate hikes. Even then, interest rates would be held steady rather than cut until inflation is on a clear path towards the Fed’s 2% target.

They may be right. Whilst the headline rate of CPI is expected to have fallen by 0.1% month-on-month in August, pulling the yearly print further down to 8.1%, the core measure is projected to have headed in the wrong direction. When stripping out the effects of food and energy prices, CPI is forecast to have accelerated from 5.9% to 6.1% y/y in August. On a monthly basis, core CPI is expected to have increased by 0.3%, the same pace as in the prior month.

Consumption boom may have run out of steam

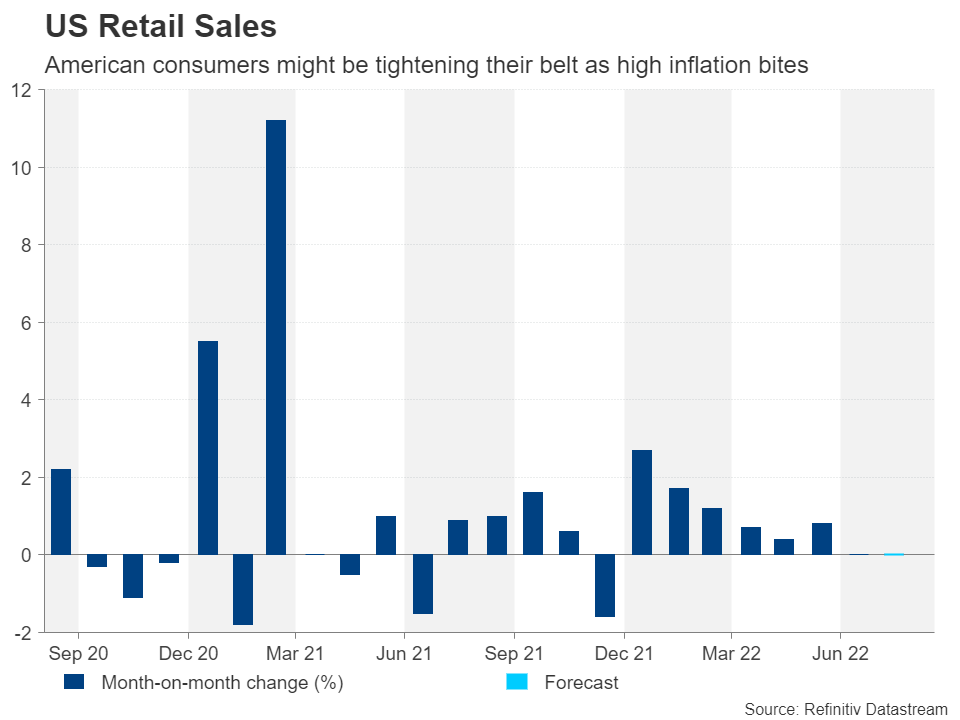

Looking at the forecasts for the upcoming retail sales numbers, there could be cause for concern about consumers finally feeling the squeeze from skyrocketing prices. Retail sales are expected to show no growth for the second straight month in August, having risen at each month this year prior to July.

But again, this isn’t likely to be a deal-breaker for the Fed just yet. In fact, reducing consumption and cooling the hot labour market are exactly what policymakers want to achieve right now as this would help in their drive to ease inflationary pressures. The jobs market in particular is far too tight still. Add to that the disappointment that financial conditions haven’t tightened substantially enough despite all the hawkish language, there can be few doubts that the Fed means it when it says the job is not done yet.

Has the dollar lost its shine?

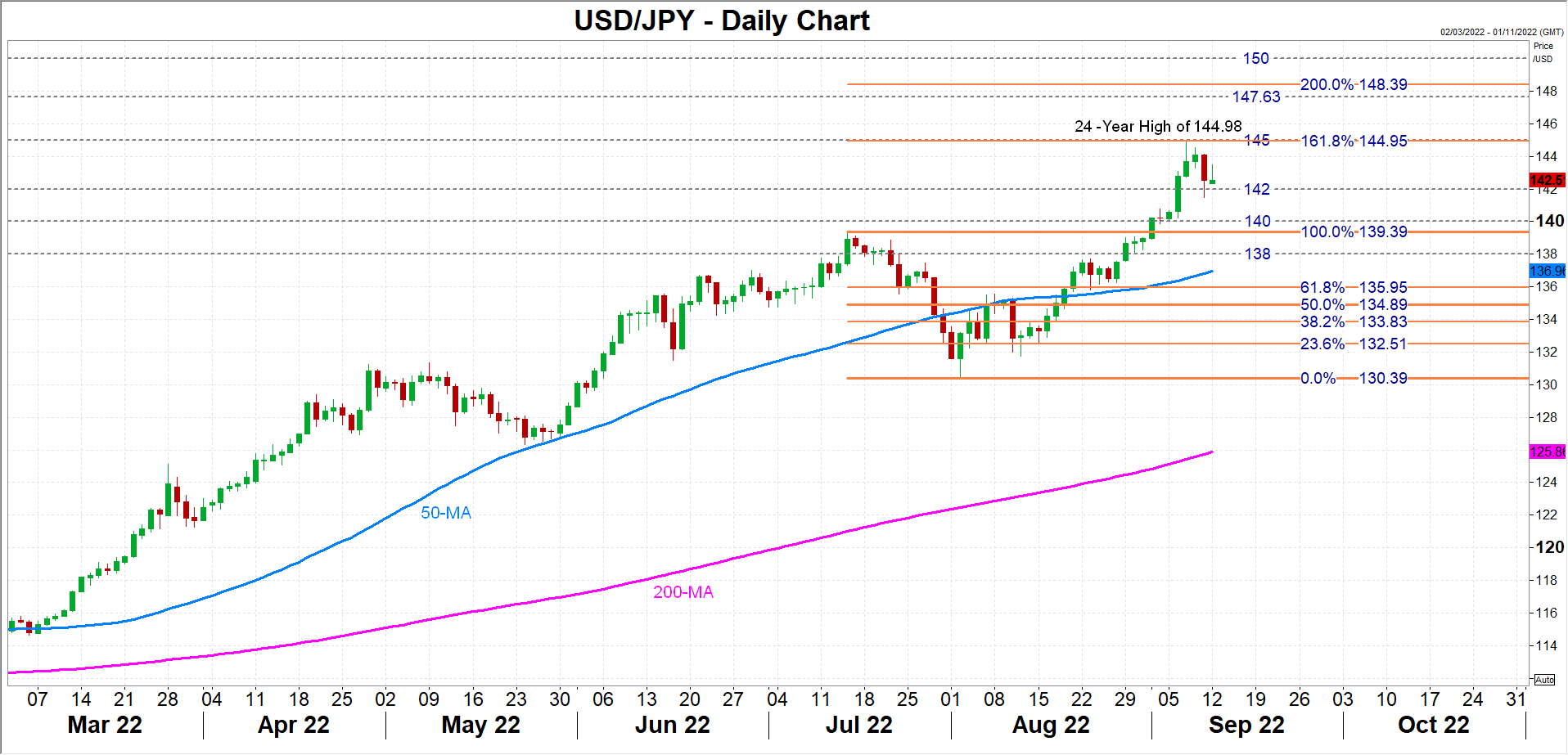

Market odds of a 75-basis-point rate hike in September have subsequently gone up to around 90%, but investors are already anticipating that the Fed will slow down after that. This may not be good news for the dollar, which has retreated from more than two-decade highs, both against the Japanese yen and against a basket of currencies.

Dollar/yen reached a 24-year high of just under 145 last week and this level is likely to again act as resistance in any renewed upward attempt as it coincides with the 161.8% Fibonacci extension of the July-August downleg. But even if that hurdle is cleared, the road to the critical 150 level will be difficult as the high of 147.63 from 1998 and the 200% Fibonacci of 148.39 stand in the way.

To the downside, the obstacles are similarly crowded, with the 142 and 140 being the nearest support areas.

All eyes on the next FOMC decision

If the August inflation report turns out to be surprisingly soft again, it’s bound to keep the greenback in consolidative mode, at least until the next FOMC decision due on September 21. Against other currencies such as the euro, the dollar could even deepen its pullback.

However, the real test will be what Chair Powell signals about the future pace of rate increases next week, whether he will confirm the market belief that the Fed will go into lower gear after September. So although it’s unlikely that the CPI data will have much bearing on the size of the September rate hike, another soft report could persuade Powell & Co. to consider toning down their hawkish rhetoric.

{kind=link}