There’s a storm of critical events this week that will shape the US dollar’s trajectory, including a speech by the Fed boss on Wednesday and the latest employment report on Friday. The Fed chief could strike a hawkish tone, while most indications suggest the US labor market is still in good shape. As for the dollar, even though the rally has stalled lately, a trend reversal is probably a story for next year.

Dollar loses its shine

It’s been a tough couple of months for the US dollar, which has surrendered almost half the gains it recorded this year, as some early signs that inflation has started to simmer down saw traders unwind bets that the Fed will push interest rates above 5% this cycle.

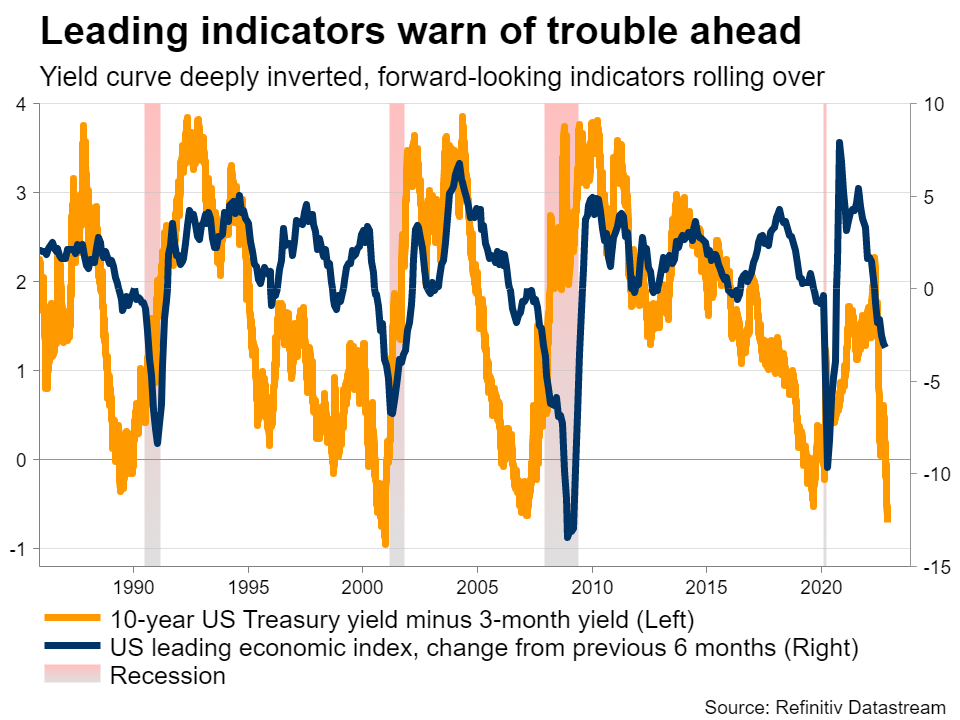

While the inflation landscape hasn’t changed so dramatically, investors seem to be placing emphasis on several leading indicators suggesting the US economy is losing steam, betting that this will prevent the Fed from raising rates much further. Gloomy business surveys, high inventory levels, a softening housing market, low consumer morale, and a deeply inverted yield curve are all classic warnings of trouble ahead.

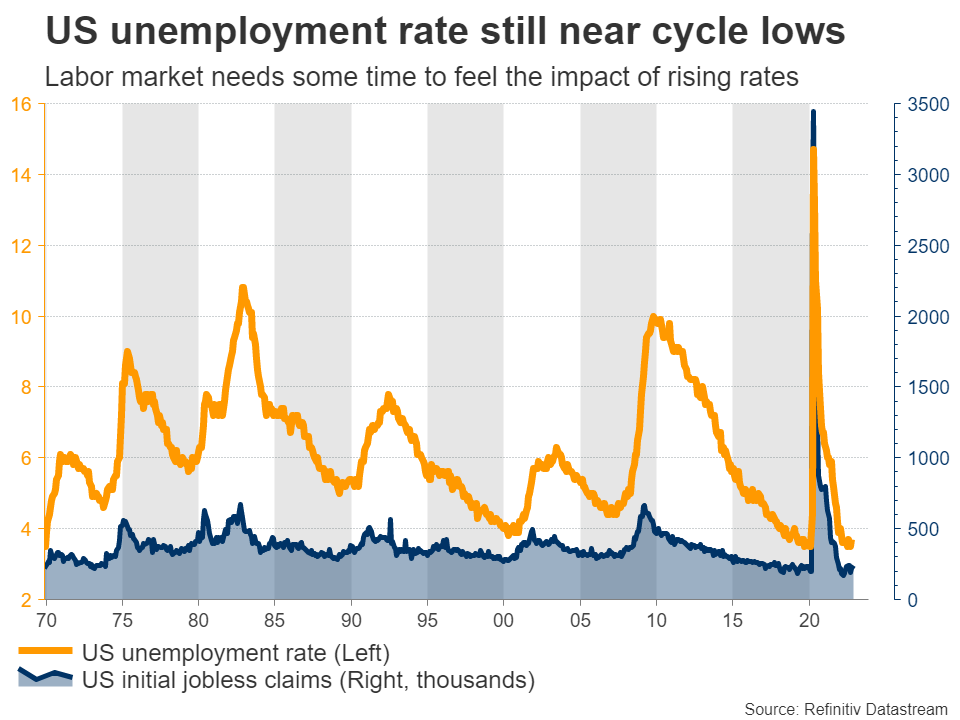

Nevertheless, this weakness hasn’t been reflected in ‘official’ data yet. Consumption remains solid, the Atlanta Fed GDPNow tracker points to annualized growth of 4% this quarter, and the labor market is still near full employment. This durability means the Fed cannot back down yet, despite mounting evidence that the economy might struggle next year.

Powell and nonfarm payrolls

This week, the show will get started with a speech from Fed chief Powell at 18:30 GMT Wednesday, where he is likely to highlight his unwavering commitment to getting inflation under control. Markets have been trading as if the inflation war has been won, with yields sliding and stocks rallying lately, which is counter-productive for the Fed as it neutralizes the impact of its rate increases.

Therefore, Powell might take the opportunity to push back and remind investors that the tightening cycle still has some ways to go, stressing that rates will stay elevated for some time. This has been the playbook all year – whenever financial conditions loosen excessively, Powell hits back.

Turning to the data, Wednesday will bring the second estimate of GDP for Q2 and the ADP jobs report for November. Then on Thursday, personal income and consumption numbers are due out, alongside the core PCE price index and the latest ISM manufacturing index. The week will conclude with the jobs report for November and the ISM services survey on Friday.

Nonfarm payrolls are expected at 200k in November, slightly softer than the 261k in October but still a healthy number overall. The unemployment rate is seen unchanged at 3.7%, while wage growth is projected to have cooled a little both in monthly and yearly terms.

Labor market indicators softened during the month, but not much. Business surveys revealed a marginal increase in workforce numbers while seekers of unemployment benefits increased a touch, albeit not enough to signal any massive disappointment in this data. It will likely take a few more months before the labor market truly feels the heat of higher rates.

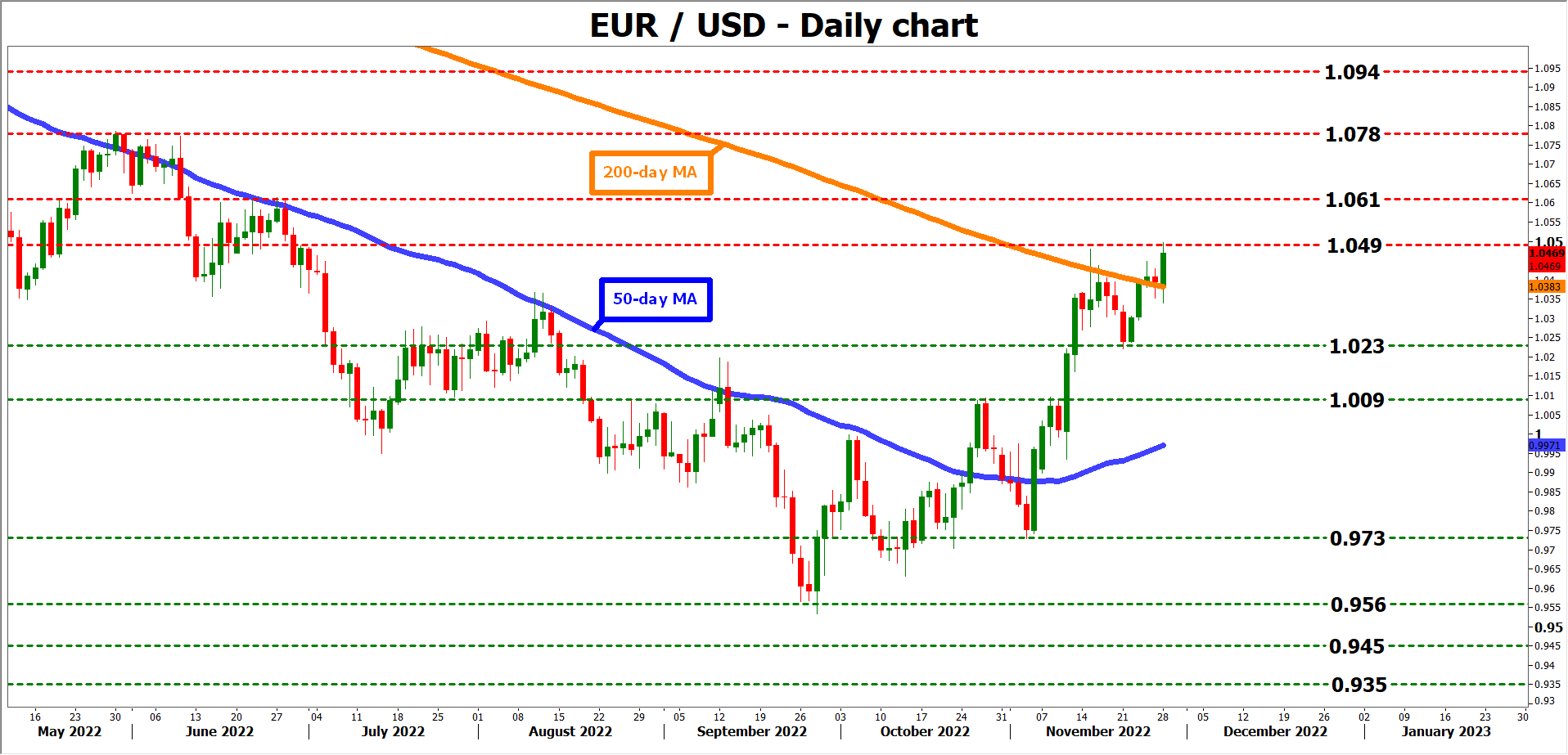

From a technical standpoint, a soft report could propel euro/dollar above the 1.0490 region, opening the door towards 1.0610. On the other hand, another solid dataset might pressure the pair lower, with the first major support barrier being the 1.0230 zone.

Dollar reversal?

All told, even though some of the elements that fueled this ferocious dollar rally seem to be losing their kick, for instance with US inflation cooling off, it is still too early to call for a proper trend reversal.

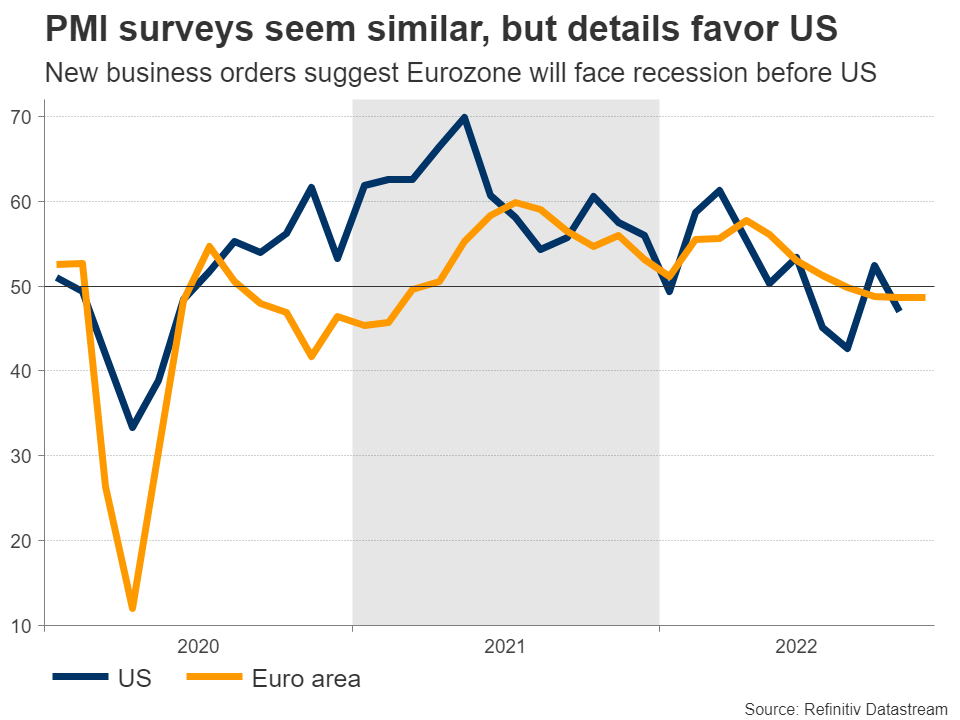

The argument is simple – other major economies such as the Eurozone and United Kingdom will probably fall into recession long before America does. Business surveys suggest these economies might be in a downturn already, while the US likely needs a few more quarters to get there thanks to its resilience to the energy shock.

Historically speaking, powerful dollar rallies don’t end while the outlook for global growth is deteriorating, as safe-haven flows keep the reserve currency in demand. Hence, while this rally seems to be entering its final chapters, the prospect of a reversal remains premature for now, and possibly a story for next year.

{kind=link}