The September U.S. employment report (08:30 am EDT) should be affected by the impact of Hurricanes Irma and Harvey in late August.

The median forecast for this morning’s release is a +80k gain in non-farm payrolls, less than half the average +182k monthly rise since the start of last year and an unemployment rate of +4.4%.

Note: U.S state by state data due near the end of this month will be able to strip out that impact for the rest of the country.

The ‘mighty’ U.S dollar is expected to carry on as usual, even though the headline number is expected to be much smaller. Beyond a headline shock, the consensus is anticipating the implication and knee-jerk reaction for bonds and FX should be muted and indeed short-lived as the Fed is expected to look though the fall and continue with its policy normalization.

However, if the headline print comes in on the strong side, it should inspire “bullish investors” in the U.S dollar, and potentially push the dollar index to new highs.

Fed fund futures are pricing in a +78% probability that the Fed will hike interest rates by the end of the year, up from around +44% last month.

Elsewhere, Canada will also release its employment report at 08:30 am EDT. Dealers are looking for a headline print of +13k and the unemployment rate to tick up a tad to +6.3%.

1. Stocks in the black

In Japan, the Nikkei share average scaled a fresh two-year peak on Friday and posted its fourth straight weekly gain, buoyed by the impact of a weaker yen (¥113.05) as well as record highs on Wall Street. The Nikkei ended +0.3% higher. For the week, it added +1.6%, while the broader Topix was up +0.2%.

In Hong Kong, the benchmark stock index closed at its highest level in a decade Friday, supported by Chinese automakers and banks. The Hang Seng index rose +0.3%. On the week, the index rose +3.3%, its biggest such gain in three-months. The China Enterprises Index rallied +0.5%, its highest close since mid-2015. It ended up +5% for the week, the best in six-weeks.

Note: The Shanghai Composite and Korea Kospi remained closed for Golden Week.

Down-under, S&P/ASX closed out the week up +1.04%, mostly supported by ‘dovish’ comments from RBA’s Harper on potential rate cuts.

In Europe, regional bourses have opened mixed with peripherals once again under pressure; banks with exposure in Catalonia are especially impacted. U.K’s FTSE 100 is being supported by weakness in sterling (£1.3073).

U.S stocks are set to open in the red (-0.5%).

Indices: Stoxx50 -0.2% at 3,604, FTSE +0.1% at 7,518, DAX +0.1% at 12,974, CAC-40 -0.2% at 5,370, IBEX-35 -0.7% at 10,144, FTSE MIB -0.8% at 22,393, SMI +0.2% at 9,280, S&P 500 Futures -0.05%.

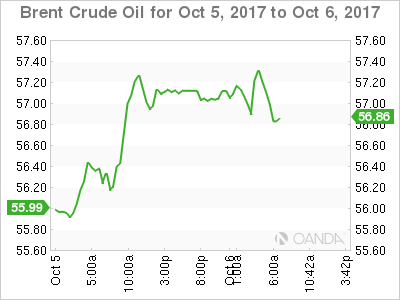

2. Oil markets wary as a storm heads for Gulf of Mexico, gold lower

Oil markets remain cautious as traders monitor a tropical storm heading for the Gulf of Mexico.

However, the prospect of extended oil production cuts by OPEC and non-OPEC members is providing some underlying support.

Brent crude futures are down -12c at +$56.88 a barrel, while U.S light crude (WTI) is trading at +$50.63 per barrel, down -16c from Thursday’s close.

Tropical storm Nate heading for the Gulf of Mexico has triggered U.S Gulf production and refinery closures just weeks after several hurricanes pummelled the region.

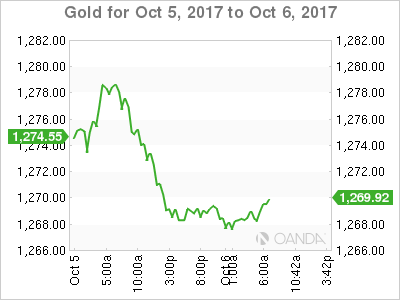

Ahead of the U.S open, gold has hit its lowest print in nearly two-months in range-bound trade, as the ‘mighty’ dollar climbs to a two-month high ahead of today’s jobs data.

Spot gold is at +$1,267.71 an ounce, after hitting its lowest since Aug. 9 earlier in the session. It is down -0.9% for the week and is heading for a fourth straight weekly decline.

3. Yield differentials the name of the game

10-year Spanish government debt is broadly unchanged in early Friday trade as they continue to benefit from Thursday’s well-received debt auction. Fixed income dealers say the auction may have “signaled a turning point in the mood toward Spanish debt” after its losing streak following Sunday’s Catalan independence vote. The 10-year Spanish bond yield trades at +1.70%, about +9 BPS up from the Sept. 29 close, the last trading session before last weekends ‘illegal’ referendum.

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more ‘hawkish’ successor to Fed Chair Janet Yellen is helping to support higher U.S yields. The yield on 10-year Treasuries have gained +2 bps to +2.36%, the highest in more than three-months.

In Germany, the 10-year Bund yield has climbed +3 bps to +0.48%, the highest in more than two-months, while in the U.K, the 10-year gilt has advanced +3 bps to +1.414%, the highest in eight-months.

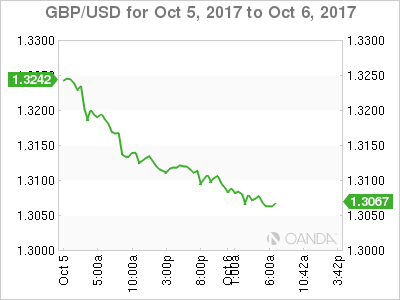

4. Pound under Political Pressure

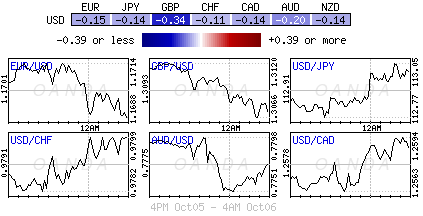

U.K’s political uncertainty has sent the pound to three-week lows against the USD and EUR on reports that a group of Conservative MPs are calling for Theresa May to quit as Prime Minister. This threat is now posing market doubts on whether the Bank of England (BoE) would hike rate in November. GBP/USD is down -0.4% to £1.3060, while EUR/GBP has rallied to €0.8956.

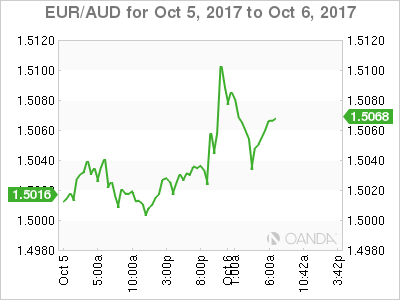

The EUR is little changed after the release of the ECB minutes yesterday, which gave little detail on plans to scale back asset purchases under QE. The EUR/USD trades atop of €1.1700, little changed from Thursday’s close. The minutes said ECB officials discussed how to scale down their giant bond-buying program at their September policy meeting, but said policy makers want to proceed “in a very gradual and cautious manner.” They expressed some concern about weak inflation and disagreed on the reasons for the recent appreciation of the EUR.

Down-under, following yesterday’s Australian retail sales induced declines (-0.6% vs. +0.3% m/m); the AUD has again struggled in the overnight session (A$0.7763) after RBA official Harper surprised the market with his statement that the central bank did not rule out a rate cut amid the weaker retail sales data. The RBA last cut rates in Aug 2016.

5. Italian retail trade disappoints

The value of Italian retail trade decreased by -0.3% in August 2017 compared with the previous month (-0.4% for both food goods and non-food goods) and decreased by -0.5% compared with August 2016 (+0.8% for food goods and -1.5% for non-food goods).

Despite short-term variability, the underlying pattern in retail trade remains flat as in the three months to August 2017 the value is estimated to have decreased by -0.1%, whilst the volume is estimated to have increased by +0.1%.

The volume of retail trade decreased by -0.4% compared with July 2017 (-0.4% for food goods and -0.5% for non-food goods) and decreased by -1.0% from the same month a year earlier (+0.0% for food goods and -1.8% for non-food goods).

Note: Looking at year-on-year change, retail trade sales were up +1.4% in large-scale distribution and down -2.4% in small-scale distribution.