Forward Guidance will be on vacation next week, Happy Holidays!

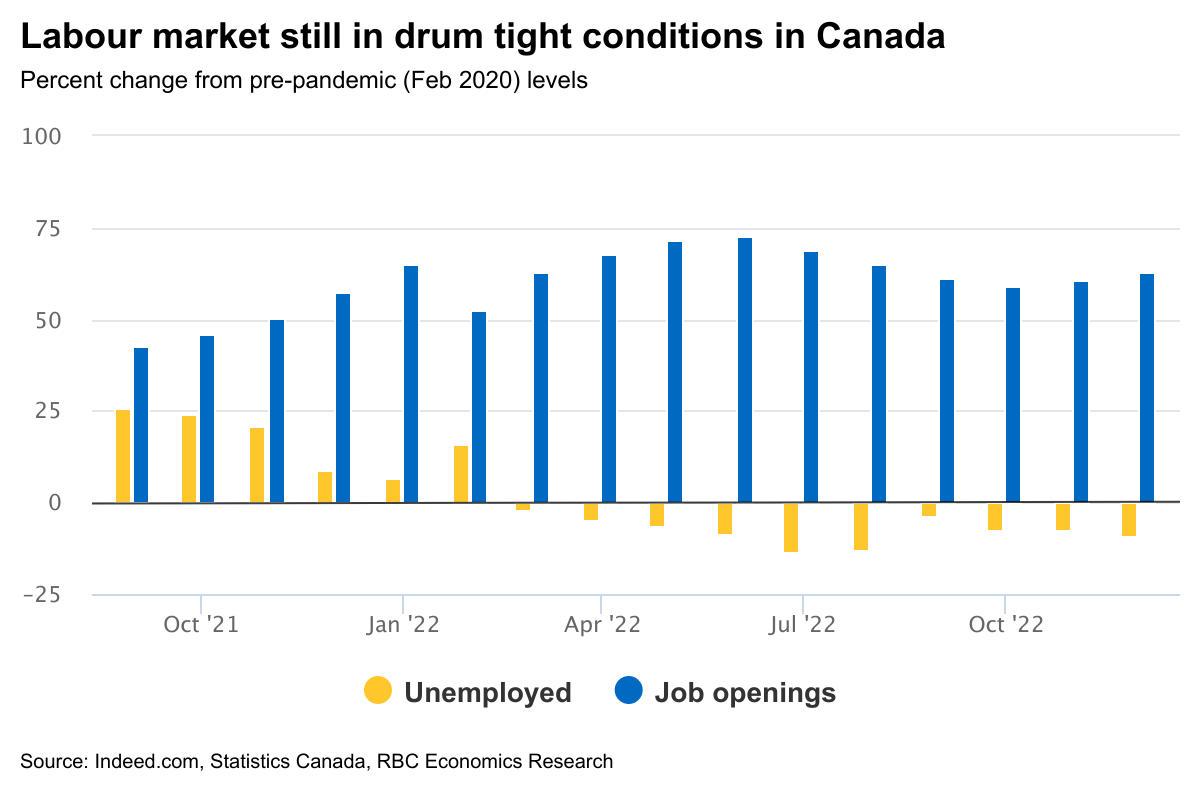

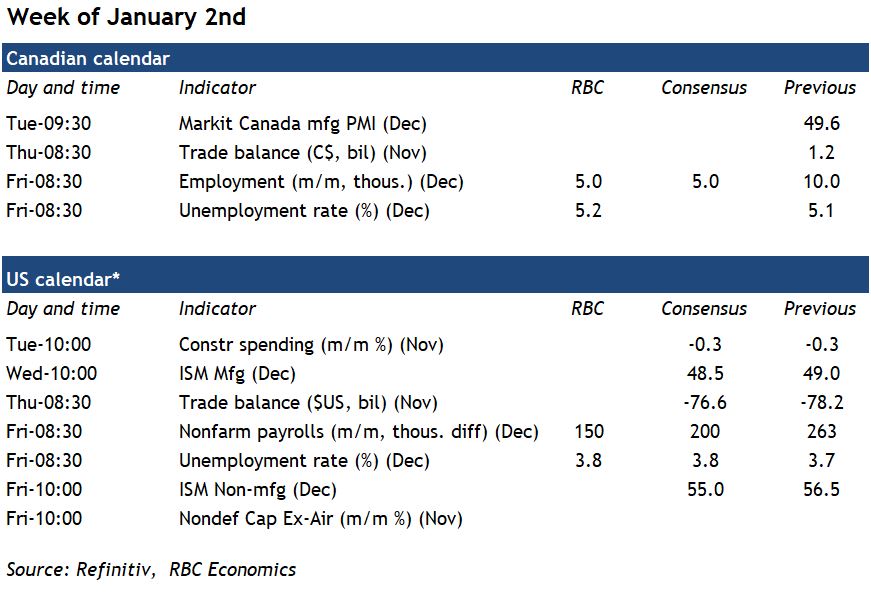

A quiet Christmas holiday week will have few economic data releases in North America. But the first week of 2023 will kick off with December labour market reports for the U.S. and Canada. Labour shortages are still a bigger issue than a lack of hiring demand in both economies – job openings continue to run well-above pre-pandemic levels and unemployment rates are still very low. Still, there have been early signs of softening in the outlook and we look for the Canadian unemployment rate to tick up to 5.2% on a soft 5k increase in employment. Employment growth in Canada has been volatile, but essentially flat on average over the last 6 months with declines over the summer offset by gains in October and November. The unemployment rate has ticked up from the record low (dating back to at least 1976) 4.9% earlier in the summer but is still well-below pre-pandemic levels. As a result of tight labour market conditions, wage growth has been accelerating. Average hourly earnings growth from a year ago ticked up to 5.6% in November. But we continue to expect inflation and the lagged impact of the aggressive interest rate hikes of 2022 to cut into household purchasing power and slow hiring demand in the New Year.

Job growth has been more resilient in the United States – and we look for another 150k positions to be added in December. But, there too, the pace of improvement has been slowing and the unemployment rate has ticked up from summer lows. There is still substantial momentum near-term in labour markets with the level of job openings still very high. But hiring demand will slow in 2023 as higher interest rates begin to slow the economy down more significantly.

Week ahead data watch

The Canadian international trade surplus likely narrowed in November. A 3% pull-back in oil prices will lower the energy trade balance and a stronger Canadian dollar will lower the prices of both exports and imports in Canadian dollar terms. Imports of equipment (a key indicator of domestic business investment) will be watched closely after a sharp decline in October.

{kind=link}