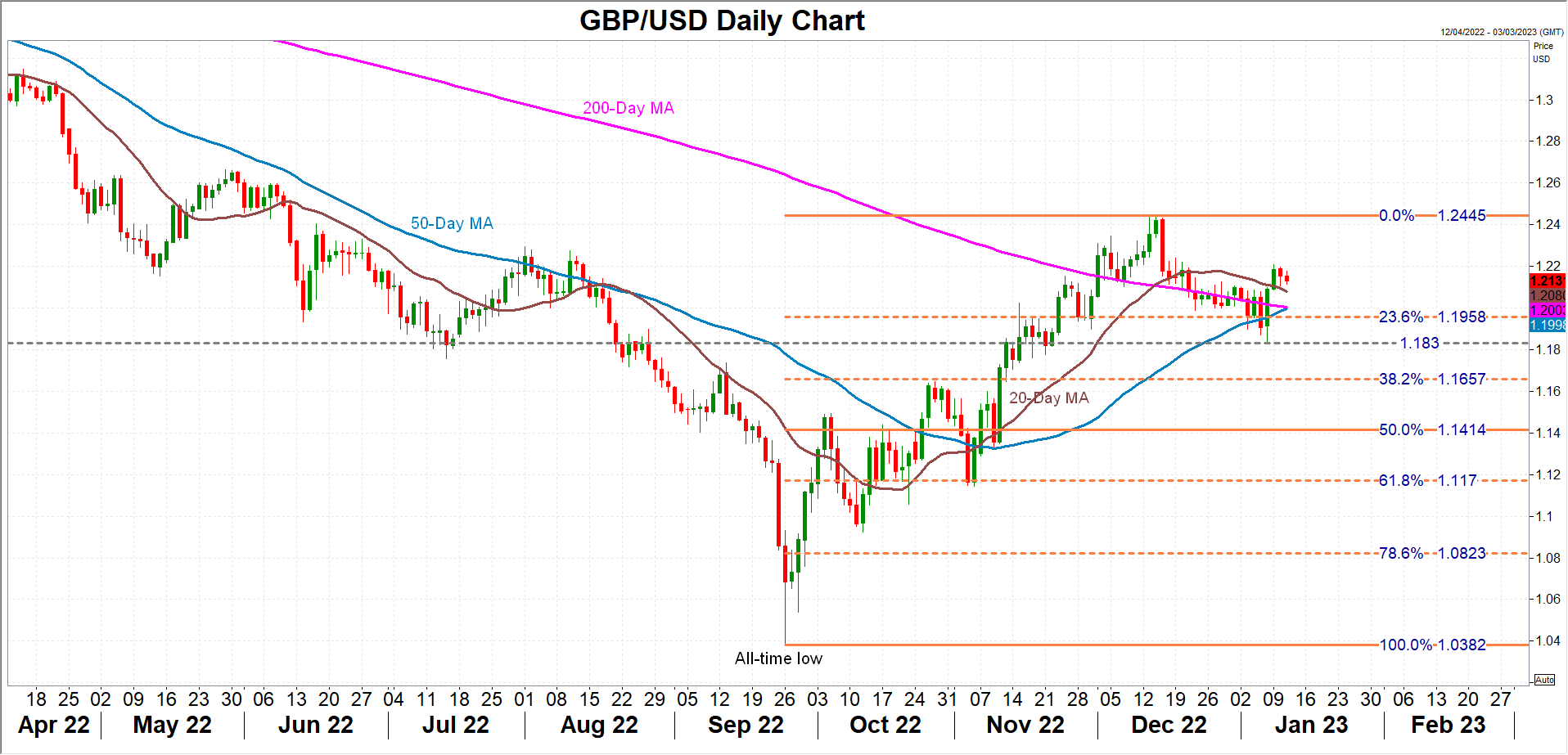

Britain’s economy has been on the receiving end of some of the more pessimistic forecasts around for 2023 and Friday’s data dump, due at 07:00 GMT, isn’t anticipated to lift any of the gloom. The monthly output indicators will likely show that the economy went back into contraction in November, even as the Bank of England is expected to hike interest rates by another 50 basis points at its next meeting in February. A poor set of data could scupper the pound’s chances of a meaningful rebound as it struggles to get its three-month old uptrend back on track.

From crisis to crisis

It’s been a tough year for UK assets as, fresh out of the pandemic, the country was hit by the energy crisis, spurred by the war in Ukraine. This was then followed by political turmoil where investors lost count of the residents moving in and out of numbers 10 and 11 Downing Street. Whilst it is easy to dismiss the happenings at Westminster over the summer and autumn as nothing more than political drama, the damage inflicted to investor confidence towards the UK economy may outlast the effects of the energy crisis.

Thanks to a relatively mild winter season, worries about a severe energy crunch have not materialized and are not likely to either, at least not this winter. But the UK’s troubles don’t end there as public sector discontent over pay has led to a series of strike actions across the country, with the government being blamed for refusing to negotiate new pay deals. The affected sectors range from transport to the civil service to hospitals.

Grim forecasts

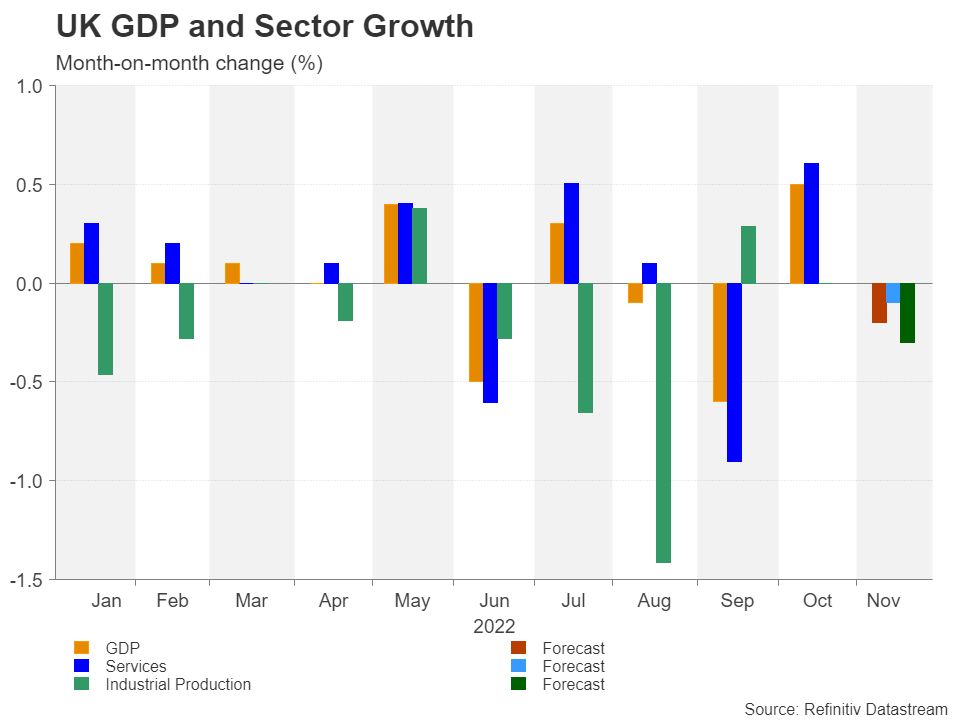

The disruptions are bound to cause a significant dent in GDP output in December, meaning that if the forecasts of negative growth in November turn out to be correct, the UK will almost certainly record two consecutive quarters of contraction, placing it in a technical recession.

For November, the projections are pretty grim. Both services and industrial output are expected to have shrunk over the month, by 0.1% and 0.3%, respectively. Overall output is anticipated to have fallen by 0.2%, reversing some of the 0.5% bounce enjoyed in October.

Confidence in the UK is at a low

Some small upside surprises cannot be ruled out in November’s data, but given that GDP has barely grown in the last 12 months, whether there’s still a chance that the UK can avoid a technical recession is unlikely to change the view that the economy has stagnated. The lack of business and economic leadership from the government is a major source of worry for investors, not to mention the increasing tax burden. Thus, when you take out the weakening US dollar out of the equation for cable, the pound doesn’t have much going for it at the moment.

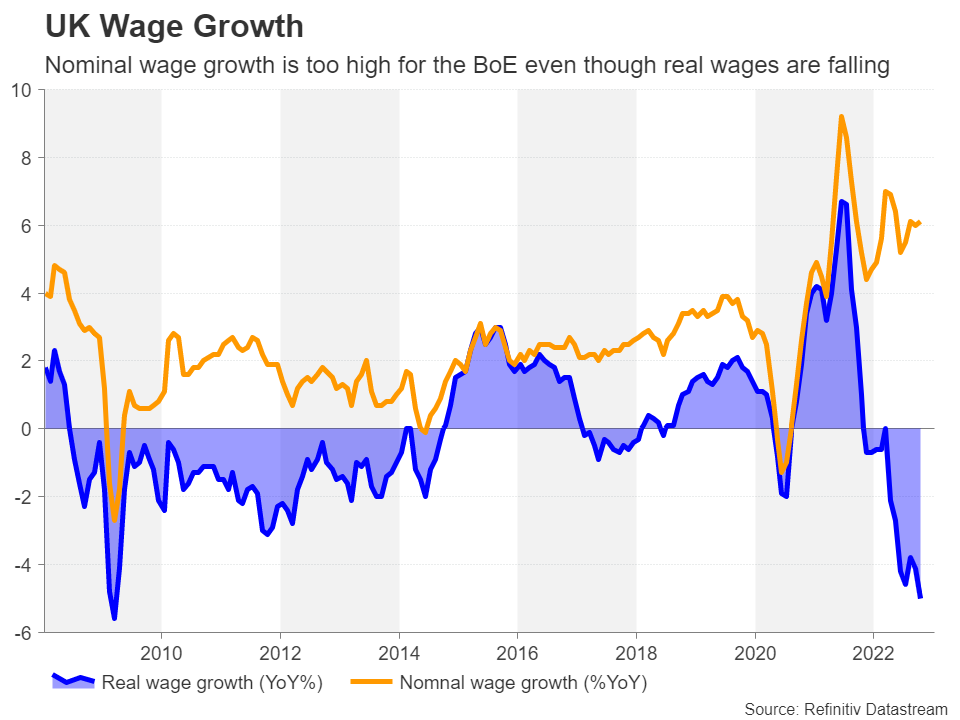

The cost-of-living crisis seems to be hurting UK consumers more than those in other advanced economies. Brexit has had some part to play in this as certain import prices rose after leaving the single market, labour shortages have worsened and exports to the EU have taken a hit. But perhaps the biggest concern is the bleak prospect for consumer spending in 2023. Consumption is the most important engine of economic growth in Britain and as long as households are being squeezed by high inflation and falling real wages, a recovery doesn’t seem imminent.

Squeeze on households could continue well into 2023

In fact, things could get worse in the coming months as rising interest rates push up mortgage costs further and many households currently on fixed mortgages are set to see their installments jump when their fixed-rate loans come up for renewal.

On the plus side, the Bank of England appears to more than recognise the risks that higher rates pose to households with rising mortgages. But at the same time, policymakers might have their hands tied from the tight labour market.

The UK’s labour pool has shrunk in the aftermath of Brexit and the pandemic and unless the government relaxes immigration rules, worker shortages in specific sectors could persist even as the jobless rate ticks higher. The Bank’s chief economist, Huw Pill, warned on Monday that wage pressures and supply-chain problems could make it more difficult for inflation to drop to 2% despite the substantial retreat in energy prices.

Can cable extend its uptrend?

Nevertheless, in the short term, traders might still find cable an attractive buy as long as the dollar stays on the backfoot and there are some positives in the November stats. Having just cleared the obstacles set by the moving averages, the bulls are likely to set their sights on the $1.2445 resistance where the uptrend stalled in mid-December in such a scenario.

However, if Friday’s data disappoint, amplifying concerns about the UK’s economic prospects, the pound could revisit its recent low of $1.1830. If breached, the 38.2% Fibonacci retracement of the September-December upleg could be the next major support at $1.1657.

{kind=link}