Summary

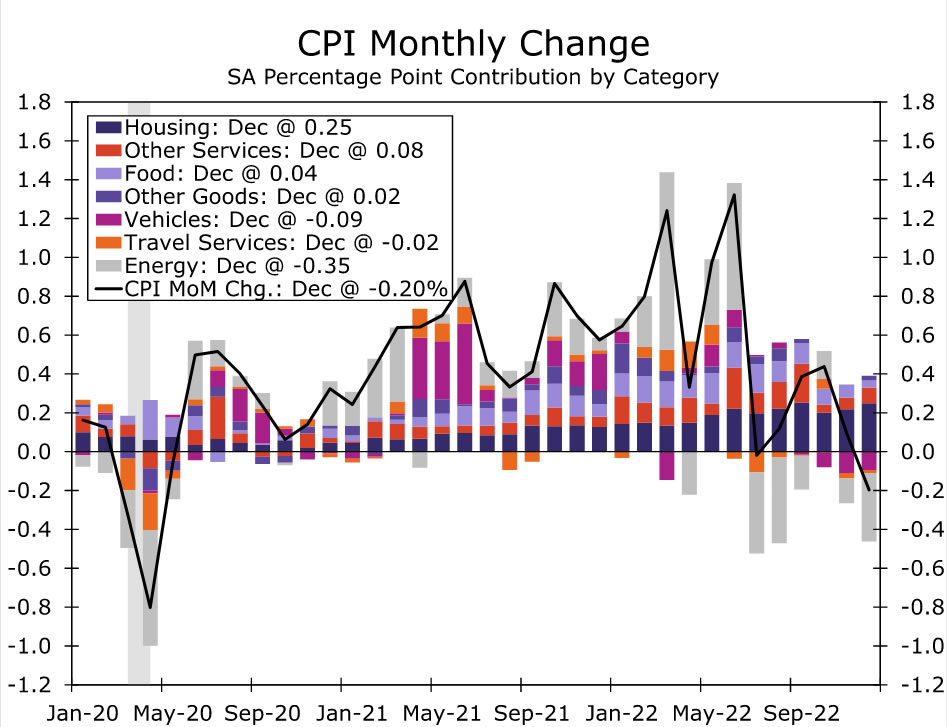

Inflation continued to ease in December. The headline CPI fell 0.1% in the month, and December marked the third consecutive increase in the core index of 0.3% or less. A major decline in gasoline prices helped keep headline inflation in check, but the signs of slower inflation extended beyond prices at the pump. Grocery store prices grew at the slowest pace since March 2021, and core goods prices declined for the third consecutive month, led lower by another decline in prices for used autos. Services remained the hottest inflation category. Prices of core services rose 0.5% in December, led higher by a sizable 0.8% increase in shelter costs.

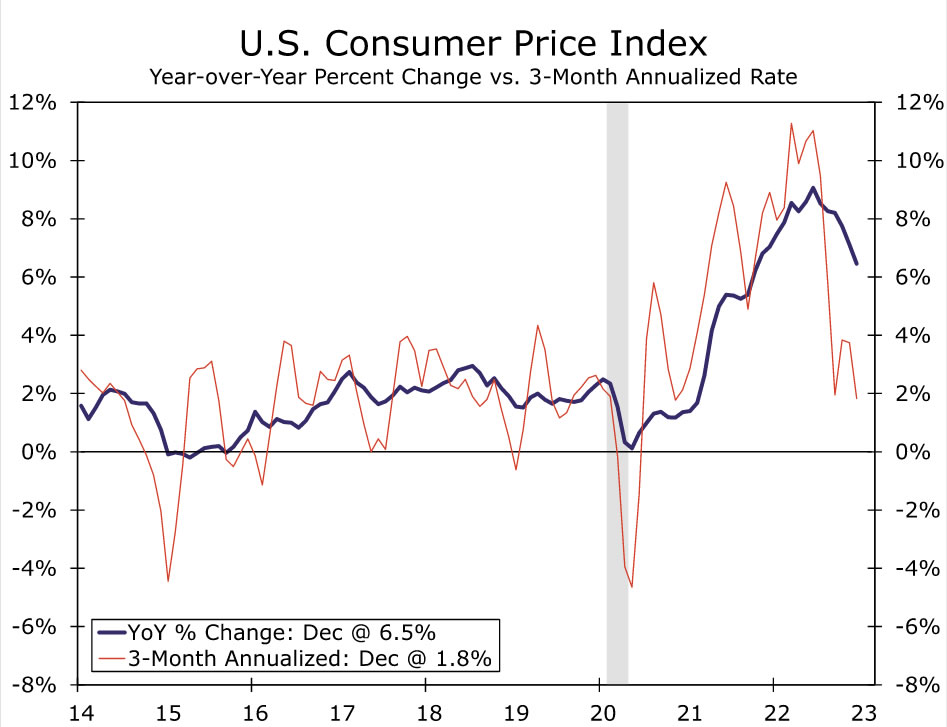

Inflation clearly has slowed from its breakneck pace in mid-2022. Headline inflation has fallen by 2.6 percentage points since June, and the annualized run rate over the past three months is just 1.8%, demonstrating further slowing is still to come in the year-ago change. Additional progress should be made in the coming months as goods inflation remains soft and the lagged effect of slower housing cost growth eventually flows through to the CPI data. As a result, the days of 75 bps rate hikes from the FOMC appear to be well in the rearview mirror.

That said, we doubt the FOMC is ready to declare mission accomplished. There have been head fakes on inflation before, to no avail, and there is a wide range of inflation outcomes between the peaks seen last summer and the central bank’s 2% inflation target. Eventually the goods price deflation will cease, and labor cost growth continues to run in excess of what Fed officials believe is consistent with 2% inflation. The increasingly compelling evidence of slowing inflation brought by today’s report ups the chance that the FOMC will hike the fed funds rate by just 25 bps at its next meeting, but with the trend in inflation still above target, we expect that even if the FOMC delivers a downshift in pace, it will continue tightening past its next meeting.

Energy, Food, Goods Prices Keep Normalizing

The Consumer Price Index (CPI) fell by 0.1% in December, matching the Bloomberg consensus forecast and marking an albeit modest month of deflation to finish 2022. It was a narrowly-driven decline with major deflationary contributions from gasoline and used autos. Gasoline prices declined 9.4% in December and were down 1.5% compared to a year-ago. Energy services inflation surprised to the upside, led higher by monthly price increases of 1.0% and 3.0% for electricity and utility gas, respectively. Food inflation continued to cool. Prices at the grocery store increased 0.2% in December, the smallest monthly increase since March 2021. Prices for food-away-from-home rose a faster 0.4% in the month but also decelerated from the previous few months.

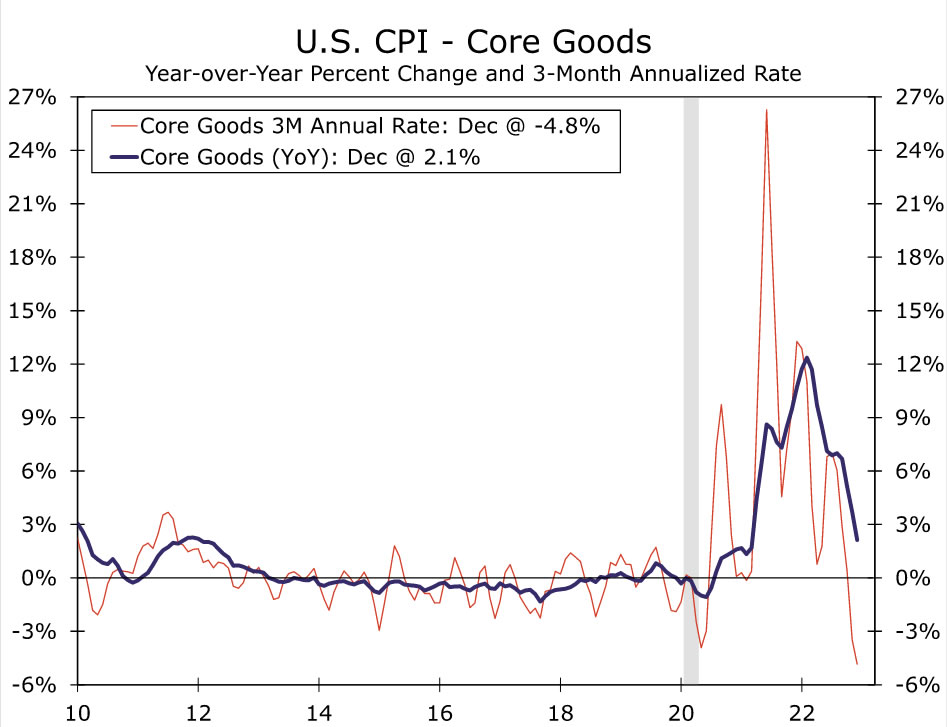

The normalization of prices in sectors that were distorted by the pandemic mostly continued. Core goods prices fell by 0.3% in December, the third consecutive month of deflation for this category. Prices for used cars and trucks fell another 2.5% and are now down 8.8% on a year-over-year basis. New vehicle prices declined a much more modest 0.1%, while a few categories such as apparel (+0.5%) posted upside surprises. Several travel-related categories also experienced another bout of deflation in December including airfares (-3.1%) and car rentals (-1.6%). Lodging away from home was the outlier in travel, posting a 1.5% increase.

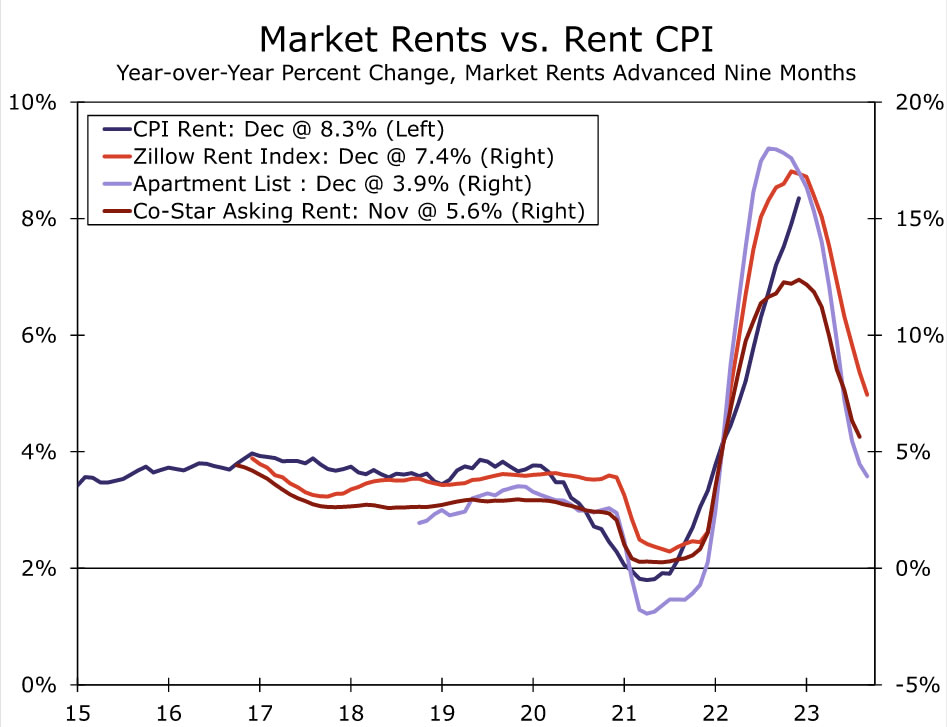

Prices of core services, on the other hand, continued to advance at a strong clip, rising 0.5% in December. A rebound in hospital services and smaller drop in health insurance drove a pickup in medical care services. Surprising in our view were stronger gains in primary rent and owners’ equivalent rent, both up 0.8% on the month. Given the sharp slowdown in private sector rent measures and more recent declines in home prices, we do not expect the strength to last, however, and we look for sequential gains to trend lower imminently.

Elsewhere, details continued to suggest core services inflation is at least not getting worse. While the various ways to slice and dice the traditional core may at times be going a bit overboard, core services ex-shelter rose a tame 0.2% in December. In addition to the declines in airfare and car rental costs, price growth for recreation services, education/communication services and vehicle insurance all slowed.

Progress Made, but the War Is Yet to Be Won

Stepping back, the inflation picture is vastly improved from where it was in the middle of last year. Headline inflation has fallen by 2.6 percentage points since June, and the annualized run rate over the past three months is just 1.8%, demonstrating further slowing is still to come in the year-ago change.

We see scope for both headline and core inflation to quickly cover additional ground in its march back to 2% over the coming months. Some giveback in goods prices seemed inevitable after the stratospheric rise of the past two years, and that time seems to have finally come. Retail inventories have piled up as demand for goods has flat-lined and supply chain kinks have unwound. Even the hard-hit auto sector appears to have reached an inflection point, with inventories rising and transaction prices squeezed by higher financing costs (one sign the Fed’s policy tightening is helping to reduce inflation). Similarly, the pace of shelter inflation seemed destined to ease after the housing market frenzy finally fizzled, and the turn is drawing increasingly near.

But, the weakening in goods prices and even shelter costs needs to be viewed in conjunction with more labor-intensive services. We suspect core services excluding shelter, which accounts for nearly one-third of the core index, will prove more stubborn to improve given the longer lag with which input cost changes are incorporated. Labor costs are still rising at a 4-5% clip which is one to two percentage points faster than the pre-pandemic pace. While Fed officials have acknowledged the recent progress and should welcome this report, like us, they remain skeptical that inflation will easily settle back down to 2% past the correction in goods and housing. The increasingly compelling evidence of slowing inflation brought by today’s report ups the chance that the FOMC will hike the fed funds rate by just 25 bps at its next meeting, but with the trend in inflation still above target, we expect that even if the FOMC delivers a downshift in pace, it will continue tightening past its next meeting.

{kind=link}