Bank of England Preview – Topside risk to EUR/GBP

- We expect the Bank of England (BoE) to hike the Bank Rate by 50bp.

- We pencil in an additional 25bp hike in March, now expecting the Policy Rate to peak at 4.25% in March 2023.

- Dovish communication from BoE should send EUR/GBP higher during the day.

BoE call. We expect the Bank of England (BoE) to hike the Bank Rate (Policy Rate) by 50bp on 2 February bringing it to 4.00%. Markets are currently pricing 45bp for the meeting next week. Importantly, we consider it a closer call between 50bp and 25bp than what markets are pricing and the distribution of analyst expectations would suggest. That said, we believe the latest data releases support a continued forceful response by the BoE which favours a slightly more aggressive 50bp hike compared to the 25bp alternative.

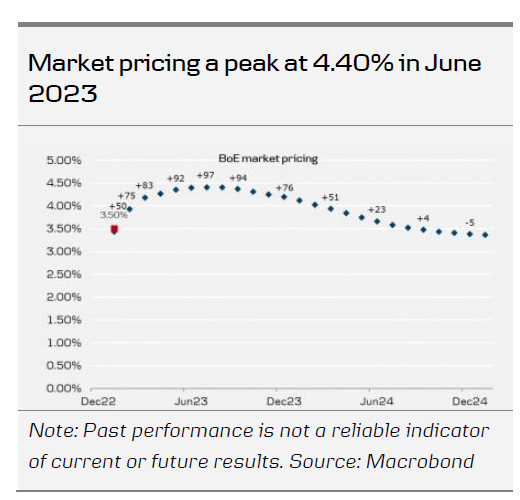

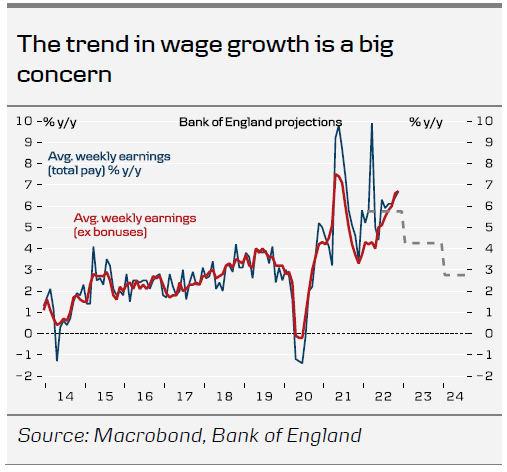

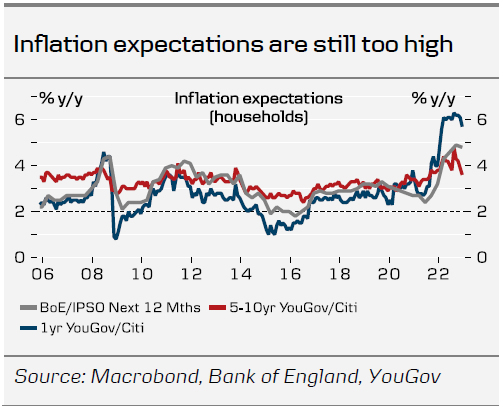

Since the last meeting in December, data has shown further persistent inflationary pressures as well as a more resilient UK economy. Wage growth has surprised to the upside reaching 6.41% in November, whereas the BoE in their November projections estimated wage growth at 5.75% for Q4. Likewise, core CPI remained unchanged at elevated levels, headline inflation fell less than expected and GDP growth came in stronger than expected. As highlighted in the December minutes, the BoE is particularly concerned about the tightness of the labour market and the pass-through to domestic prices and wages. This is an important reason why we think a majority of the MPC will vote for a 50bp February hike. Likewise, we expect the central bank’s updated projections to show a relative improved economic outlook as market pricing for policy input has come significantly down since the last meeting (from peak 5.25% to peak 4.40%) which supports our case for 50bp.

Additionally, we extend our current forecast to include a final hike of 25bp in March this year, forecasting a peak in the Bank Rate at 4.25%. This is still fewer hikes than priced in markets (currently 90bp until June 2023). We expect BoE to return to its more dovish stance as recession risks should start to be more pronounced as the growth outlook continues to become weaker. We do, however, not expect cuts to materialise before 2024.

Growth outlook. The UK economy might avoid negative GDP growth in Q4 2022 due to stronger than expected growth during October and November, while data gives weak signals for December. This, however, does not mean that the UK economy will avoid a recession, but merely that it will come later than originally pencilled in. Inflation continues to be substantially above target and despite a seeming peak in October last year, core inflation remains resilient. This is also reflected in retail sales figures, which took a hit during December. While the labour market remains tight, unfilled vacancies have continued to come lower and survey indicators as PMI’s are showing the first signs of easing.

FX. In our base case of a dovish 50bp hike, we expect EUR/GBP to move slightly lower upon announcement, but reverse higher on the back of a dovish statement and press conference. In its statement we expect the BoE to highlight the dire state of the UK economy lending support to our call that market pricing is too aggressive currently pricing a peak in the Bank Rate at 4.40% by June 2023. Combined with the expectation of a hawkish 50bp hike by the ECB later in the afternoon, we expect EUR/GBP to move higher during the afternoon, ending the day ca. ½ figure higher than the opening levels

{kind=link}