Summary

- While there have been some mildly encouraging developments in the recent U.K. data flow, the outlook for the British economy remains distinctly subpar. A flat Q4 GDP outcome has been followed by improving confidence surveys early this year. However, with prior price increases likely to pose lingering challenges to household purchasing power, we still forecast U.K. GDP to contract 0.6% in 2023.

- There has also been some improving news on the inflation front, which decelerated more quickly than expected in January at both the headline and the core levels. We view this as a noteworthy development, given the backdrop of the rapid slowing of inflation forecast by the Bank of England (BoE) over the medium-term and some dovish comments from important central bank policymakers.

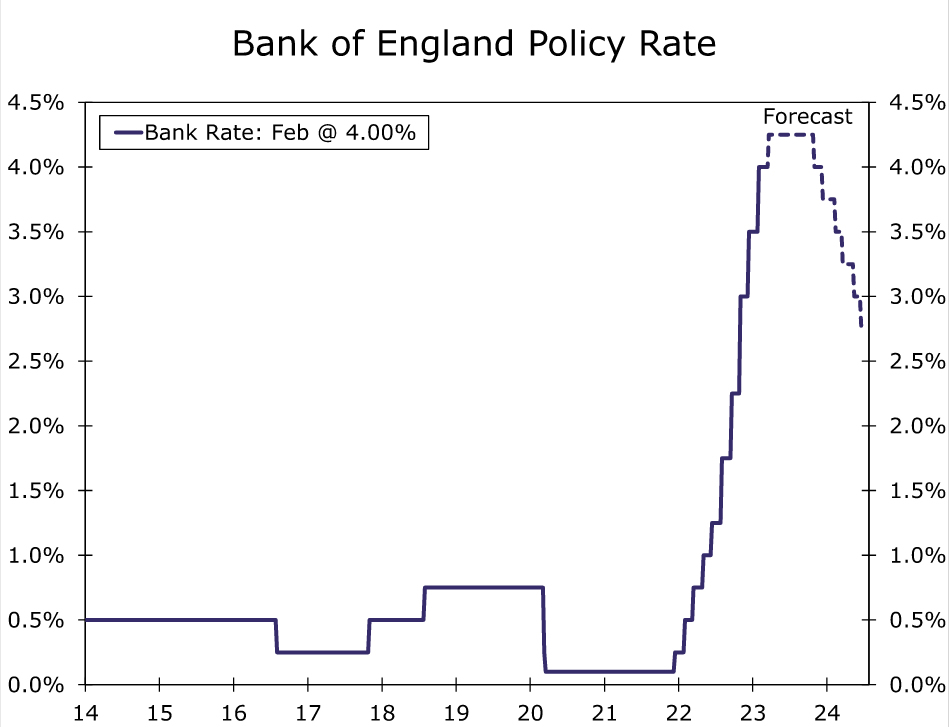

- Should inflation continue to show a pronounced declaration, and activity and survey data show renewed softening, we expect the Bank of England to deliver a final 25 basis point rate to 4.25% in March and to begin cutting interest rates as early as Q4 of this year.

- Our forecast policy rate peak is well below the level implied by current market pricing. The less aggressive approach we envisage from the BoE is an important reason we expect that, over the medium-term, the pound will be an underperformer against a broadly soft U.S. dollar, targeting a GBP/USD exchange rate of just $1.2200 by the end of this year. The BoE’s less aggressive approach should also contribute to some decline in two and ten year U.K. government bond yields from current levels over time.

U.K. Economic Outlook Still (Somewhat) Underwhelming

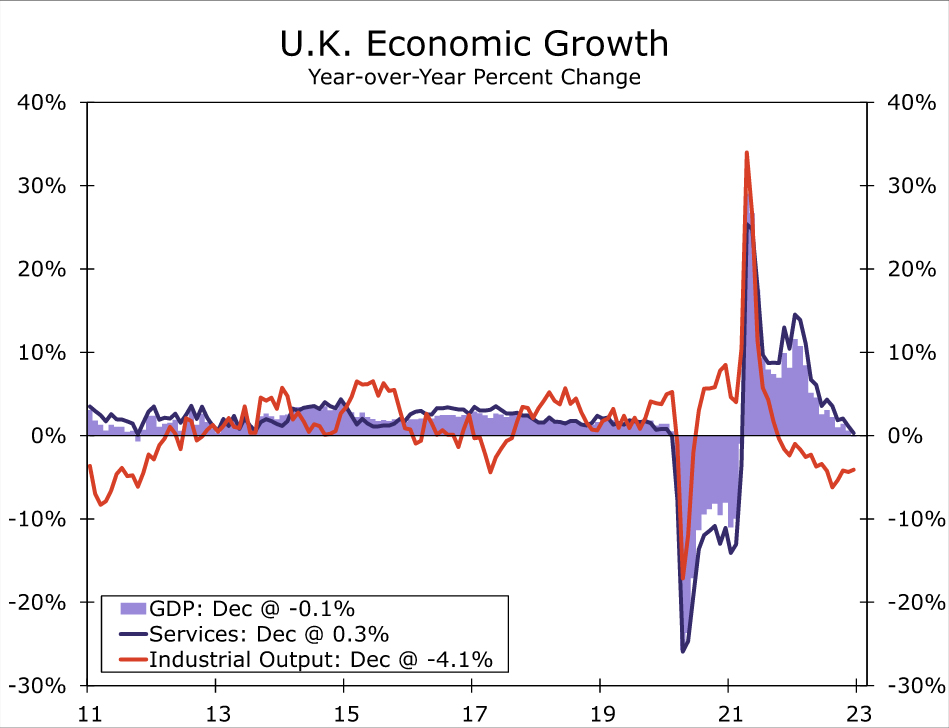

Although there have been some mildly encouraging developments in the recent U.K. data flow, the outlook for the British economy remains distinctly subpar. The U.K. has narrowly avoided recession, for now, with the release of its fourth quarter GDP figures. Q4 GDP was flat for the quarter, with the details showing consumer spending edging up 0.1% and business investment jumping 4.8%. While the economy held steady for quarter as a whole, the economy did finish 2022 on a soft note as U.K. December GDP dropped 0.5% month-over-month, driven by a 0.8% decline in services activity as industrial output rose 0.3%. The Q4 GDP report also suggested that high inflation could pose some lingering challenges to household purchasing power in the months ahead. After adjusting for higher prices, we estimate that U.K. real employee compensation fell 0.5% quarter-over-quarter in Q4, and was down 2.8% year-over-year. The previous increase in U.K. prices could remain a headwind for the U.K. consumer for the time being and, by extension, act as a restraint on the broader economy.

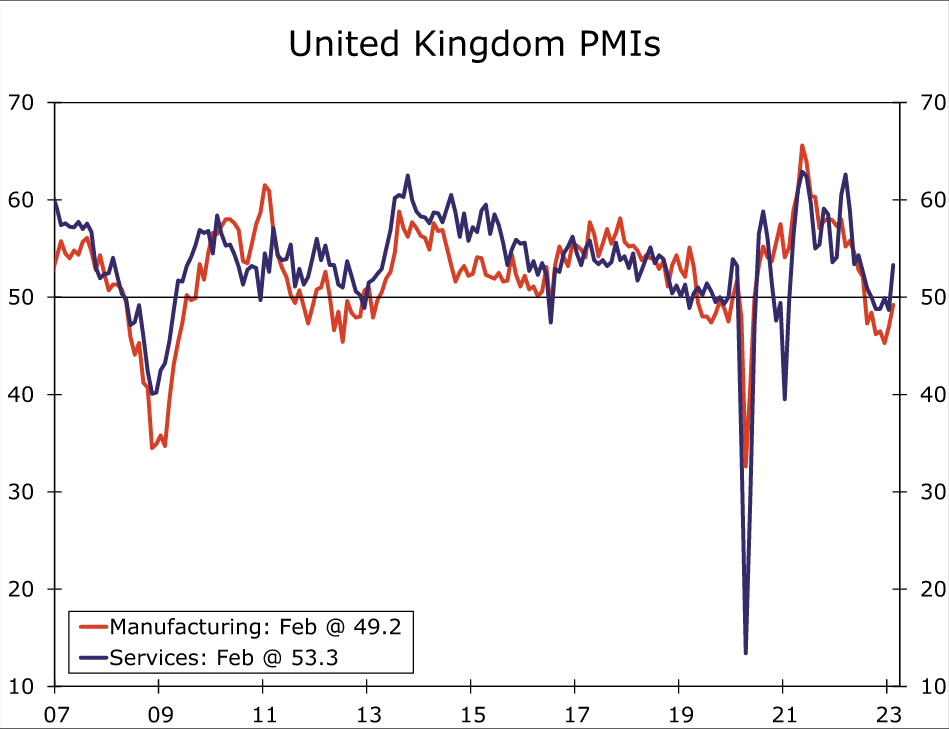

Most recently as energy prices have fallen back, there have been somewhat more encouraging developments for the U.K. outlook. Turning the page into 2023, retail sales rose in January, although that comes after a large December decline. Perhaps more noteworthy was the improvement in the U.K. February PMI surveys, as the manufacturing PMI rose to 49.2 and the services PMI rose above the breakeven 50 level to 53.3. The labor market backdrop is also reasonably solid, as Q4 employment rose by 74,000 and January payroll employees gained 102,000—both stronger than expected outcomes. Overall, this combination of U.K. data makes us less downbeat on the economy than previously. While we believe elevated inflation will remain something of a drag on the economy, we also believe that slowing inflation could result in less of a drag than we previously forecast. As a result, we have turned less negative on growth prospects in recent months. For full-year 2023 we now forecast U.K. GDP to contract by 0.6%, compared to a forecast 1.5% contraction as recently as December.

The Path Ahead for Bank of England Policy

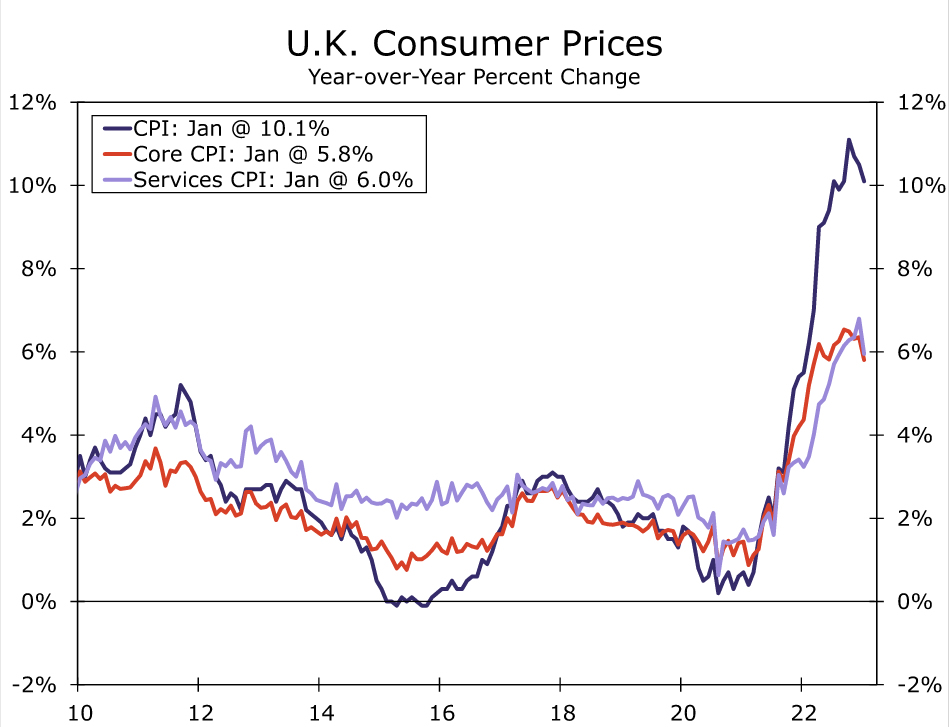

In addition to some better news on the activity front, there has also been improving news on the inflation front. Headline CPI inflation slowed more than expected to 10.1% year-over-year in January while, just as importantly, core CPI inflation also slowed more than forecast to 5.8% and services inflation slowed to 6.0%. It is true that those inflation readings remain elevated and well above the Bank of England’s (BoE) 2% inflation target, meaning some further policy tightening will almost certainly be forthcoming. The more pressing question is, given slowing inflation and underwhelming growth, what could the extent of that policy tightening be?

At its most recent policy announcement in early February, the BoE’s updated economic projections forecast CPI inflation falling below 2% over the medium term. Specifically, based on market implied interest rates at the time, which envisaged a peak policy rate near 4.50% around mid-2023, the central bank forecast CPI inflation to fall to 1.9% by Q1-2025 and to just 0.8% by Q4-2025. At the same time, in referring to the inflation outlook, Bank of England policymakers said there “are considerable uncertainties around this medium-term outlook, and the Committee continues to judge that the risks to inflation are skewed significantly to the upside.”

This was further elaborated in the minutes from the meeting, which qualitatively said that, “an inflation forecast that took into account these upside risks was judged to be much closer to the 2% target at the policy horizon than the modal central projection.” These considerations were reflected in the Bank of England’s policy guidance, in which the central bank said it will “continue to monitor closely indications of persistent inflationary pressures, including the tightness of labor market conditions and the behavior of wage growth and services inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

Recent comments from the BoE have been mixed, although comments from some key policymakers have leaned towards the dovish side. In mid-February, BoE Chief Economist Pill said continuing to raise interest rates at the pace of the past year would eventually, and perhaps soon, imply that monetary policy had tightened too much. In early February, BoE Governor Bailey said “I do think we’ve turned the corner in terms of headline inflation … It has not only fallen, it’s now under what we thought it would be in November. But we need to see more evidence that this process will take effect.”

Considering the Bank of England’s projections and policymaker comments, how quickly inflation decelerates, and to a lesser extent whether the economy shows renewed softness, will be key to how much further the BoE hikes rates. Should inflation continue slowing similarly to the pronounced pace seen in January, and should activity and survey data show renewed softening (which would be consistent with our forecast for U.K. Q1 GDP to fall by 0.2% quarter-over-quarter), we expect the Bank of England will be comfortable shifting to a slower pace of rate hikes and, indeed, we forecast a 25 basis point rate hike to 4.25% at the March monetary policy meeting. In fact, the longer inflation continues decelerating while U.K. growth remains subpar—which again is broadly consistent with our outlook—the more convinced policymakers could become that the upside risks to their below-target medium-term inflation forecast are dissipating. Thus, at the current juncture, should U.K. activity and inflation data soften as we anticipate, we expect the BoE’s March rate hike will mark the end of its tightening cycle and that rate cuts could begin by Q4 of this year.

While there is admittedly some upside risk to our policy rate outlook, our forecast peak of 4.25% is still well below market implied interest rates, which currently envisage a peak near 4.75% by September this year. The less aggressive approach we envisage from the BoE is also an important reason we expect that, over the medium-term, the pound will be an underperformer against a broadly soft U.S. dollar. Even as the greenback is weighed down by eventual U.S. recession and aggressive Fed rate cuts beginning from early 2024, we forecast only modest gains in the GBP/USD exchange rate, targeting around $1.2200 by the end of 2023 and $1.2400 by mid-2024. We also anticipate some decline in U.K. government bond yields from current levels over time, and forecast the U.K. two and ten year yields at 2.75% and 2.90% respectively by the end of this year.

{kind=link}