- As expected, the ECB hiked its three key policy rates by 50bp today and gave no indications for the coming rate path. The ECB communication clearly highlighted the number of risks prevailing to the economic and inflation outlook, but should the baseline prevail once the current turmoil subsides, more rate hikes may be needed. We keep our call for a 50bp rate hike in May due to the still high underlying inflation, and a peak policy rate reached in July of 4%.

- The ECB argued there is no trade-off between price and financial stability, which shows the ECB is willing to introduce measures to allow it to keep fighting inflation.

Inflation prevails – and remains too high for too long

Lagarde’s communication today showed a clear preference and focus on inflation over financial stability. For example, the first sentence in the ECB decision was ‘Inflation is projected to remain too high for too long’. She also said there is no trade-off between price stability and financial stability. While we believe that it is a very fine balance, the fact that she says this clearly shows to us the ECB is willing to take the necessary measures to allow it to further hike and fight inflation.

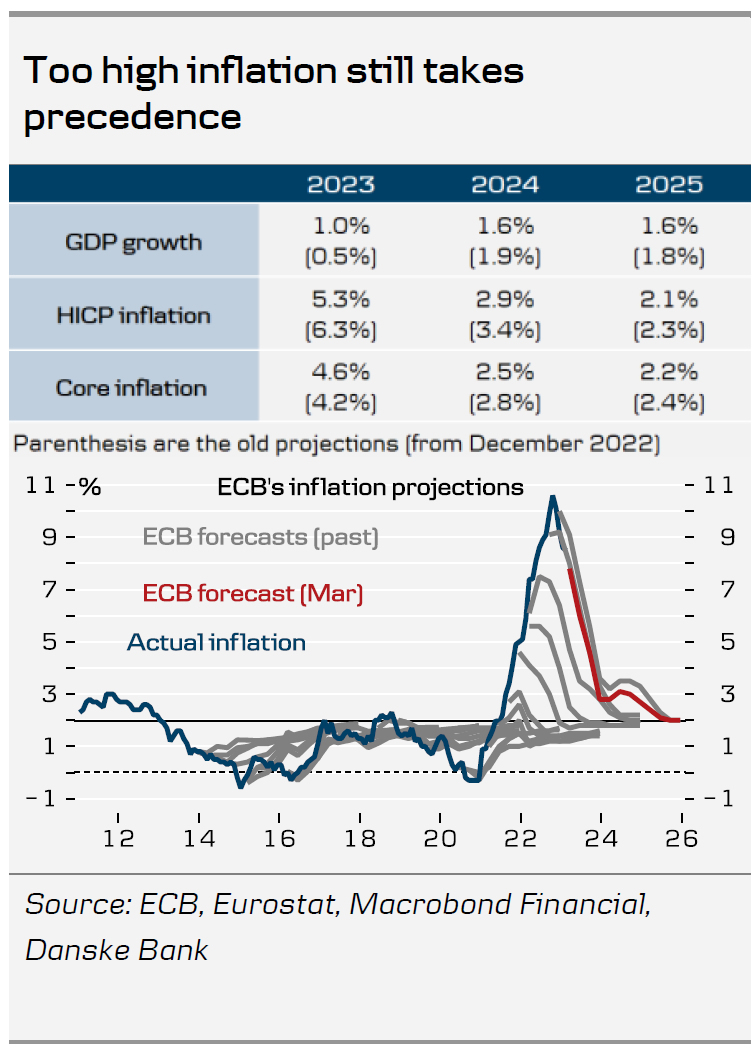

The new (though already outdated) staff projections showed both headline and core inflation remaining above the 2% target by the end of the forecast horizon in 2025. Growth and core inflation were revised higher in the near term, in light of the ongoing resilience of the economy. The ECB staff expects the euro area recovery to continue in the coming quarters, though risk to the growth outlook remains tilted to the downside, particularly from adverse confidence effects in financial markets impacting credit conditions.

With a strong labour market and still building wage pressures, Lagarde stressed that the ECB cannot afford to waver in its commitment to fight inflation. We agree, as underlying price pressures remain too strong and pipeline pressures mean high core inflation could remain a worry for the ECB for some time yet.

No guidance for May

The ECB statement did not give any explicit guidance for the size of the May policy decision. However, Lagarde said they will remain data dependent, and should the baseline persist, then ‘we have a lot more ground to cover’, thereby also saying that more hikes are coming – and potentially this could be another 50bp in March. As we are yet to see if this turns into a macroeconomic crisis or if the turmoil stays isolated, we continue to like our call for a 50bp rate hike in May and a peak policy rate reached in July at 4%. Ahead of the decision today, no option other than the 50bp rate hike was discussed and the decision was taken by a very large majority. She said that three or four GC members didn’t support the decision, as they would have liked to see more data before taking that decision.

Future rate path

The ECB’s decision statement laid out what will form the future rate path: 1) its assessment of the inflation outlook in light of the incoming economic and financial data; 2) the dynamics of underlying inflation; and 3) the strength of monetary policy transmission. Specifically, Lagarde said she is already seeing a ‘good transmission’ of rate hikes in the credit sector, although it may take longer to feed through. Notably, the weakened and delayed pass through has been discussed by both Chief Economist Lane and ECB board member Schnabel recently.

Financial stability and uncertain outlook – but no measures

While financial stability features prominently, focus was on the alertness and preparedness, should it be needed. Both de Guindos and Lagarde emphasised that compared with previous crises, euro area banks are in completely different and vastly improved capital positions.

50/50 for a rate hike in May – limited market reaction

Markets are little changed after the press conference today and are now pricing in a 50/50 probability of the ECB hiking in May at all. However, as we see it, the question boils down to whether or not this turmoil in the banking sector turns into a macroeconomic crisis; the market pricing represents this very binary outcome space. If yes, this is deflationary in itself – and therefore sizeable rate cuts could follow, which could lead to a significant steepening of the curves; however, if no, (our baseline), markets appear ripe for a repricing higher in yield as inflation is still stubbornly high for the central bank to accept. This suggests more curve inversion. That means we should see a significant repricing once the dust settles. After the FOMC next week, we believe markets will focus again on the macro picture, which is too high inflation.

Despite the large uncertainty with respect to the rate decision, the reaction in FX markets was remarkably limited. We entered the meeting with a fundamental predisposition of wanting to sell EUR/USD rallies on a 50bp hike but the cross hardly reacted with the FRA curve flattening upon announcement. Looking ahead, systemic risk fears look set to dominate price action among majors. Our bias remains for systemic fears to subside over the coming weeks, but we humbly acknowledge the high sensitivity to negative news, which leaves us side-lined with no high-conviction calls near term. On a 3-6M horizon, we still pencil in a lower EUR/USD compared with current spot levels.

{kind=link}