Summary

- The Bank of England and Swiss National Bank both make monetary policy announcements tomorrow, March 23.

- Our base case is for the Bank of England to raise its policy rate 25 basis points to 4.25% this week, and then pause tightening. However, an unexpected quickening of inflation has added some uncertainty to that outlook. In the absence of a closer, or finely balanced, vote in favor of a rate hike, or a softening in the Bank of England’s language, we will be inclined to adjust our outlook towards further tightening, an adjustment that could also be positive for the pound.

- In Switzerland, growth appears to be bottoming out and there has been an uptick in inflation. While Swiss markets have been dominated by banking sector strains over the past week, with some sense of relative calm restored and after the European Central Bank’s rate hike last week, we still expect the Swiss National Bank to raise its policy rate by 50 basis points to 1.50% at this week’s announcement.

Bank of England to Hike, But Will They Signal More To Come?

The Bank of England (BoE) announces its monetary policy decision on March 23, with market participants focused on both the size of any potential rate hike and any signals of potential future rate hikes. Our base case has been for the Bank of England to hike its policy rate by 25 basis points to 4.25% at this week, a view with which we are still comfortable. In recent days, as banking sector strains in the U.S. and Switzerland led to unsettled global markets, market discussion has centered on whether the Bank of England could even pause at this week’s meeting. However, with those strains alleviated to a modest extent, further tightening now seems very likely at this week’s meeting.

A more interesting question, in our view, is whether there will be any further tightening beyond this week’s meeting. Our base case has been that this week’s rate increase will be the last of the current cycle. The Bank of England’s economic projections, which forecast a moderate U.K. recession and below-target inflation over the medium-term, are consistent with a pause from the Bank of England after this week. In our view, some key policymakers have also been quite balanced in their comments and are looking for opportunities to pivot towards a pause. For example, Governor Bailey recently said in early March, “I would caution against suggesting either that we are done with increasing Bank Rate, or that we will inevitably need to do more”.

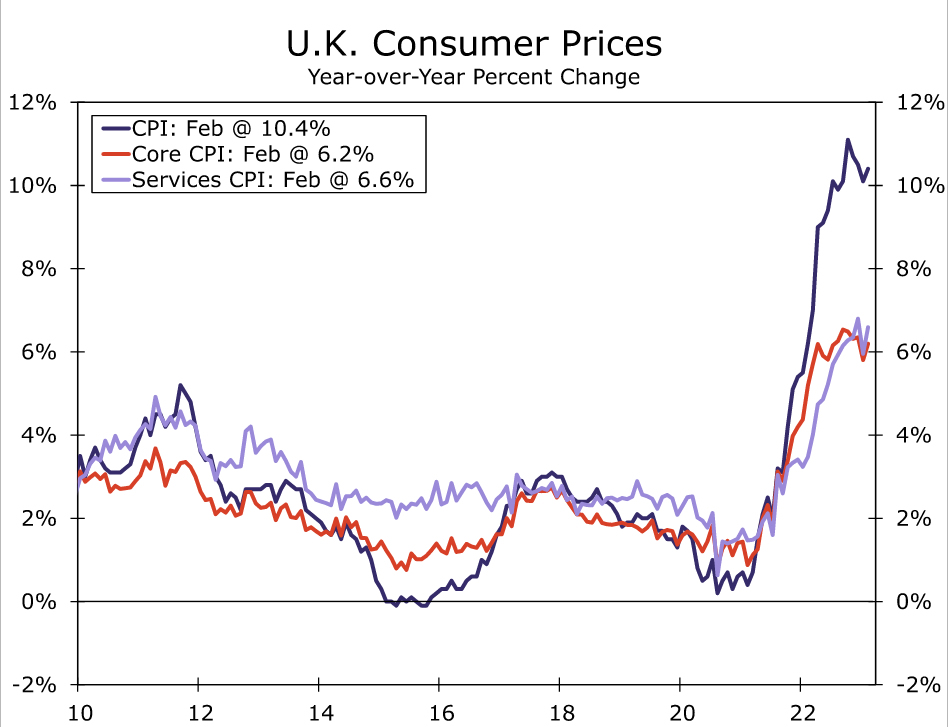

A moderate slowing in inflation over the last few months had opened the door slightly ajar, in our view, to a Bank of England pause. However, that pause has been thrown into doubt by the U.K. February CPI. U.K. inflation was an upside surprise, with the headline and core CPI unexpectedly quickening to 10.4% and 6.2% year-over-year, respectively. Today’s Federal Reserve monetary policy decision may also be a factor—while it is not our base case, if the Fed does hike rates at its meeting, it could potentially make it easier for the Bank of England to deliver additional rate hikes after this week as well. Hence, while we are reasonably confident the BoE will hike rates 25 basis points this week, we will be scrutinizing the accompanying statement closely for signs of a pause (or not) going forward. In particular:

- The Bank of England voted 7-2 at its February meeting to hike rates, with the two dissents in favor of holding rates steady. We look for a closer vote split (6-3 or 5-4) as a hint that this week’s hike could be the last. However, if the vote remains decisively in favor of a rate increase, more hikes could be forthcoming.

- The BoE also said it “will continue to monitor closely indications of persistent inflationary pressures, including the tightness of labor market conditions and the behavior of wage growth and services inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.” (Note: Our bolding). Should the BoE once again highlight these persistent inflationary risks, that would be a signal of further tightening in our view.

To sum up, we will be looking for a closer vote split and a softening in the Bank of England’s language to support the view of a potential pause. In the absence of those elements, we will be inclined to adjust our outlook towards further Bank of England tightening, and adjustment that could also be positive for the pound.

Swiss National Bank to Hike Despite Banking Sector Strains

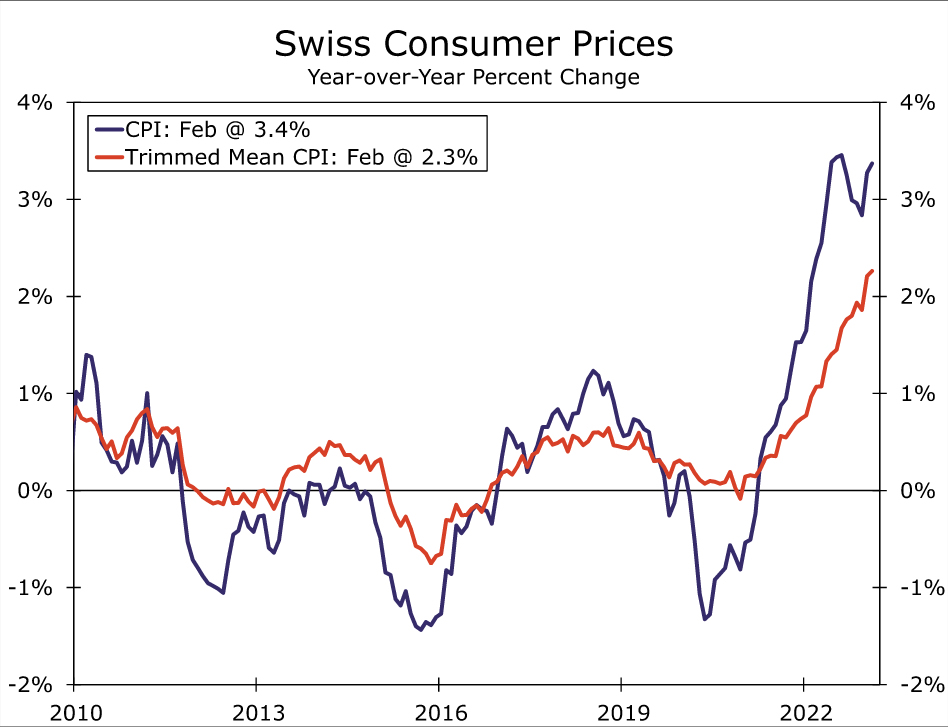

Early last week, we wrote on the Swiss economy, highlighting that growth appears to be bottoming out while CPI inflation has shown a renewed uptick, as the trimmed mean CPI rose 2.3% year-over-year in February. This led us to anticipate a 50 basis point hike from the Swiss National Bank (SNB) at its March 23 announcement. Since then, Swiss markets have been dominated by banking sector strains, which ultimately saw authorities engineer a takeover of Credit Suisse by rival firm UBS. The deal led the SNB to provide 100 billion francs of liquidity support for UBS, and the Swiss government to provide a guarantee of 9 billion francs against potential losses. With those developments having restored some relative calm to markets (the emphasis here is very much on the relative rather than the calm), and with the European Central Bank having raised its policy rate 50 basis points last week, we still expect the SNB to raise its policy rate by 50 basis points to 1.50% at this week’s meeting. Moreover, while Swiss growth could be softer than previously expected, CPI inflation will likely remain mildly elevated above the central bank’s 2% inflation target for the time being. If the SNB does raise rates 50 basis points this week, even in the context of recent market events, we believe it will also deliver a 25 basis point rate hike at its June meeting amid what we expect will be calmer markets conditions.

{kind=link}