Summary

- The FOMC raised its target range for the federal funds rate by 25 bps at today’s policy meeting. Fed policymakers have raised rates by 475 bps over the course of the past 12 months, the fastest pace of tightening since the early 1980s.

- The FOMC continues to have a relatively upbeat assessment of the current state of the economy. That said, it noted that “recent developments are likely to result in tighter credit conditions.” This credit tightening likely will “weigh on economic activity,” although “the extent of these effects is uncertain.”

- Previously, the FOMC thought that “ongoing increases” in the fed funds rate would be needed to bring inflation back to the Committee’s 2% target. Now the FOMC thinks that “some additional policy firming may be appropriate.” In short, it appears that the end of the current tightening cycle is coming into view.

- The median 2023 dot in the “dot plot” lies between 5.00% and 5.25%, which is only 25 bps higher than the current target range for the federal funds rate. We look for the FOMC to hike rates by 25 bps at its May 3 before going on an extended pause in future meetings in 2023.

FOMC Hikes Rates By 25 bps Again

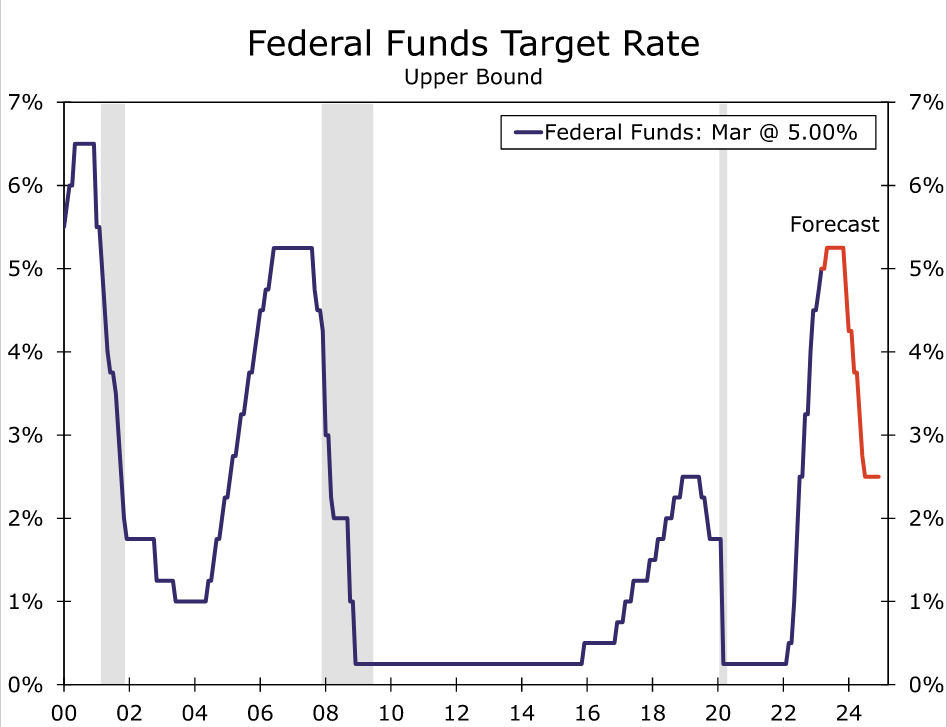

The Federal Open Market Committee (FOMC) voted unanimously today to hike rates by 25 bps, bringing the target range for the federal funds rate to 4.75%-5.00% (Figure 1). The Committee has now hiked rates by 475 bps over the course of the past 12 months, the fastest pace of tightening since the early 1980s. Furthermore, the FOMC decided to maintain the current pace of quantitative tightening, allowing up to $60 billion of Treasury securities and $35 billion of mortgage-backed securities to continue to roll off its balance sheet every month. The decision was more or less expected by financial markets.

The FOMC continues to characterize the current state of the economy in favorable terms. The statement noted that “recent indicators point to modest growth in spending and production,” and that job gains “are running at a robust pace.” According to the FOMC, “inflation remains elevated.” The Committee also noted the strains that have appeared in the banking system recently. In the FOMC’s view, these strains “are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring and inflation,” although “the extent of these effects is uncertain.”

Accordingly, the FOMC backed off somewhat on its forward guidance regarding further tightening. Previously, the statement said that “ongoing increases (emphasis ours) in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” The FOMC now judges that “some additional policy firming may be appropriate.” In short, the uncertainty that the present banking system turmoil has engendered, along with the “tighter credit conditions” that likely will result, means that the end of the current tightening cycle is coming into view. In that regard, Chair Powell acknowledged in his post-meeting press conference that the FOMC considered a pause in its tightening cycle at this meeting.

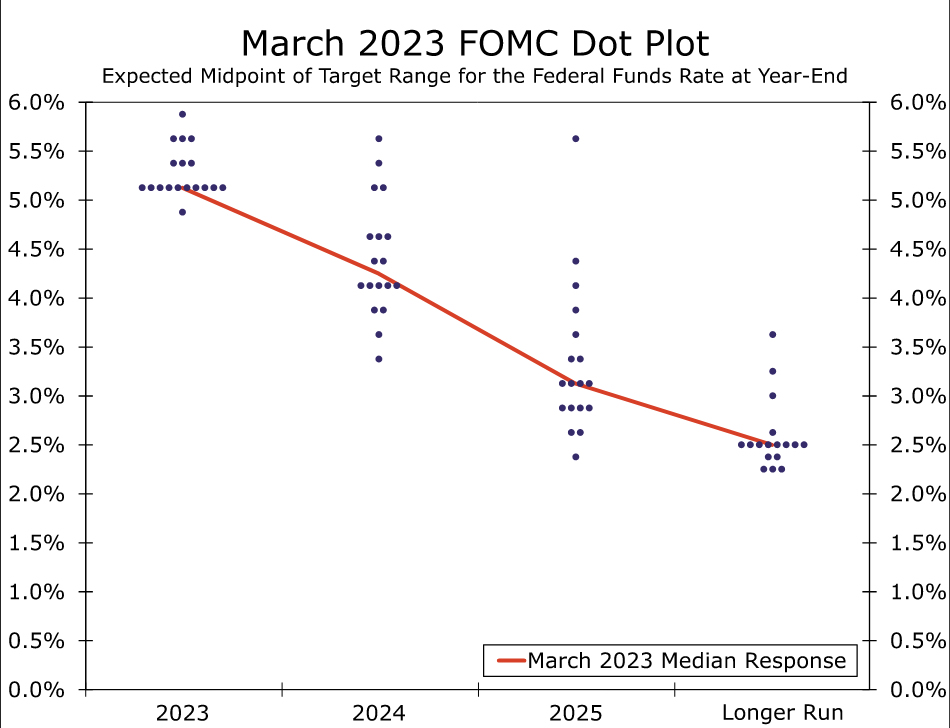

The FOMC updated its Summary of Economic Projections (SEP), as it normally does once per quarter, in which it specifies its macroeconomic forecasts. The SEP contains the so-called “dot plot” that shows each individual FOMC member’s assessment on the appropriate level of the fed funds rate over the next few years (Figure 2). The median dot for the end of this year lies in the middle of the 5.00%-5.25% range. Although this median dot is unchanged from the last dot plot in December, it likely would have been higher if banking system strains had never occurred. Relative to the projection that it released in December, the FOMC shaved 0.4 percentage points from its GDP growth forecast for 2024 and now looks for 1.2% GDP growth next year. This downward revision is consistent with the Committee’s view that the current strains in the banking system will lead to “tighter credit conditions” that likely will have consequences for the real economy.

As we wrote in our recent U.S. Economic Outlook in which we updated our forecasts, we are explicitly assuming that authorities take the necessary steps in coming days and weeks to keep the current turmoil in the banking system more or less contained. If this assumption proves to be valid, then we anticipate that the Committee will increase the target range for the federal funds rate by another 25 bps at its next meeting on May 3, which we believe will be the last rate hike in this cycle. We think the FOMC will refrain from hiking the fed funds rate at the June 14 meeting in order to assess the effects that tighter monetary policy and credit conditions are having on the economy. That said, we would judge the risks to our fed funds forecast to be skewed to the upside. That is, we judge the probability of another 25 bps rate hike at the June 14 meeting to be higher than a pause at the May 3 meeting, assuming that authorities are successful in stabilizing the recent turmoil. We expect the Committee will remain on hold for most of the rest of 2023 as economic activity weakens and inflation recedes further. If our forecast of a modest recession beginning in the third quarter comes to pass, then we look for the FOMC to cut rates significantly next year.

{kind=link}