The Federal Reserve delivered its tenth consecutive rate hike on Wednesday, as expected, but reset its guidance to indicate increased emphasis on incoming data. Hence, Friday’s nonfarm payrolls will be the next test for the US dollar at 12:30 GMT, with forecasts pointing to a discouraging outcome.

A dovish rate hike

The Federal Open Market Committee (FOMC) decided to increase its funds rate by a quarter percentage point to the highest range in sixteen years of 5.0-5.25% for the sake of fighting inflation, despite three private banks collapsing recently. Although Powell reiterated that the banking system remains sound and resilient, he acknowledged that downside risks in the sector have grown, and a more cautious approach might be needed.

Unlike the ECB, the Fed is now more confident that a pause in monetary tightening could be around the corner but with inflation standing at 5.0% y/y – more than twice its symmetrical 2.0% target – it could not make any promises. Alternatively, it chose a safer path, adopting a less hawkish guidance to state that additional tightening could still be possible if there are signs of stronger-than-expected growth, inflation, and hiring. Previously, policymakers were focused on signs of slowing inflation to ease the pace of tightening.

Nonfarm payrolls might be the next challenge for markets

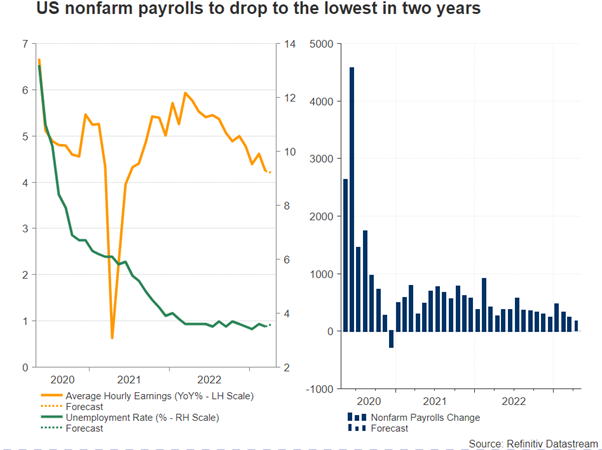

Consequently, the central bank’s new guidance added extra importance to the upcoming nonfarm payrolls report due on Friday. Investors expect employment growth to have eased to a more-than-a-year low of 180k in the month of April, while projecting a negligible pickup in the unemployment rate to 3.6% and a steady wage growth of 4.2% y/y.

If forecasts are correct, the data would still reflect a tight labor market, though given the persisting rate cut pricing in futures markets, a significant decline in jobs growth could send fresh negative shockwaves to the US dollar, especially if the participation rate pulls lower as well. Powell tried to convince investors that rate cuts are not on the table at the moment, but his efforts proved fruitless, with investors currently providing a small probability of 13.5% for a 25bps rate cut in June while projecting an equivalent rate cut at some point in the fourth quarter.

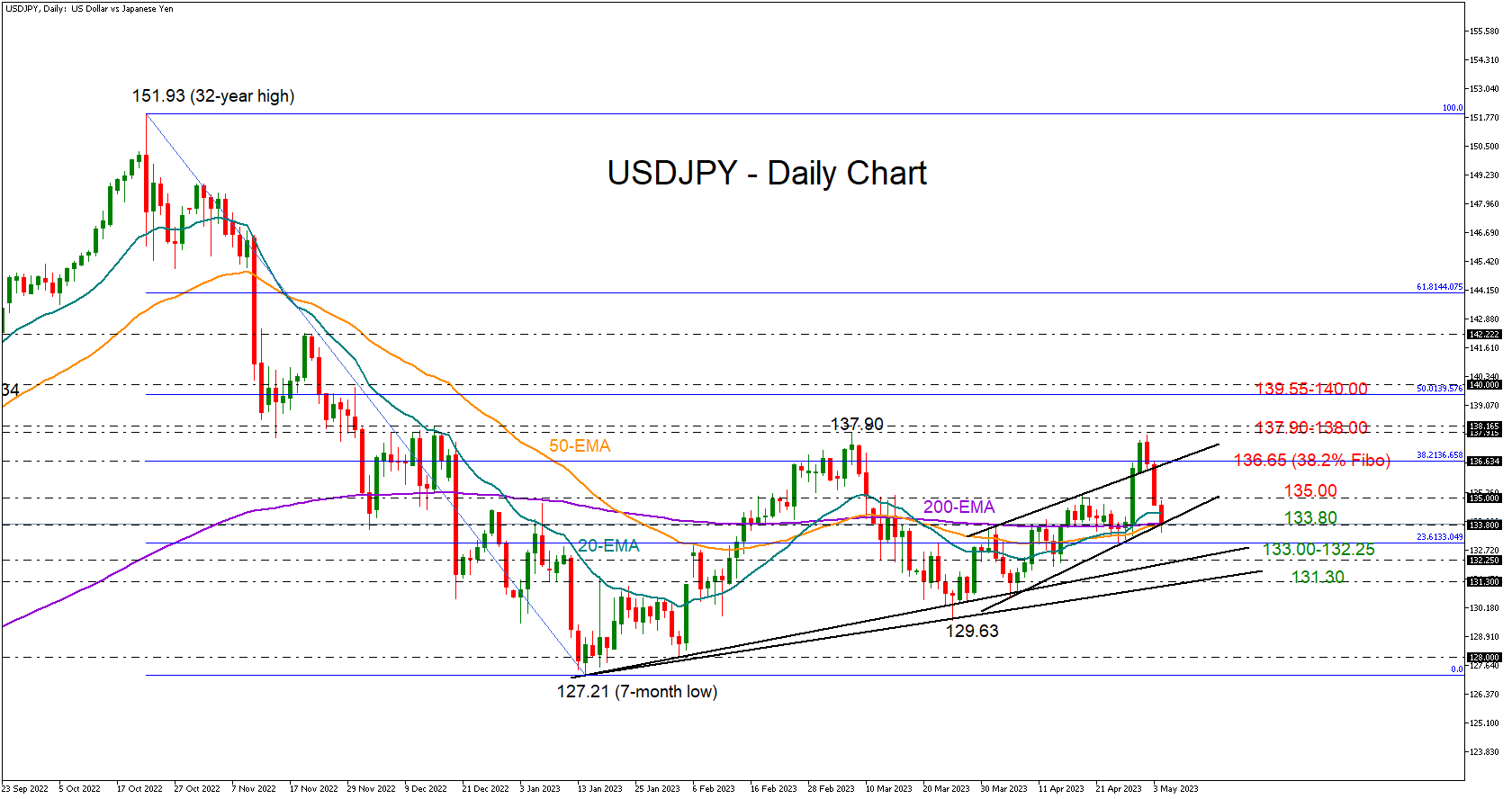

USD/JPY levels to watch

The group of dovish traders could grow further if the employment report misses forecasts, likely staging a new bearish wave in dollar/yen. The pair is testing the key 134.00-133.80 support region at the moment, a break of which could extend losses towards the former 133.00-132.25 support region and then down to 131.30.

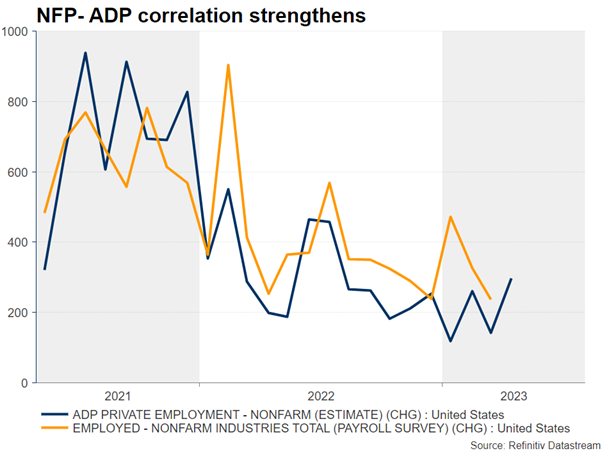

On the other hand, the improvement in the ISM employment indices and the remarkable spike in the private ADP employment report, which came in twice as high as analysts forecast, is feeding speculation that the outcome might arrive brighter than expected. It’s worthy to note that although the private ADP data has been a misleading proxy for the government’s comprehensive NFP report for some time now, the correlation between the two surveys has been improving over the past few months.

Technically, the data will need to be strong enough to help dollar/yen crawl back above 135.00. In this case, the pair may extend its recovery towards the 136.65 constraining. Yet, only a sustainable extension above 137.90-138.00 would switch the short- and medium-term outlook back to bullish.

{kind=link}