- In line with our expectation, the BoE today hiked policy rates by 25bp, bringing the Bank Rate to 4.50%.

- With both growth and domestic inflation having surprised to the topside and given BoE’s message today we pencil in an additional 25bp hike in June 2023.

- We now expect the Bank Rate to peak at 4.75%. We still do not envision rate cuts from BoE before 2024.

In line with our expectation, the Bank of England (BoE) hiked the Bank Rate (key policy rate) by 25bp to 4.50% with 7 members voting for a 25bp hike and two members voting for keeping the Bank Rate unchanged.

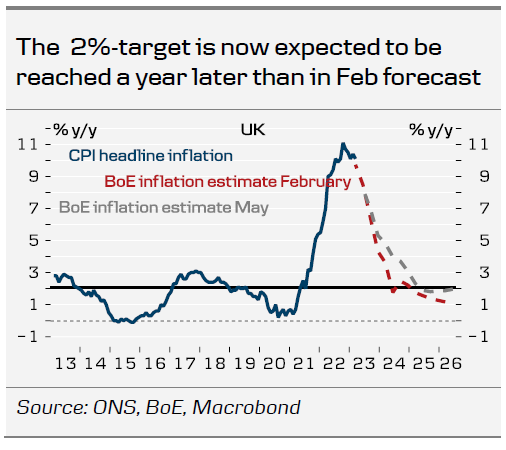

Given the past months strong data releases we have for some time contemplated revising our call to include another hike in our profile. With the communication from the BoE today, we think this marks the final nail in the coffin. The BoE continues to keep the door open for further increases in the Bank Rate repeating that “if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.” The majority of the Monetary Policy Committee (MPC) voted for an increase of 25bp as they deemed it “important to continue to address the risk of more persistent strength in domestic price and wage setting”. The updated inflation projections showed that the BoE has revised its inflation projections higher across the forecast period, now expecting inflation to reach its 2% target in 2025. Additionally, the MPC sees the “risks around the inflation forecast [as] skewed significantly to the upside”. The key concern for the BoE remains developments in wage data as well as service inflation and thus is the key data to follow.

With both the global backdrop, inflation and wage growth having surprised to the topside, we do not believe that data will have weakened enough for the BoE to pause its hiking cycle at the June meeting. We thus revise our forecast to include a 25bp hike in June, marking a peak in the Bank Rate at 4.75%. Likewise, we believe that upcoming data releases have to prove worse than expected for a pause to be warranted considering the forecasts presented in the Monetary Policy Report (MPR).

Rates. Initially, Gilts yields moved 5bp higher across the curve. However, during the press conference, yields began to trend downwards, reaching their lowest level in a week. Probably rather influenced by developments in European and US yields, rather than any new information at the press conference. The peak rate of 4.8% remained unchanged.

FX. EUR/GBP initially moved slightly lower but fully retraced the move during the press conference. Overall, we regard the relative central bank outlook to be a positive for EUR/GBP but with other factors acting as a headwind, we increasingly see a case for continued range trading in the cross around 0.87-0.88.

Our call. We now expect another hike of 25bp at the June meeting. In order for BoE to keep policy rates unchanged we believe that we would have to see data releases prove considerably worse than what we currently pencil in. Our call is fairly closely in line with market pricing (33bp until September). Markets are pricing in a likelihood for a cut in December (-6bp). We still believe that the first rate cuts will not be delivered before Q2 2024.

hiked the Bank Rate (key policy rate) by 25bp to 4.50% with 7 members voting for a 25bp hike and two members voting for keeping the Bank Rate unchanged.){kind=link}