- US debt ceiling limit of US$31.4 trillion may be reached on 1 June.

- Prior movement of implied bond market volatility during the 2011 US debt ceiling standoff provided a leading indicator for the uptick in US stock market volatility.

- Given the current loop-sided performance among the major US benchmark stock indices, the downside adjustment to offset the relatively low level of the VIX may be significant.

The US debt ceiling limit is now getting closer to hitting the US$31.4 trillion cap that was approved previously in December 2021. Failure to extend the current ceiling and the shortfall in tax revenue collections to cover fiscal policies spending at this juncture will render the US government inability to issue new bonds to pay for its existing obligations.

US government at risk of technical default after 1 June

US Treasury Secretary Yellen warned earlier that based on current projections, the X-date, when the US government could lose the ability to meet all its payment obligations, could arrive as early as 1 June. Since the middle of January, the US Treasury has started to withhold scheduled contributions to a federal employee retirement fund and keep paying debts to delay the ceiling limit from being breached.

Based on the latest update from the US Treasury last Friday, 12 May, it had just US$88 billion worth of extraordinary measures left to enable it to pay the existing bills as of 10 May and this amount is justly slightly above a quarter of the US$333 billion of authorized measures that are still available to keep the US government from running out of borrowing room under the current debt ceiling limit of US$31.4 trillion.

Hence, time is running out for Congress to approve an extension of the debt ceiling before 1 June, and failure to do so increases the risk of a first-ever technical default in the US government’s obligations which has the potential to roil financial markets via a tightening in credit conditions via a similar downgrade of the long-term outlook and even credit rating of US sovereign bonds by credit rating agencies that occurred in the summer of 2011.

What happened to the markets during the 2011 debt ceiling standoff?

The 2011 US debt ceiling partisan squabbles started around 9 April 2011 between then Obama’s Democrats White House Administration and the Republicans’ controlled House.

Due to extraordinary measures and various accounting methods, the 2011 US debt ceiling extension deadline was prolonged to 2 August 2011. During this period, there were lots of drama, intense negotiations, and “horse trading” among key leaders of the Democrats and Republicans on tax cuts and fiscal spending to reduce the budget deficit.

A point to note is that during this period, the global financial markets had another risk factor to consider which was the European sovereign debt crisis inflicted on Greece, Portugal, and Spain.

Fig 1: S&P 500, US Dollar Index, US Treasury Bonds, VIX & MOVE during 2011 US debt ceiling standoff.

(Source: TradingView, click to enlarge chart)

Before the US debt ceiling limit extension was finally approved by US Congress on 2 August 2011, the S&P 500 had tumbled by -15% from its May 2011 high to its August 2011 low and even fall further to record an accumulated loss of -20% before it hit a major swing low in early October 2011.

The US Dollar Index was almost unchanged during this period whereas else there was a flight to safety despite the credit ratings and outlook downgrade from Standard & Poor’s on the US sovereign debt from AAA to AA+ that saw the US Treasury 20+ year bonds ETF (TLT) to record return of +14% over the same period.

What’s interesting was the Chicago Board Options Exchange (CBOE) Volatility Index, the VIX, a measurement of the 30-day forward-looking volatility of the S&P 500 remained “calm” at around a level of 15 that indicating complacency before the S&P 500 recorded its most severe sell-off during May 2011 to Oct 2011.

In contrast, the ICE BofAML MOVE Index tracks the implied volatility (over-the-counter options) of the US Treasury yield on 2-year, 5-year, 10-year, and 30-year US Treasuries have ticked up before the S&P 500 plummeted. Hence, the bond market started to price the heightened risk of a credit condition crunch or squeeze that could be detrimental to equities via a higher cost of funding ahead of the VIX Index.

What are the volatility crystal balls of the MOVE and VIX saying now?

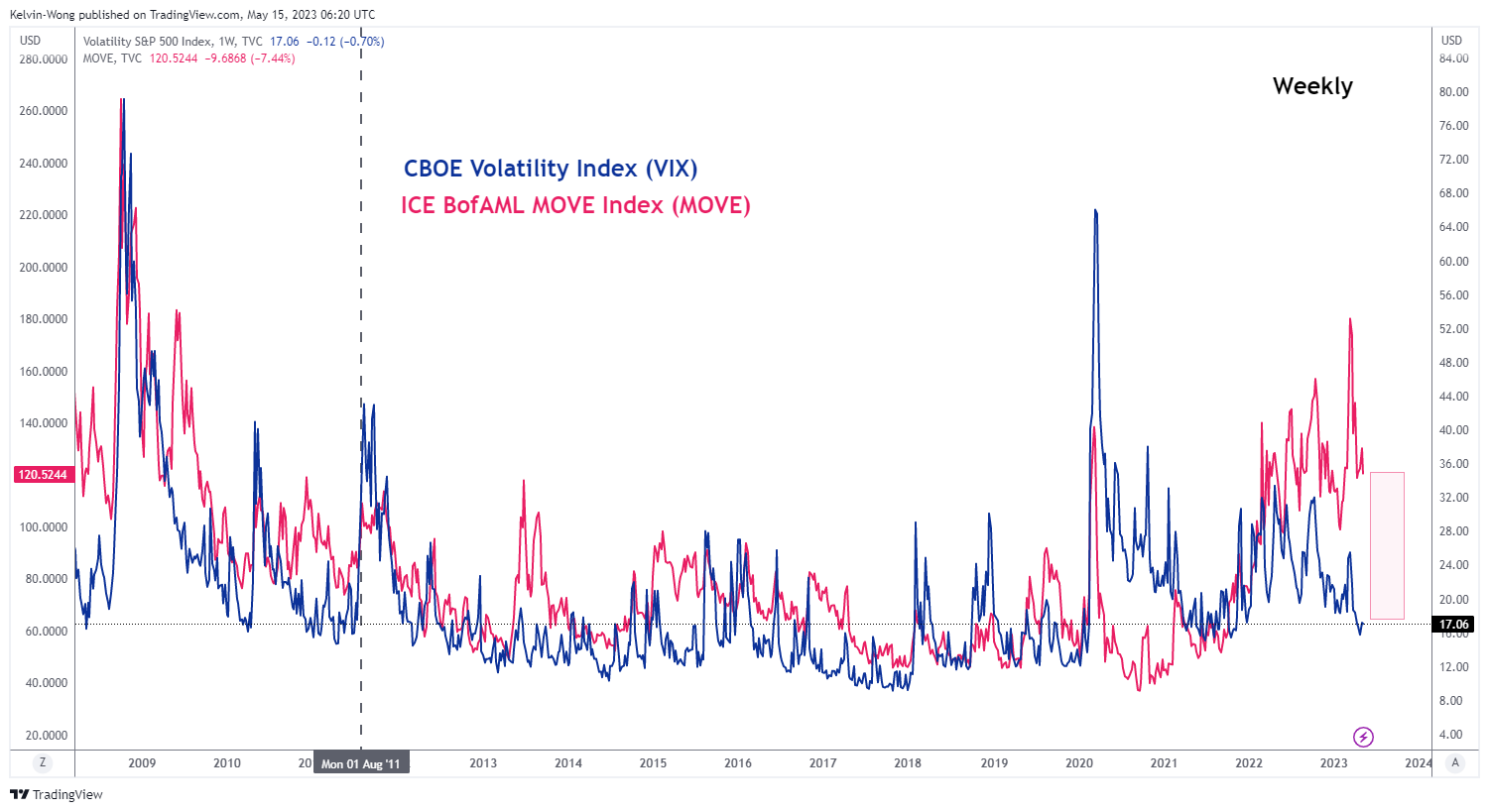

Fig 2: VIX & MOVE trend as of 12 May 2023 (Source: TradingView, click to enlarge chart)

Based on last Friday, 12 May data, the VIX has continued to plummet to 17.06 which is close to a 2-year low but in contrast, the MOVE Index has remained at an elevated level of 120.50 and this is still higher than the 90.00 level reached during the onset of the summer 2011 US debt ceiling extension negotiations.

Hence, the MOVE Index has now started to price in the risk of a risk-off scenario via a spike in the US Treasury yields which in turn may provide a leading signal for the VIX to stage a rebound at such low levels of “complacency”.

Thus, given the current loop-sided performance of the major US stock indices where the technology and long-duration concentrated Nasdaq 100 outperformed the rest of the pack with a current year-to-date return of (+21.9%) over the S&P 500 (+7.4%), Dow Jones Industrial Average (0.5%) and the Russell 2000 (-1.2%), the downside risk of the Nasdaq 100 and S&P 500 is indeed still a “live” event that may occur in the coming weeks as the clock ticks closer to 1 June coupled with an external risk of on-going geopolitical tensions and sticky inflationary environment.

{kind=link}