- Monetary policies and guidance of the 4 major central banks are moving in the opposite direction.

- US Fed and Eurozone ECB are in the hawkish camp while Japan BoJ and China PBoC are still in accommodating mode.

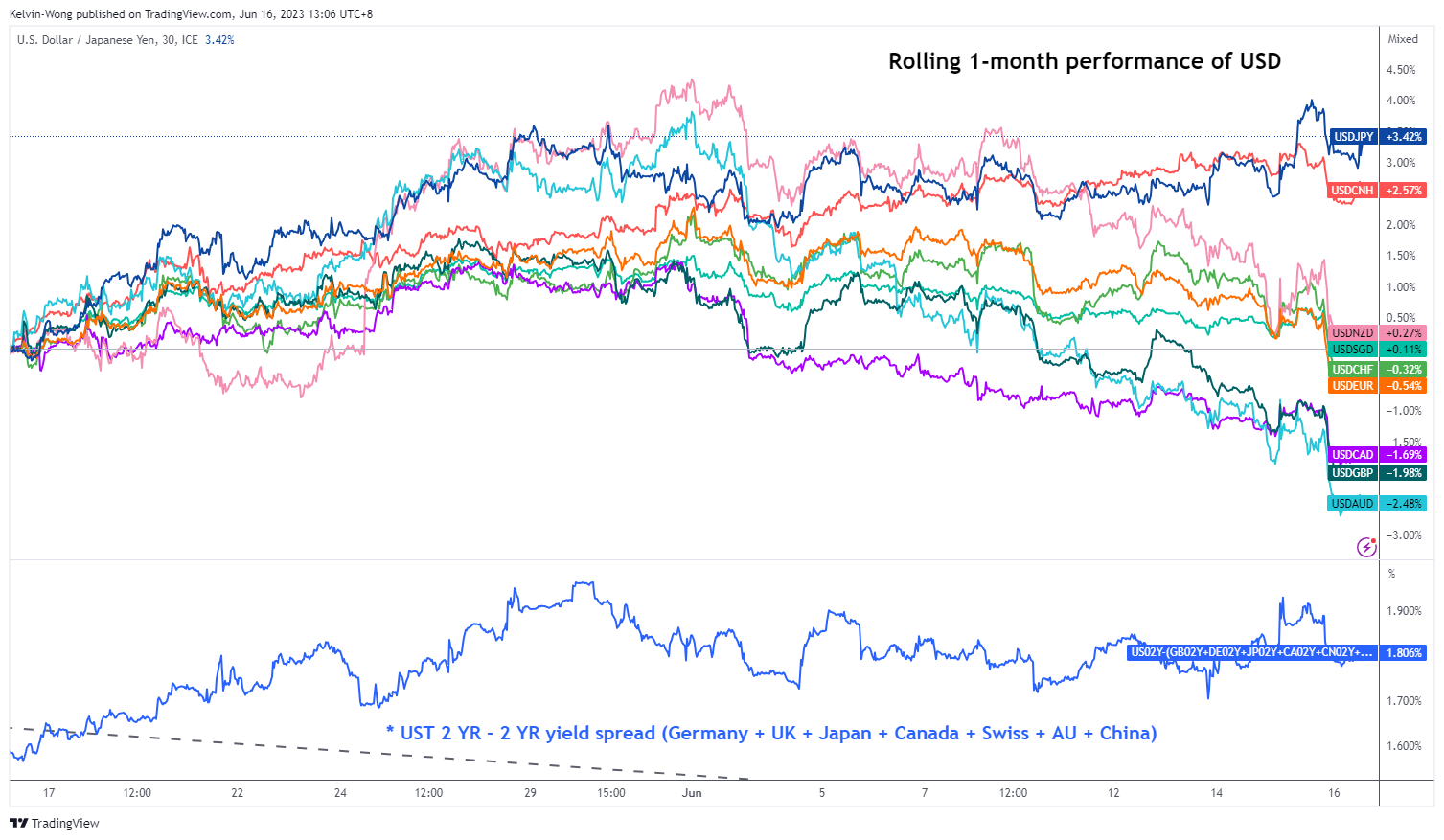

- K-shaped performance in USD against key G-20 currencies; JPY remained weak and CNH sideways, in contrast, the rest has strengthened against the USD.

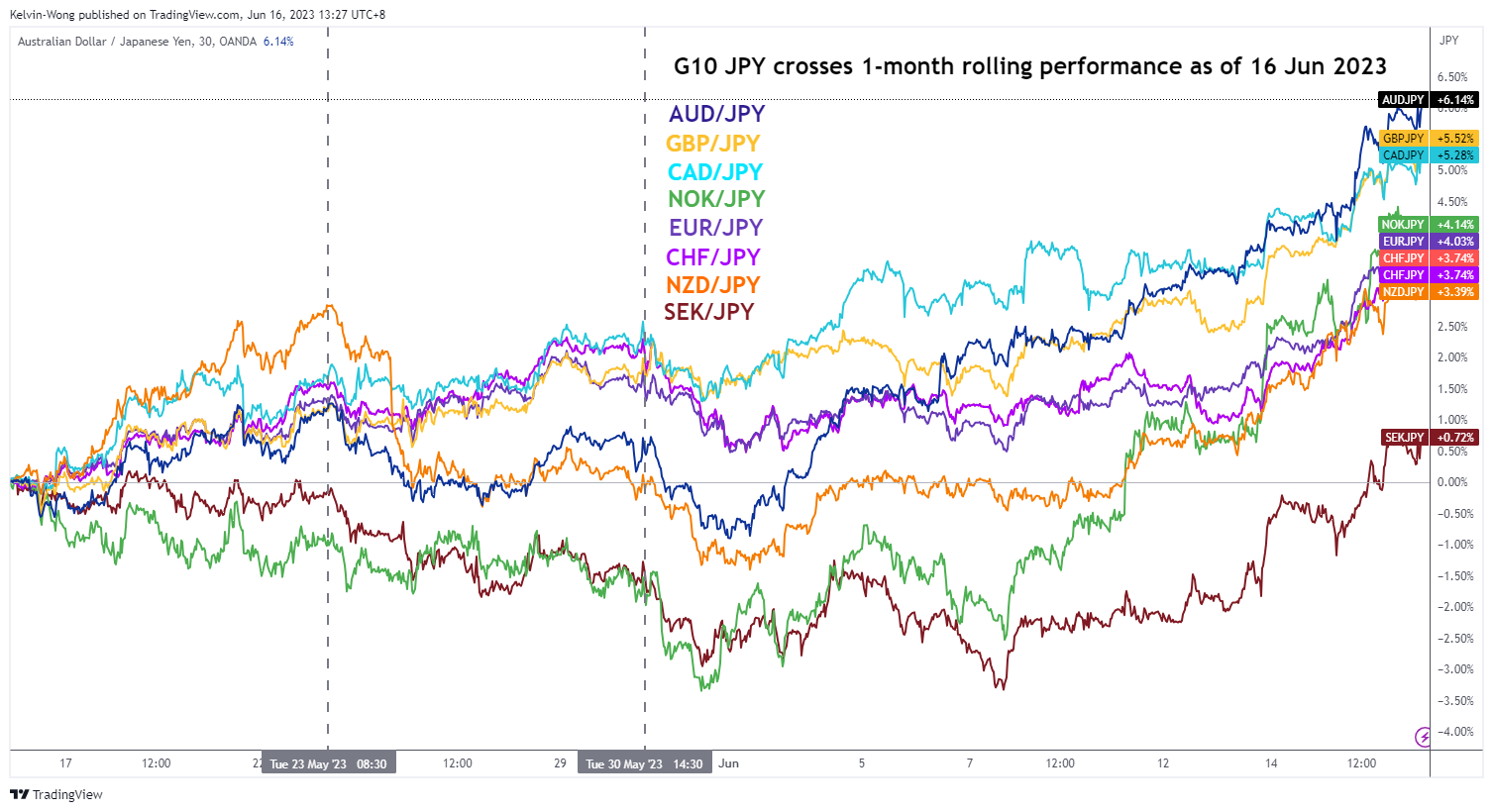

- G-10 JPY crosses are bursting up.

We have concluded three plus one monetary policy decisions outcome from four major G-20 central banks for this week; the US Federal Reserve (Fed), European Central Bank (ECB), Bank of Japan (BoJ), and People’s Bank of China (PBoC).

The latest monetary policies guidance from the Fed and ECB has been more skewed toward the hawkish side; despite the FOMC’s decision to skip a hike on the Fed funds rate this time round, the dot-plot projection has suggested two 25 basis points hike before 2023 ends to bring the terminal Fed funds rate of this current hiking cycle to a median level of 5.6%.

Over at the ECB, President Lagarde has hinted during the press conference that ECB is likely to hike by another 25 basis points (bps) in July after it raised its key policy deposit rate by 25 bps yesterday, 15 June to bring it to 3.5%, the highest level in more than 20 years. Expectations from money markets indicate that ECB may not be done hiking after July as traders’ positioning has implied an 80% probability of the ECB raising the deposit rate to 4% by October, an increase from 50% odds earlier.

In Asia, PBoC cut its one-year medium-term lending facility (MLF) interest rate yesterday which lends out funds to major China commercial banks by 10 bps to 2.65%, its first cut since August 2022. Hence, the expectations have now increased for more easing policies from PBoC to address the current slew of weak domestic/internal consumption data from China, a shift from its prior cautious targeted accommodating monetary policy stance.

Today, BoJ has maintained its ultra-easy monetary policy in place since the Great Financial Crisis of 2009, with no change in the band for the yield curve control program of the 10-year Japanese Government Bond at 0.50% on either side and short-term key policy interest rate stayed at -0.1%.

BoJ’s monetary policy statement cited Japan’s economy is picking up and likely to continue recovering moderately. But stated that the pace of core inflation is likely to slow down towards the middle of the current fiscal year with inflationary expectations moving sideways after an earlier increase. Therefore, this latest statement has suggested that BoJ is not in a “rush mode” to normalize its ultra-easy monetary policy due to an expected slowdown in inflationary pressures.

Impact on the FX market, USD outperformance against JPY but weaken significantly against the rest

Fig 1: USD against key G-20 currencies (including NZD) rolling 1-month performances as of 16 Jun 2023

(Source: TradingView, click to enlarge chart)

The rolling 1-month performances of the USD against the key G-20 currencies (inclusive of NZD) as of 16 June 2023 has shown a stark contrast driven by the current easy momentary policies mode of BoJ and PBoC. A “K-shaped” performance where the USD has strengthened against the JPY, sideways with CNH (offshore yuan) but weakened significantly against CAD, GBP, and AUD at this time of the writing.

JPY crosses are now bursting upwards

Fig 2: G-10 JPY crosses rolling 1-month performances as of 16 Jun 2023 (Source: TradingView, click to enlarge chart)

The weakness seen in the JPY against the USD has led to the continuation of the JPY carry trade medium-term uptrend phase where the GBP/JPY and AUD/JPY are now trading close to a 9 and 10-month high respectively.

US Dollar Index is looking weak again for a retest on its 100.95 key near-term support

Fig 3: US Dollar Index medium-term trend as of 13 Jun 2023 (Source: TradingView, click to enlarge chart)

The US Dollar Index (a weighted average of 6 currencies, EUR, JPY, GBP, CAD, SEK & CHF where the EUR has the highest weightage of around 57%) has just broken below its 50-day moving average after it traded above it since 12 May 2023. Medium-term momentum has turned bearish as the daily RSI oscillator has reintegrated below its former corresponding support at the 50% level.

A break below the 100.95 key near-term support which the US Dollar Index has managed to hold on the previous five occasions since 2 February 2023 may resume its major downtrend movement with the next support coming in at 97.85 in the first step.

{kind=link}