- China’s Premier Li Qiang’s morale booster speech during yesterday’s opening of the World Economic Forum’s 14th Annual Meeting of the New Champions ignited a bullish tone in China’s stock market.

- USD/CHH (offshore yuan) retreated from 7.2500 key intermediate resistance after PBoC’s indirect FX intervention yesterday.

- USD/CNH may strengthen further which may trigger another round of downside pressure in China-related equities.

China’s Premier Li Qiang, also the Head of the State Council that directs economic policies in China used his keynote speech yesterday, 27 June during the opening of the World Economic Forum’s 14th Annual Meeting of the New Champions in Tianjin to smooth out fears of a significant impending economic slowdown in the second half of 2023.

He informed the 1,500 forum attendees that consist of foreign-policy makers and global business leaders that China’s Q2 economic growth will be faster than the 4.5% recorded in Q1 and on track to achieve the annual GDP growth target of around 5% for 2023.

Morale booster on China’s H2 2023 growth trajectory but no details on new fiscal measures

Li Qiang stopped short of revealing any details on the highly anticipated new fiscal stimulus measures that the State Council discussed two weeks ago. But yesterday’s “confident boosting” speech by one of China’s top economic policymakers has triggered a broad-based rally in key China’s proxies benchmark stock indices that snapped five consecutive days of losses.

The Hang Seng China Enterprises Index ended yesterday’s session, 27 June with a gain of +2.08%, the Hang Seng Index added +1.88% and the Hang Seng TECH Index which comprises China’s mega-cap technology stocks outperformed with a rally of +2.57% and close back above its 50 and 200-day moving averages. The A-shares CSI 300 had a smaller gain of +0.94%.

Watch out for further Yuan’s weakness

Fig 1: USD/CNH medium-term trend as of 28 Jun 2023 (Source: TradingView, click to enlarge chart)

The offshore yuan has weakened considerably in the past four weeks where the USD/CNH staged a rally of +5% from its 4 May 2023 low to 27 June 2023 high of 7.2495 and such yuan weakness could spur capital outflows amid a weak internal demand environment that triggers a negative feedback loop back into the China’s stock market.

Given the recent hawkish rhetoric from the US central bank, Fed’s to keep interest rates higher for a longer period in the US has caused the 2-year sovereign bond yields between the US and China to widen further that put further downside pressure on the yuan which prompted China central bank, PBoC to step in yesterday by setting its opening daily reference rate higher than expected on the onshore yuan against the US dollar that led to a daily loss of -0.3% in the USD/CNH by the end of yesterday US session.

However, such indirect intervention by PBoC has been fruitless so far as the offshore USD/CNH has resumed its upside momentum today with an intraday gain of +0.13% at this time of the writing, and printed an intraday high of 7.2367, just a whisker away from its key immediate resistance of 7.2500.

Today’s current downbeat tone seen in the offshore yuan has been magnified by yesterday’s better-than-expected US economic data; Conference Board’s consumer confidence for June, and durable goods for May that increased the odds of the Fed’s upcoming two expected hikes on the Fed funds rate before 2023 ends which in turn may widen the differential of US-China’s 2-year sovereign bond yield spread further.

Failure to keep the 7.2500 resistance in check on the offshore USD/CNH may see another bout of yuan’s weakness towards the next resistance at 7.3450 (the major 25 Oct 2022 swing high area & the upper boundary of the long-term secular ascending channel in place since January 2014).

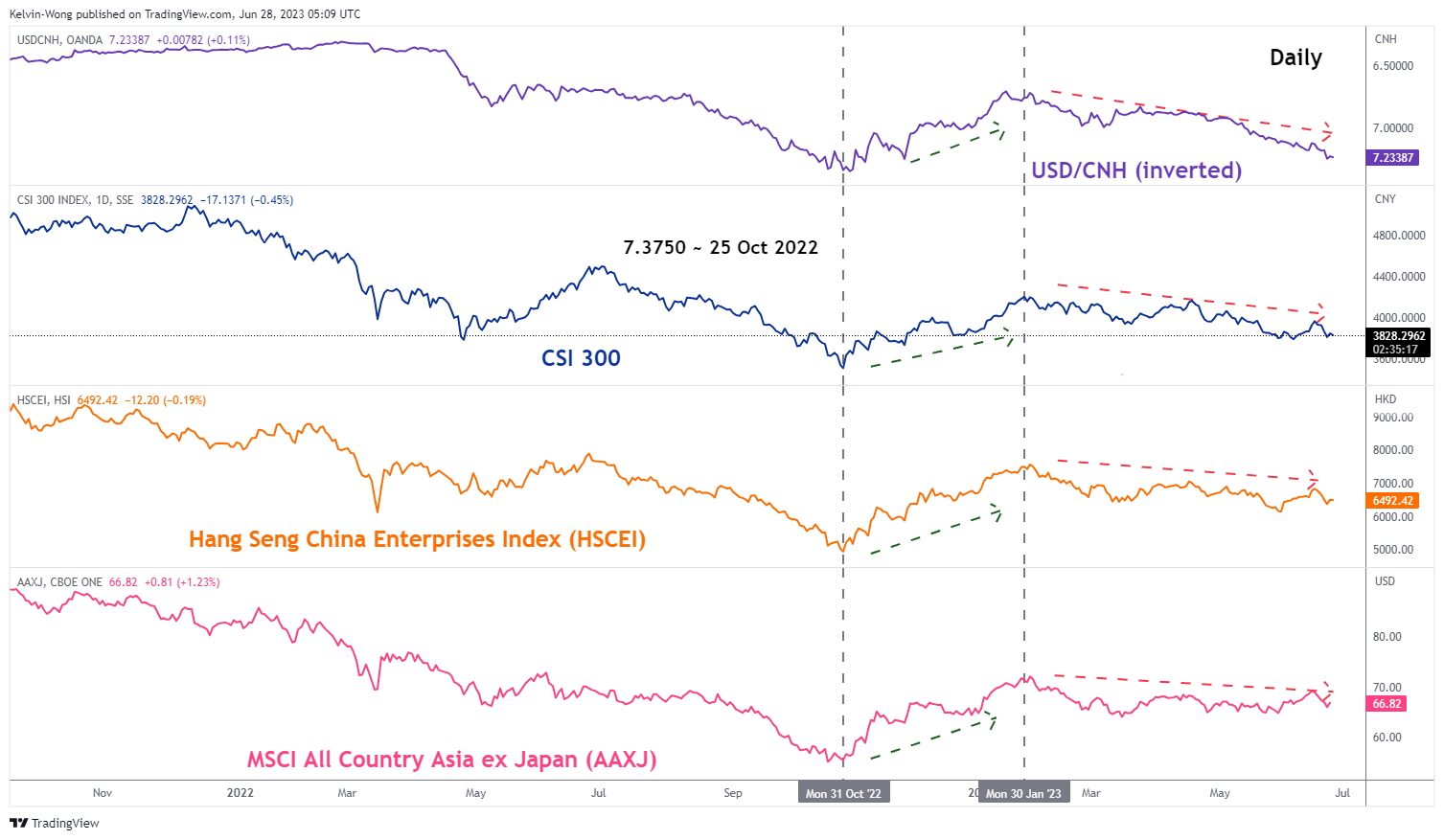

Yuan has moved in lockstep with China and Asia ex-Japan equities since October 2022

Fig 2: Yuan correlation with CSI, HSCEI & MSCI All Country Asia ex Japan as of 28 Jun 2023 (Source: TradingView, click to enlarge chart)

Since October 2022, the movement of USD/CNH (inverted) has had a strong direct correlation with China benchmark stock indices (CSI 300 & Hang Seng China Enterprise Index) as well as the Asia ex-Japan stock markets.

Hence, without any clear indication of the scope and implementation timing of the new fiscal stimulus measures from the State Council and clearance above the 7.2500 key intermediate resistance on the USD/CNH may dampen the short-term bullish mood and trigger another bout of downside pressure in China and Asian ex Japan equities in general.

{kind=link}