The Bank of Japan will announce its latest policy decision on Friday after concluding its two-day meeting. Speculation has been intensifying in the run up to the meeting about what the central bank will decide, as higher inflation has raised the possibility of another tweak to its yield curve control policy. Officials have tried to play down the prospect of a policy shift, but the Bank of Japan has a long track record of shocking the markets and so traders have good cause to be wary. This has provided some respite for the yen, even if it turns out to be temporary.

Inflation finally rears its ugly head

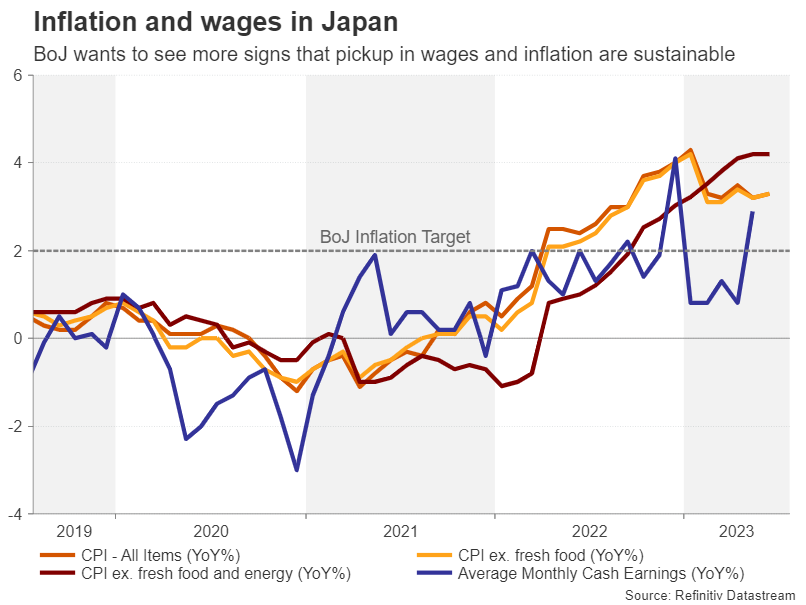

After decades of non-existent price pressures, inflation in Japan is finally headed in the right direction. The consumer price index rose at the fastest pace since the early 1990s back in January, hitting 4.3%. That is quite significant when considering that all the previous spikes in inflation over the last 30 years have been entirely down to increases in the sales tax. But the Bank of Japan isn’t celebrating quite yet. As other central banks fret about sticky inflation, the BoJ isn’t convinced that high inflation is here to stay in Japan. This need for caution is somewhat supported by the data.

Headline CPI appears to have peaked as it’s eased a little since January to just above 3.0%. Core CPI, which excludes fresh food prices and is the measure targeted by the BoJ to achieve 2% inflation, has also settled slightly above 3.0%.

However, when stripping out both food and energy prices from the CPI index, the annual rate of inflation stood at 4.2% in June and has yet to peak. When adding to the equation the effects of a weaker currency – the Japanese yen has depreciated by about 7% versus the US dollar this year – there is a reasonable argument to assume that inflation is set to stay above the BoJ’s 2% target for some time to come.

It’s all about sustained wage growth

Yet, like his predecessor, new governor, Kazuo Ueda, wants to see more evidence that inflationary pressures won’t dissipate once the pandemic and energy shocks have faded, and for that to happen, there has to be a domestically driven demand backdrop. Hence, all the focus on wage growth.

Some progress has been made; wage increases accelerated at the end of 2022 before falling back earlier this year. But there are positive signs that average cash earnings are starting to pick up again as they rose by 2.9% year-on-year in May.

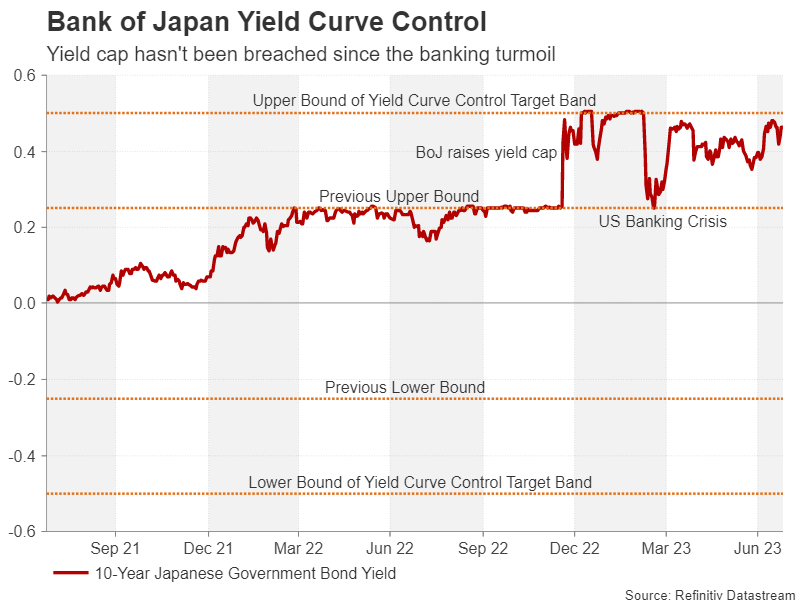

The big question now is whether or not these tentative signals that high inflation is becoming more embedded in the Japanese economy, and more importantly, in the Japanese people’s mindset, warrant another recalibration of the Bank’s yield curve control (YCC) policy. YCC was last adjusted in December when the target band on the 10-year JGB yield was widened by 25 basis points to 0.50% above and below zero percent.

The case for a BoJ shock

If the BoJ were to opt for another tweak, an increase in the band from ±0.50% to ±1.00% would be the likely scenario. The main case for the BoJ to act pre-emptively and catch markets by surprise is to avoid a situation where speculators push up the 10-year yield to the upper limit of the target band, forcing the Bank to make emergency bond purchases. The risk of a prolonged or intense pressure on the yield cap is that it could lead to a disorderly exit from yield curve control policy – something that would be hugely embarrassing for the BoJ as well as potentially costly.

A tweak now would keep speculators at bay well into 2024, buying policymakers some valuable time to properly assess the country’s changing inflation landscape. But most importantly, the Bank would in fact be prolonging the lifespan of YCC, enabling it to maintain an ultra-accommodative policy stance even as it allows the 10-year yield to climb to multi-year highs.

A boost for the yen? Maybe.

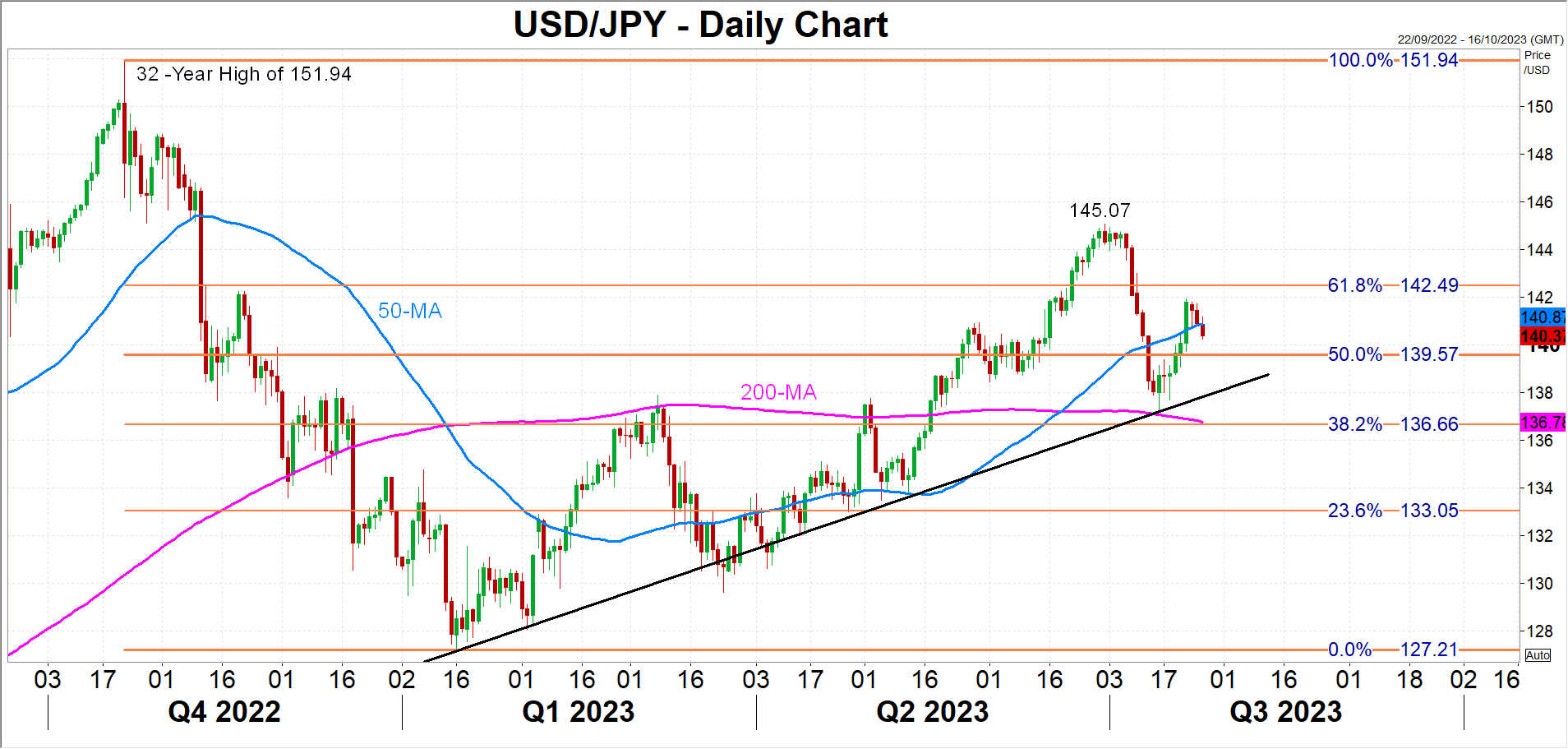

For the yen, a widening of the target band would come as welcome relief and the immediate reaction would be a spike higher. Dollar/yen could dip towards its ascending trendline before sellers target the 200-day moving average at 136.78 and the 133.00 congested region.

However, further gains would likely depend more on what the US Federal Reserve signals about its tightening plans and how the dollar responds to that. In the months ahead, if expectations about Fed rate cuts, or even a long pause, don’t materialize, a tweak in YCC policy might not be enough to prevent the yen from revisiting its 2023 and 2022 lows of 145.07 and 151.94 per dollar, respectively.

{kind=link}