Summary

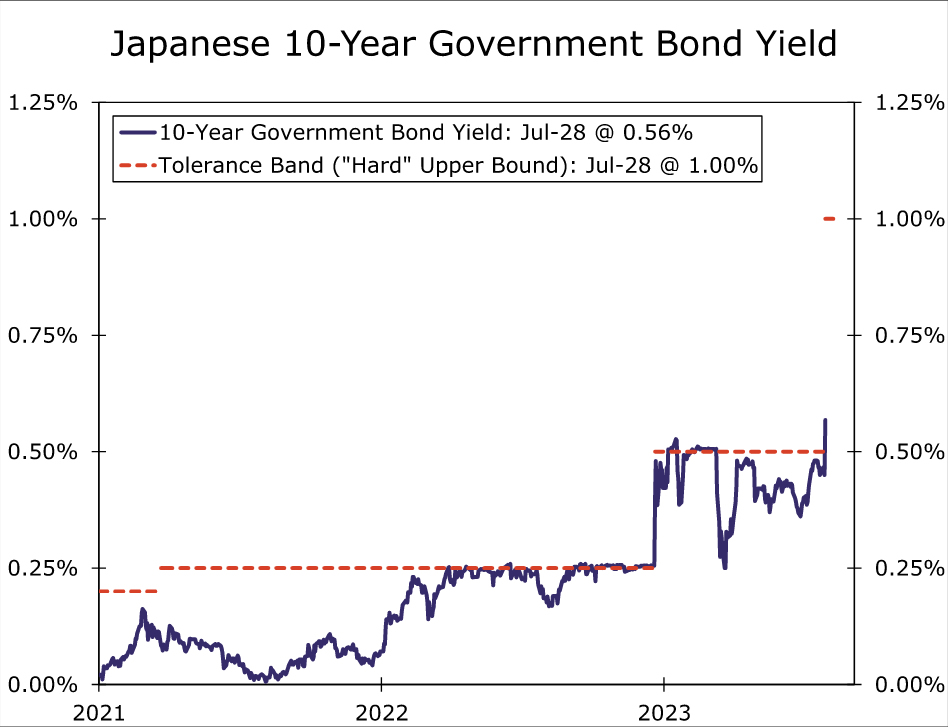

- The Bank of Japan (BoJ) sprung a surprise at today’s monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy. While the BoJ did not change its main policy parameters, it said it would conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.

- The BoJ also said it would offer to buy 10-year JGB’s at 1.00% every day through fixed-rate purchase operations if needed. In effect, the change means the Bank of Japan will cap 10-year JGB yields at 1.00% or, perhaps more accurately and in reality, somewhere between 0.50% and 1.00%.

- Overall, we view today’s policy adjustment as primarily driven by operational and tactical considerations. From a purely economic perspective, we think the case for a further shift to less accommodative monetary policy is growing but not yet overwhelming. From an operational perspective we also see limited likelihood of a further policy adjustment for now if, as we expect, global tightening is near an end, meaning global bond yields could stabilize and eventually move lower. Against this backdrop, we see Bank of Japan monetary policy as on hold for the foreseeable future, and certainly at least for the rest of 2023.

Bank of Japan Loosens Grip on Long Term Bond Yield

The Bank of Japan (BoJ) sprung a surprise at today’s monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy, a move that occurred a little sooner than the October adjustment we had forecast. With respect to its main policy parameters, the BoJ held its Policy Balance Rate at -0.10%, and said it would continue to target a 10-year Japanese Government Bond (JGB) yield of 0% with a fluctuation range of +/- 50 bps. Importantly however, the BoJ said it will “conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.” The Bank of Japan also said it would offer to buy 10-year JGB’s at 1.00% every day through fixed-rate purchase operations if needed. In effect, this change means the Bank of Japan will cap 10-year JGB yields at 1.00% or, perhaps more accurately and in reality, somewhere between 0.50% and 1.00%.

In our view, a cap of “somewhere between 0.50% and 1.00%” reflects comments from BoJ Governor Ueda, who said that depending on the situation yields could go beyond 0.50%, but that he didn’t expect long-term yields to get to 1.00%, nor did he think it was appropriate for yields to get to 1.00%. Ueda added that he did not view the move as a step towards normalization. The BoJ’s modestly upgraded economic projections also suggest only a moderate increase in the 10-year JGB cap to “somewhere between 0.50% and 1.00%”, with inflation not yet seen rising sustainably above 2%. The BoJ raised its core CPI forecast for FY2023 to 2.5%, but lowered in core CPI forecast for FY2024 slightly to 1.9%, while keeping at 1.6% for 2025. The central bank did however acknowledge that the risk to its inflation forecasts were to the upside. Separately, the BOJ lowered its GDP growth forecast for FY2023 slightly to 1.3%.

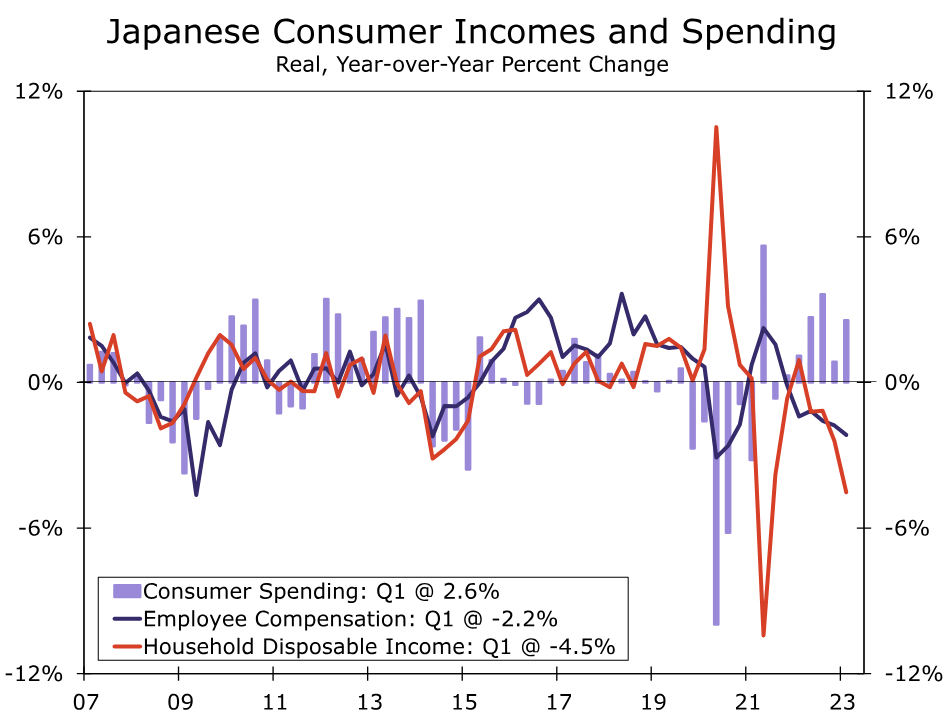

Overall, we view today’s policy adjustment as primarily driven by operational and tactical considerations, and against that backdrop, do not expect the BoJ to follow up with another policy adjustment in the near-term. From a purely economic perspective, the case for less accommodative monetary policy is growing but not yet overwhelming, in our view. With respect to economic growth prospects, it is true that Japan started 2023 on a firm footing, with Q1 GDP growing at 2.8% quarter-over-quarter annualized and the Q2 Tankan survey hinting at ongoing growth through the first half of the year. However, while wage growth has quickened it has not kept pace with the increase in prices, meaning that in real or inflation-adjusted terms, trends in employee compensation and household income have turned negative. The negative income trends could eventually restrain the consumer, and see Japan’s economy lose momentum over time. We also expect inflation to recede, and indeed the Bank of Japan’s own forecasts see inflation slowing back below 2% over the medium-term. Thus, from an economic perspective we do not see a strong rationale to tighten policy in the period ahead. From an operational perspective, we also see limited likelihood of a further policy adjustment for now. If, as we expect, global monetary policy tightening comes to an end in the immediate months ahead, upward pressure on global bond yields should ebb and, global bond yields could start moving lower. In this environment we would not expect 10-year Japanese government yields to rise close to the “hard” yield cap of 1.00% for the time being, and therefore do not envisage any significant new operational challenges for the Bank of Japan in terms of implementing monetary policy. Against this backdrop, we see Bank of Japan monetary policy as on hold for the foreseeable future, and certainly at least for the rest of 2023.

sprung a surprise at today's monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy. While the BoJ did not change its main policy parameters, it said it would conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.){kind=link}