Research China – Downside risks return

- Financial stress has increased again and put focus again on whether China is heading for a deeper financial and economic crisis.

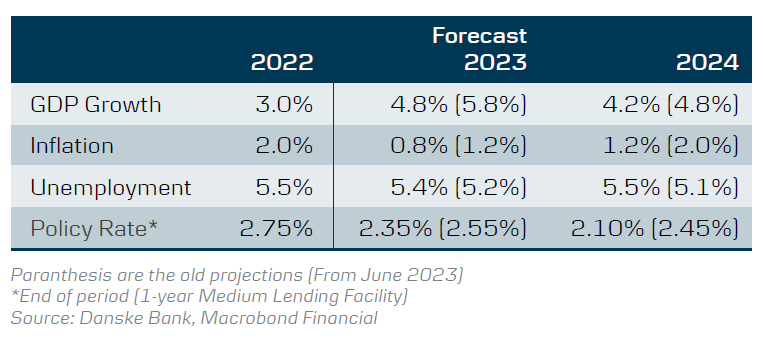

- While we do see a rising risk of this happening (25% probability), our baseline scenario remains that China has the tools to avert such an outcome and will use them to the extend needed. Yet, due to the recent weak data and rise in financial stress we recently revised down our forecast to 4.8% growth this year and 4.2% in 2024.

- China has already turned up the volume on policy measures such as easing of mortgage policies, tax cuts and infrastructure spending and we expect the government to do more if needed to keep growth close to the target of 5% this year.

Financial stress has increased again with another major developer, Country Garden, at brink of default. Contagion to the shadow banking system has also come to the surface with a big trust company, Zhongrung International Trust Co missing payments. On top of this economic data has disappointed across the board with both consumer spending, home sales and exports undershooting expectations in recent months. Taking these developments into account we have revised down growth to 4.8% this and 4.2% next year. In our baseline scenario we expect policy makers to step up stimulus as broadly signalled following the Politburo meeting in late July and to take more measures to improve financing channels for developers and lift home sales. We also expect them to provide the necessary lifelines to local governments and facilitate a restructuring of major shadow banking entities in distress. We believe they will still strive to reach their 5% target and do what is necessary to at least put a floor under growth so it does not fall below 4-4½%.

Half of the economy already in recession

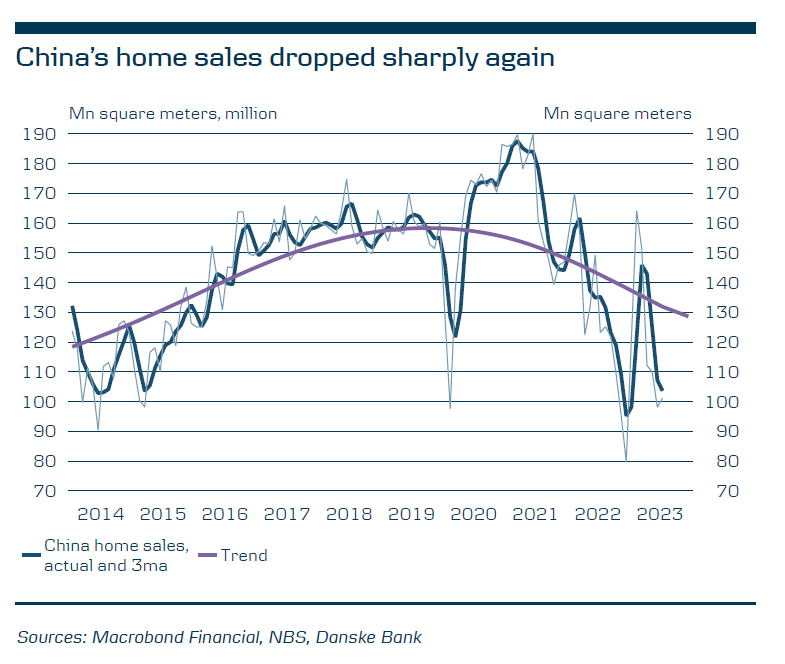

Of China’s different growth engines, housing and exports are the weak spots both being in recession. Together they constitute close to 50% of the economy. Private consumption and infrastructure investments have underpinned growth so far but there is a risk that the weakness in housing spreads to household spending, which would add further downward pressure on demand. It is crucial that Chinese policy makers step up further in stimulating housing to avoid this negative spiral. There is little China can do about the weak exports as a devaluation would risk creating more uncertainty and instability and China is unlikely to go down that path. China consumer prices fell into deflation in July as they declined 0.3% y/y. However, it was driven by energy and food and the core inflation that excludes these components were up 0.8% y/y. Hence, we are not yet seeing broad based deflation in China. We look for overall inflation to turn positive again over the next 6-9 months but that inflation generally stays low as demand is set to undershoot supply for some time.

China’s tool box is not exhausted yet

In early September China took new steps to support the economy by lowering mortgage rates and reducing the required down payments for house purchases. Early indications are that it has already spurred some home buyer interest but if needed China can ease more via these tools. Funding channels for developers can also be improved and on Friday18 August, PBOC and financial regulators met with bank executives telling them to direct more lending to support an economic recovery. China is also likely to cut Reserve Requirement Ratios (RRR) for banks to free up more liquidity to buy credit bonds and increase lending. The RRR for small and medium sized banks is 7.75% while it is 10.75% for large banks and thus has plenty of room to be lowered. Finally, if needed, China could opt for quantitative easing (QE) with PBOC buying bonds directly in the market. This would serve as a strong signal that they step in as lender of last resort.

China in a painful rebalancing of the economy

China is currently in a painful rebalancing where it needs to continue to wean itself off the reliance on housing as a structural demand driver and instead transition into an economy, where private consumption and high-tech manufacturing are the main drivers. Chinese leaders seem increasingly willing to pay a price to growth in the coming years from the lower levels of activity in the housing sector in order to achieve this rebalancing and get more capital allocated to more productive parts of the economy, not least high-tech manufacturing. The challenge is, though, to avoid that the decline in housing is so steep that it pulls down the consumer and investments with it. This is the risk China is currently facing and why we expect somewhat stronger measures to lift housing from the current depressed levels but not being so strong that they risk creating a new bubble.

{kind=link}