- September still a hold, while swap contracts suggest odds a 49.3% chance of a hike at the November 1st FOMC meeting

- Supercore inflation rate rises most since March

- Two-year Treasury drifts lower by 2.1 bps to 4.999%

Inflation is not easing enough for the Fed to abandon their hawkish stance. The upside surprises might be small, but that should keep the hawks in control. Core inflation heated up for the first time in six months and that should have markets leaning towards one more Fed rate hike in November. Inflation will likely still be running well above the Fed’s 2% target for the rest of the year, but a weaker consumer supports the case the disinflation process will remain intact.

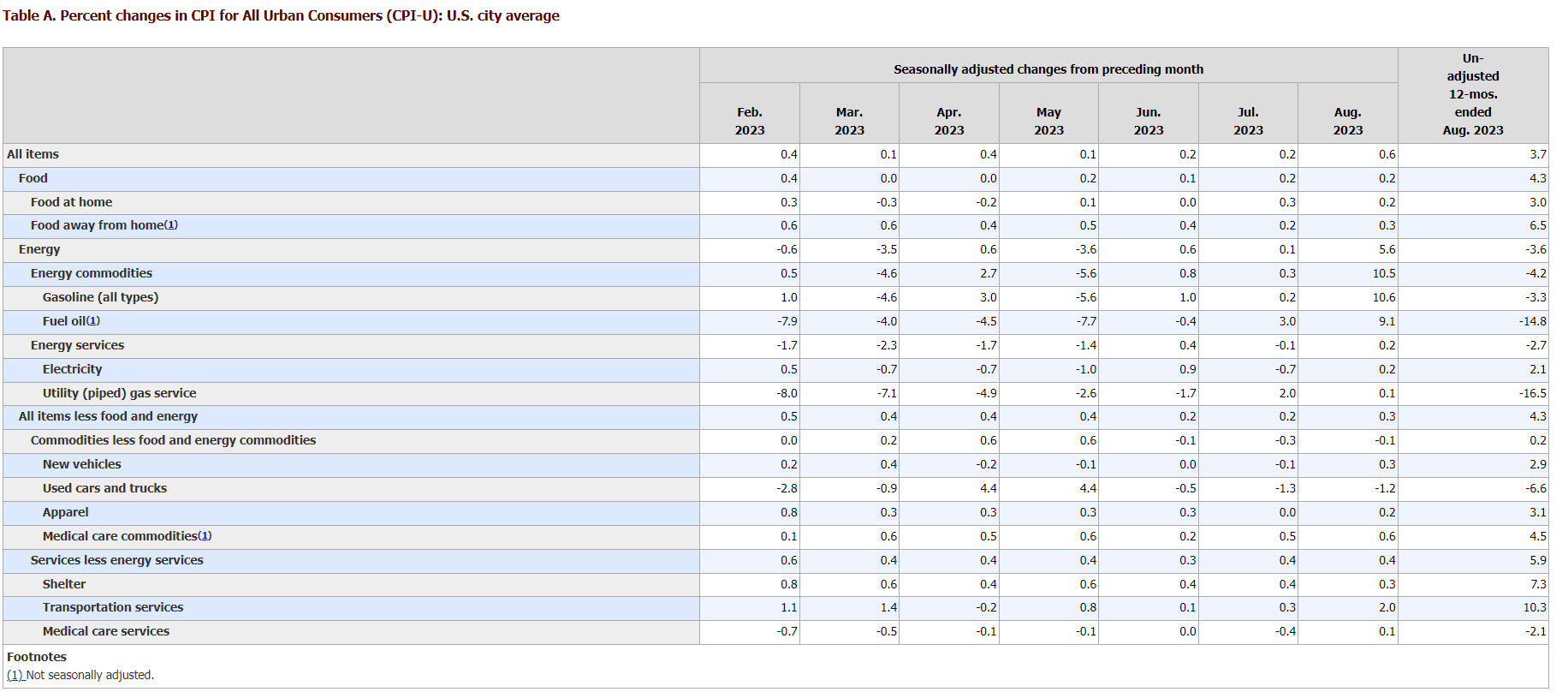

US CPI

Source: BLS

This was a complicated inflation report. Everyone knew that gas prices were sharply higher and that the housing market is still seeing elevated prices(house prices are now rising, while rents have eased). The headline inflation read showed CPI increased 0.6% in August from a month ago, which was the highest reading since June 2022. The annual inflation reading rose from 3.2% to 3.7%, a tick above expectations.

Market reaction

A weakening US consumer will continue as they battle surging gasoline prices, stubborn shelter prices, and increasing medical costs. US stocks are wavering as this inflation report will keep the Fed pushing the ‘higher for longer’ narrative. If Wall Street remains convinced that the labor market is cooling, that will do the trick for getting inflation closer to the Fed’s target.

The US dollar and Treasury yields were initially higher given the core CPI delivered an upside surprise, but once traders digested the entire report, the bond market reversed course. Core inflation rose 0.3%, which was due to the rounding of 0.278% which somehow makes it a lot less hot. Rent makes up 40% of Core PCE and prices posted the smallest gain since the end of 2021. Expectations are elevated for the consumer to be significantly weaker and that we could have a soft holiday spending season, which should support the disinflation process.

Dollar 5-minute Chart

The dollar is wavering as Wall Street wasn’t able to come up with any definitive stances on when the Fed will signal the all clear that policy is restrictive enough. The dollar’s strength is most notably against the Japanese yen, while the euro will likely react to Thursday’s ECB rate decision. Following yesterday’s Reuters report that the ECB will have inflation projections above 3%, markets appear to be leaning towards a rate hike.

{kind=link}