- Eurozone economy likely stagnated or contracted in third quarter

- Euro has been under selling pressure and could remain heavy

- Growth and inflation data will be released at 10:00 GMT Tuesday

Flirting with recession

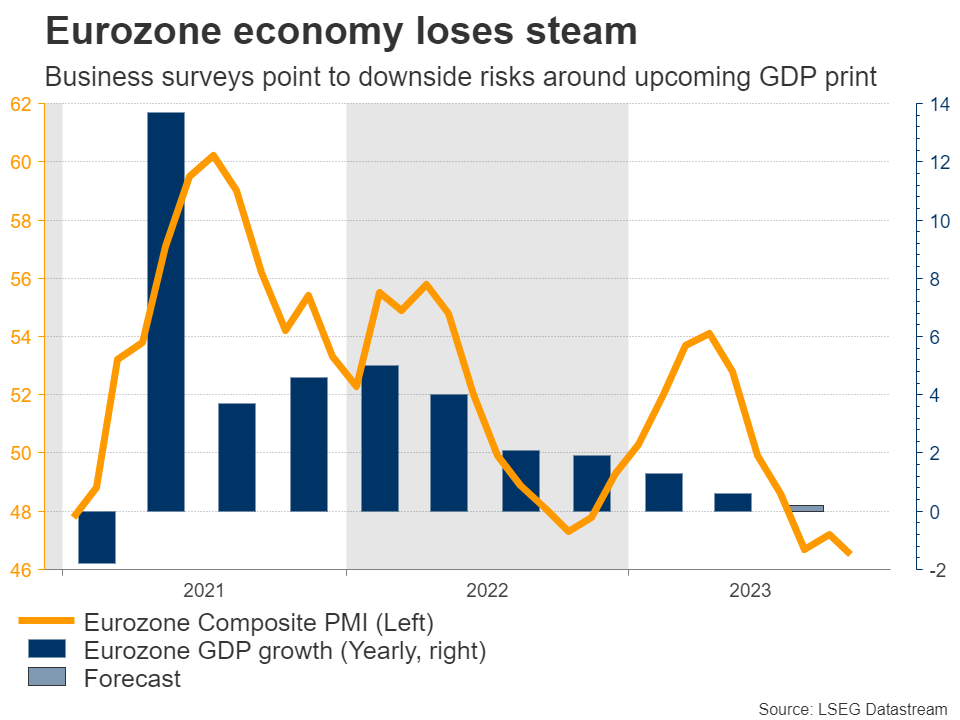

The Eurozone economy has struggled this year, as consumers have been squeezed by rising mortgage costs and elevated energy prices. Economic growth in the second quarter slowed to just 0.5% on a yearly basis, and business surveys warn that the situation will probably get worse, putting the risk of a mild recession on the radar.

Germany is responsible for much of this weakness. Haunted by the problems in global manufacturing and softer demand conditions among key trade partners such as China, the Eurozone’s largest economy has suffered serious damage and is on track to shrink 0.4% this year according to the German government’s own forecasts.

With recessionary clouds gathering, the European Central Bank has adopted a more cautious stance, signaling that interest rates have most likely reached their peak already, as inflation continues to cool off. In this sense, the question facing investors now is how soon interest rates will be cut, something that markets are pricing in for next summer.

GDP and inflation stats

Turning to the upcoming data releases, GDP growth in the Eurozone is projected to have stagnated in the third quarter, with forecasts pointing to 0% growth in quarterly terms. As for any potential surprises, the risks seem tilted to the downside.

Business surveys from S&P Global were consistent with a GDP contraction of 0.4% during the quarter, which suggests that there’s scope for a disappointment in this dataset relative to forecasts.

Similarly, inflation is anticipated to have fallen sharply in October, with the headline CPI rate expected to decline to 3.2% from 4.3% in the previous month. This was also reflected in business surveys, where firms reported the slowest increase in their selling prices since early 2021.

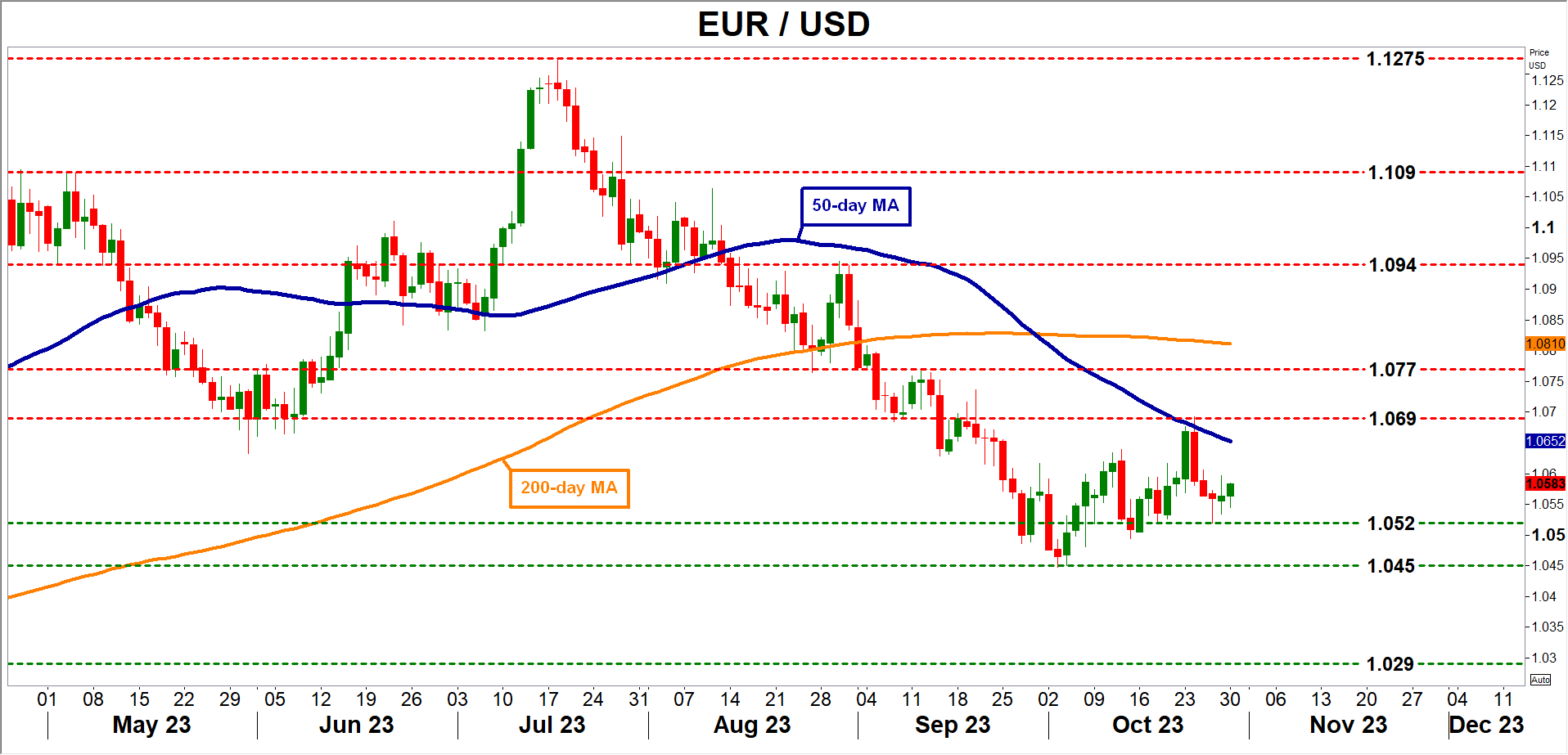

A potential disappointment in this dataset could fuel speculation that the ECB will cut rates even sooner than markets expect next year, and by extension inflict more damage on the wounded euro. Looking at the euro/dollar chart, the 1.0520 zone could act as an initial barrier to any downside moves. If sellers can pierce through, the focus would shift to the October low of 1.0450.

On the flipside, a surprisingly strong round of data releases could help the euro recover some ground. In this case, the recent local high near 1.0690 could come into play.

Euro outlook appears gloomy

In the big picture, there isn’t much to like about the euro at this stage. Germany’s export-driven business model has been decimated by high energy costs and sluggish growth in export markets like China, while sky-high borrowing rates continue to suppress consumer demand across Europe.

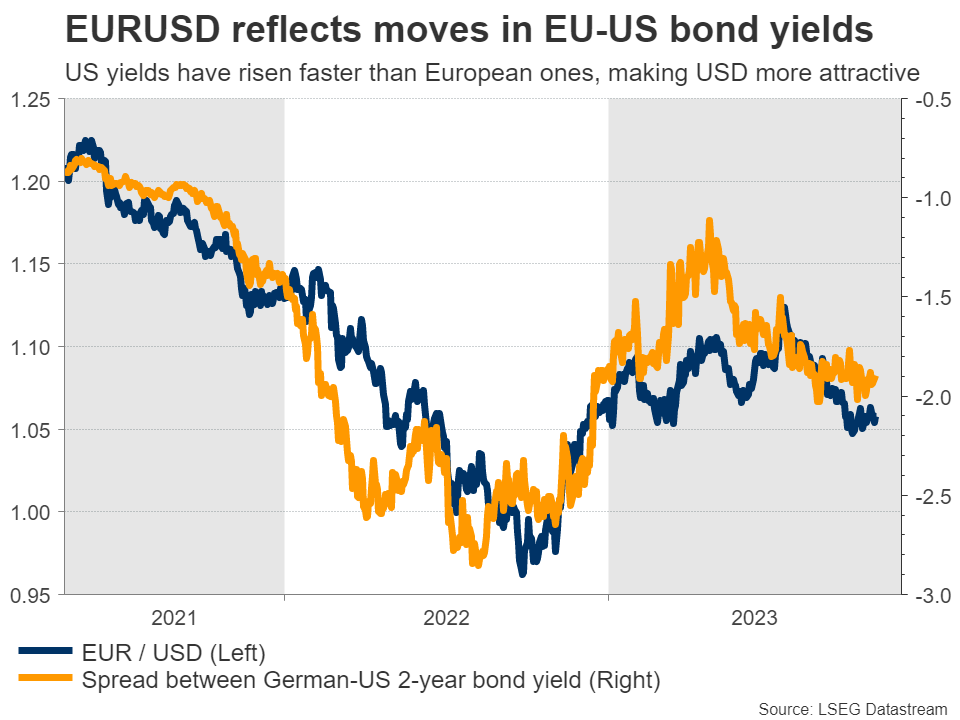

Worse of all, there’s no stimulus on the horizon to help safeguard economic growth. Most governments have reined in their pandemic-era spending measures and are hesitant to roll out new programs until inflation dies out. Therefore, the growth outlook is already dark and it probably needs to become even worse before European governments ride to the rescue.In contrast, the US economy is far more resilient. Economic activity even accelerated during the summer, with some help from powerful government spending. In other words, both interest rate and economic growth differentials currently favor the US over Europe, and as long as this is the case, the downtrend in euro/dollar might remain in force.

{kind=link}