Dollar remains stable in early US session despite release of another set of persistently high inflation figures. The strong rebound in DOW futures suggest that investors are somewhat relieved to see no disastrous surge in inflation rates. Additionally, robust spending growth appears set to continue bolstering the US economy, even as Fed is set to maintain higher interest rates for an for much longer.

Attention is turning back to Japanese Yen for the last hours of the week, which continues its steep decline. During his post-meeting press conference, BoJ Governor Kazuo Ueda provided little support to stabilize Yen. Ueda mentioned that the central bank would consider raising interest rates if new data supports its latest price forecasts or if inflation exceeds expectations. However, he did not specify any clear timing for rate adjustments. Furthermore, Ueda dismissed the possibility of a comprehensive reduction in bond purchases at this stage.

Regarding the exchange rate, Ueda remarked that the current weakness of the Yen has not significantly impacted the core inflation rates yet. He also noted that weak Yen could have some positive effects on demand which might influence core inflation in the medium to long term. The lack of heightened concern seems to indicate that it’s not time for Japan to intervene yet.

The weekly performance chart hasn’t changed too much. Yen is staying as the worst performer, followed by Swiss Franc and then Dollar. Aussie is the best, followed by Sterling, and then Kiwi. Euro and Canadian are positioning in the middle.

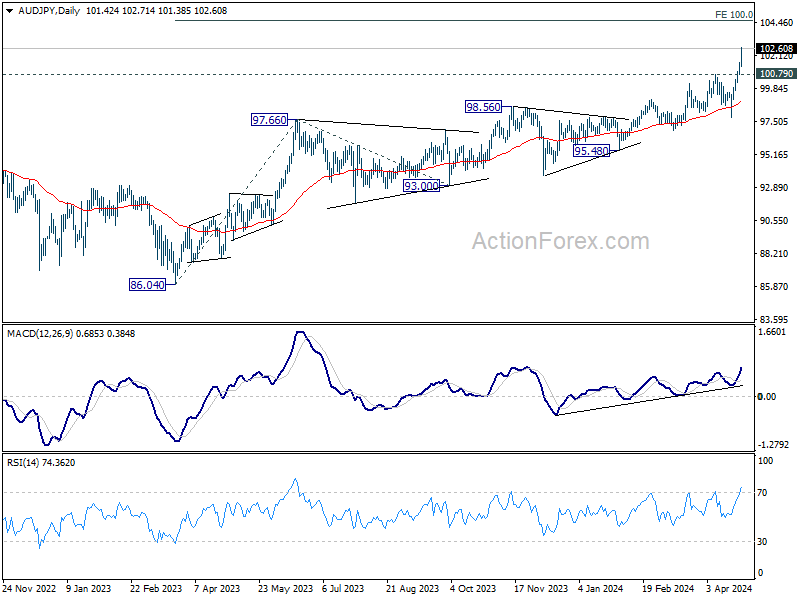

Technically, AUD/JPY is currently the top gainer for the day and the week. Further rally is expected as long as 100.79 resistance turned support holds. Next target is 100% projection of 86.04 to 97.66 from 93.00 at 104.62

In Europe, at the time of writing, FTSE is up 0.56%. DAX is up 0.90%. CAC is up 0.57%. UK 10-year yield is down -0.024 at 4.347. Germany 10-year yield is down -0.034 at 2.600. Earlier in Asia, Nikkei rose 0.81%%. Hong Kong HSI rose 2.12%. China Shanghai SSE rose 1.17%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield surged 0.0304 to 0.928.

US PCE inflation rises to 2.7% yoy in Mar, core PCE steady at 2.8% yoy

US personal income rose 0.5% mom or USD 122.0B in March, matched expectations. Personal spending rose 0.8% mom or USD 160.9B, above expectation of 0.6% mom.

Both headline and core PCE price index rose 0.3% mom, matched expectations. Prices for services increased 0.4% mom and prices for goods increased 0.1% mom. Food prices decreased less than -0.1% mom and energy prices increased 1.2% mom.

Over the 12-month period, headline PCE accelerated from 2.5% yoy to 2.7% yoy, above expectation of 2.6% yoy. Core PCE price index was unchanged at 2.8% yoy, above expectation of 2.6% yoy. Prices for services increased 4.0% yoy and prices for goods increased 0.1% yoy. Food prices increased 1.5% yoy and energy prices increased 2.6% yoy.

SNB’s Jordan: New shocks can occur any time

Speaking at SNB’s annual shareholder meeting, President Thomas Jordan highlighted the achievement in lowering inflation to below 2%, a milestone that enabled the bank to implement a rate cut last month.

Despite this progress, Jordan emphasized the continuing high levels of uncertainty in the global economic environment, acknowledging the potential for new shocks at any time.

“In the current environment, uncertainty remains elevated, and new shocks can occur at any time,” he noted. “We will therefore monitor the ongoing development of inflation closely and adjust our monetary policy again if necessary.”

BoJ stands pat, lower growth and higher inflation this year

BoJ left overnight call rate unchanged at 0-0.10% as widely expected, by unanimous vote. The BOJ says it will continue its Japanese government bond (JGB) purchases “in accordance with the decisions made at the March 2024 monetary policy meeting.”

Real GDP growth forecasts for fiscal 2024 was lowered sharply to 0.8%. But growth is expected to pick up moderately to 1.0% subsequently. CPI core forecasts was fiscal 2024 was raised to 2.8% and then slowed to 1.9% onwards. CPI core- core forecasts were left unchanged for both fiscal 2024 and 2025 at 1.9%. Fiscal 2026 CPI core-core is projected to pick up to 2.1%, which is a positive sign.

Real GDP growth forecasts:

- Fiscal 2024 at 0.8% (downgraded from 1.2%).

- Fiscal 2025 at 1.0% (unchanged).

- Fiscal 2026 at 1.0% (new).

CPI core forecasts:

- Fiscal 2024 at 2.8% (upgraded from 2.4%).

- Fiscal 2025 at 1.9% (upgraded from 1.8%).

- Fiscal 2026 at 1.9% (new).

CPI core-core forecasts:

- Fiscal 2024 at 1.9% (unchanged).

- Fiscal 2025 at 1.9% (unchanged).

- Fiscal 2026 at 2.1% (new).

Japan’s Tokyo CPI falls sharply to 1.6% yoy in Apr, vs exp 2.2% yoy

Japan’s Tokyo CPI showed significant slowdown in April. CPI core (excluding food) dropped from 2.4% yoy to 1.6%, substantially below the expected 2.2% yoy.

CPI core-core, which excludes both food and energy, also slowed from 2.9% yoy to 1.8% yoy, marking the slowest pace since September 2022.

Services inflation, a significant component of the CPI, decreased from 2.7% yoy to 1.6% yoy. This notable drop is largely attributed to policy interventions by the Tokyo metropolitan government to make some educational tuition free.

Overall headline CPI, which includes all items, also fell from 2.6% yoy to 1.8% yoy.

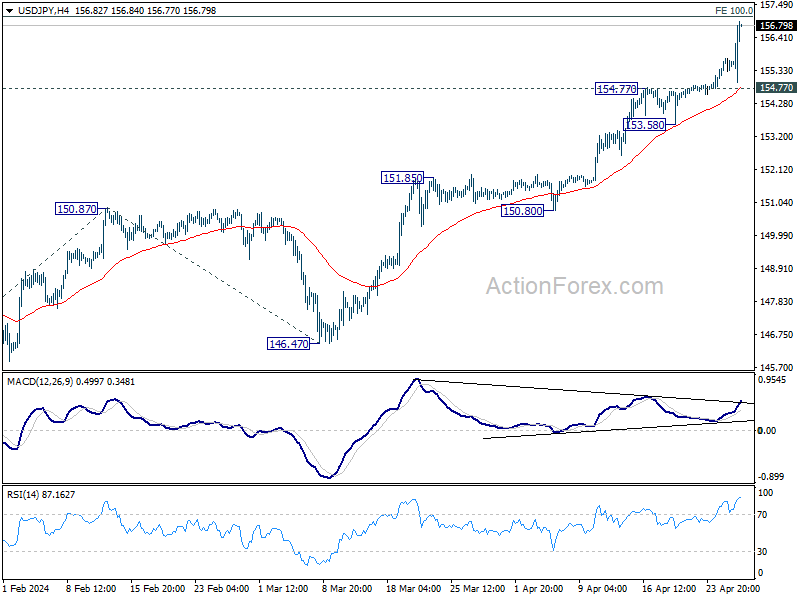

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.32; (P) 155.53; (R1) 155.87; More…

Intraday bias in USD/JPY remains on the upside for 100% projection of 140.25 to 150.87 from 146.47 at 157.09. Some resistance could be seen there to bring retreat. But further rally is expected as long as 154.77 resistance turned support holds. Sustained break of 157.09 will target 138.2% projection at 161.14 next.

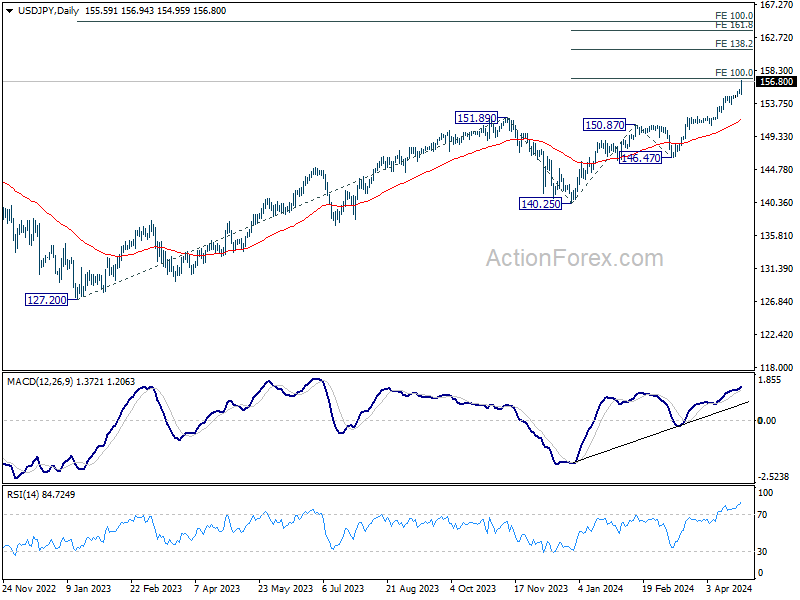

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Apr | -19 | -20 | -21 | |

| 23:30 | JPY | Tokyo CPI Y/Y Apr | 1.80% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Apr | 1.60% | 2.20% | 2.40% | |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Apr | 1.80% | 2.90% | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | -1.80% | 0.10% | 1.10% | |

| 01:30 | AUD | PPI Q/Q Q1 | 0.90% | 0.90% | ||

| 01:30 | AUD | PPI Y/Y Q1 | 4.30% | 4.10% | ||

| 03:22 | JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 0.90% | 0.50% | 0.40% | |

| 12:30 | USD | Personal Income M/M Mar | 0.50% | 0.50% | 0.30% | |

| 12:30 | USD | Personal Spending Mar | 0.80% | 0.60% | 0.80% | |

| 12:30 | USD | PCE Price Index M/M Mar | 0.30% | 0.30% | 0.30% | |

| 12:30 | USD | PCE Price Index Y/Y Mar | 2.70% | 2.60% | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 2.80% | 2.60% | 2.80% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 77.9 | 77.9 |

{kind=link}