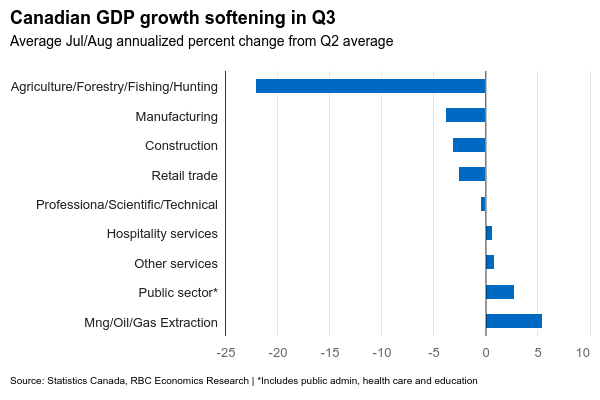

The advance estimate from Statistics Canada was that September Canadian manufacturing sales edged down 0.1% from August, despite another monthly surge in petroleum and coal prices. Manufacturing prices were up ~1% in September on a seasonally adjusted basis by our count, implying the volume of sales (excluding price impacts) declined even more after already contracting 0.7% in August. Indeed, economic growth in Canada is starting to look substantially softer. Consumer related sectors have weakened significantly – retail sales are tracking below Q2 levels to-date in Q3 and hospitality services (like restaurants and hotels) have flatlined. But cooling demand globally is also filtering down supply chains and slowing manufacturing output with the broader economy on track for another small quarterly decline in Q3.

Across the border, spending among US consumers has been much more resilient. Retail sales grew at an average pace of 0.5% per month in Q3, almost double the rate in pre-pandemic 2019. Next week’s October data will be among the first indications of how much of that momentum carried into Q4 (and the important holiday shopping period). We continue to expect strength in consumer spending to wane. October marked the restart of the student loan repayment program, and labour market conditions in the U.S. are starting to deteriorate. Employment growth has remained positive, but the rise in the unemployment rate over the last three months is similar to what has usually been seen at the start of a downturn in labour markets. The U.S. Fed will be watching next week’s October U.S. CPI report closely. Inflation pressures ticked higher in September – breaking a string of softer price growth readings. But a drop in gasoline prices should push headline year-over-year CPI growth lower in October. Core CPI in September was propped up by a larger increase in the owner’s equivalent rent index but that was not expected to be repeated this month. As indicated by Powell in his speech at the IMF yesterday, the Fed is still willing to hike interest rates further if needed. But we continue to expect slower consumer spending and deteriorating labour market conditions will keep the central bank on the sidelines, before pivoting to gradual rate cuts in the second quarter of next year.

Week ahead data watch

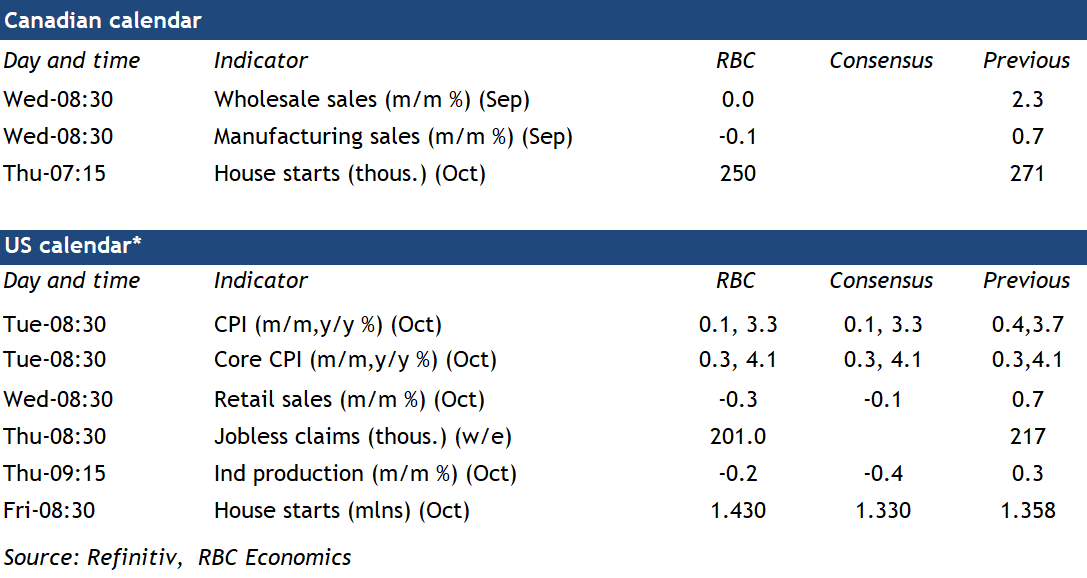

Canadian manufacturing sales likely inched down 0.1% in September, primarily driven by lower sales in metal and transportation equipment subsectors and despite a sharp price-led increase in petroleum sales.

Core wholesale sales are expected to remain unchanged from the prior month, in line with Statistics Canada’s early estimate. The preliminary estimate showed sales in auto and food subsectors with the largest increases, offsetting a pullback from machinery and equipment sales.

We anticipate U.S. retail sales to edge down 0.3% in October. Gasoline station sales likely fell on lower prices.

We look for a pullback in industrial production (-0.2%), with lower outputs in manufacturing and utility sectors.

declined even more after already contracting 0.7% in August. Indeed, economic growth in Canada is starting to look substantially softer. Consumer related sectors have weakened significantly – retail sales are tracking below Q2 levels to-date in Q3 and hospitality services (like restaurants and hotels) have flatlined. But cooling demand globally is also filtering down supply chains and slowing manufacturing output with the broader economy on track for another small quarterly decline in Q3.){kind=link}