- At today’s monetary policy meeting the BoE left the key policy rate unchanged at 5.25% as widely expected.

- The BoE delivered hawkish communication in an attempt to push-back on markets expectation of rate cuts next year.

- EUR/GBP declined on the back of the statement but fully retraced the move following the ECB meeting, in line with our expectation.

As expected, the Bank of England (BoE) decided to keep the Bank Rate (key policy rate) unchanged at 5.25%. The vote split mirrored that of the November meeting as 6 members voted for an unchanged decision and 3 members voted for an increase of 25bp in the Bank Rate.

The majority of the Monetary Policy Committee (MPC) voted to keep the Bank Rate unchanged citing that, although some news in key data have been to the downside since the MPC’s previous decision, changes to the overall outlook look limited. Additionally, the group noted that it was too early to conclude that services price inflation and pay growth were on a firmly downward path, indicating that talks of rate cuts were still premature.

As expected, focus of the statement and minutes, as seen with recent MPC commentary, was to push back expectations on rate cuts in order to prevent financial conditions from easing prematurely. The BoE reiterated that “monetary policy will need to be sufficiently restrictive for sufficiently long” and “is likely to need to be restrictive for an extended period of time“. The BoE retained its forward guidance repeating that “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures“. Likewise, in a broadcast interview following the release of the statement, Governor Bailey noted that it is too early to speculate about rate cuts and that he could not definitively say that rates have already peaked.

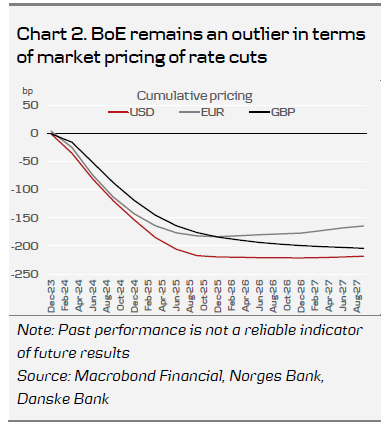

Overall, we expect the UK economy to show further signs of weakness, inflation to level off and wage growth to have peaked as shown by recent data releases. Coupled with global momentum and more rate cuts being priced in for peers, we expect this to spill over to the BoE pricing (in line with our call).

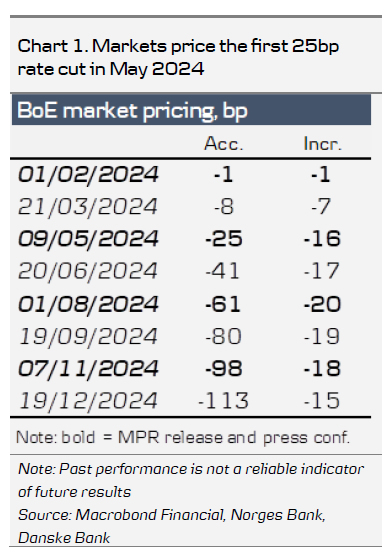

Rates. Overall, the reaction in rates markets was relatively muted. 2Y Gilt yields moved 5bp higher on the statement but remain more than 20bp lower than Monday’s highs. While the SONIA-curve inverts from Q1’24 the first 25bp rate cut is not priced before May 2024.

FX. Following the release of the statement, EUR/GBP moved lower, breaching the 0.86 mark but fully retraced the move during the afternoon. Overall, we see relative rates as a negative for GBP and see the recent rebound as attractive levels to sell GBP. We continue to forecast EUR/GBP to move modestly higher the coming year to 0.89.

Our call. We expect the first rate cut of 25bp in June 2024 and subsequently 25bp cuts in the following quarters, totalling of 75bp of cuts for 2024. This is less than current market pricing (110bp). We do not see the BoE deviating from the Fed and ECB by the extent currently priced by markets and expect markets to scale back on expectations from the latter.

decided to keep the Bank Rate (key policy rate) unchanged at 5.25%. The vote split mirrored that of the November meeting as 6 members voted for an unchanged decision and 3 members voted for an increase of 25bp in the Bank Rate.){kind=link}