- US dollar re-energized as strong data, hawkish Fed dent early rate cut bets

- American economy still churning out new jobs, shows no signs of cracks

- Will hot economy scupper the Fed’s plan to ease policy this year?

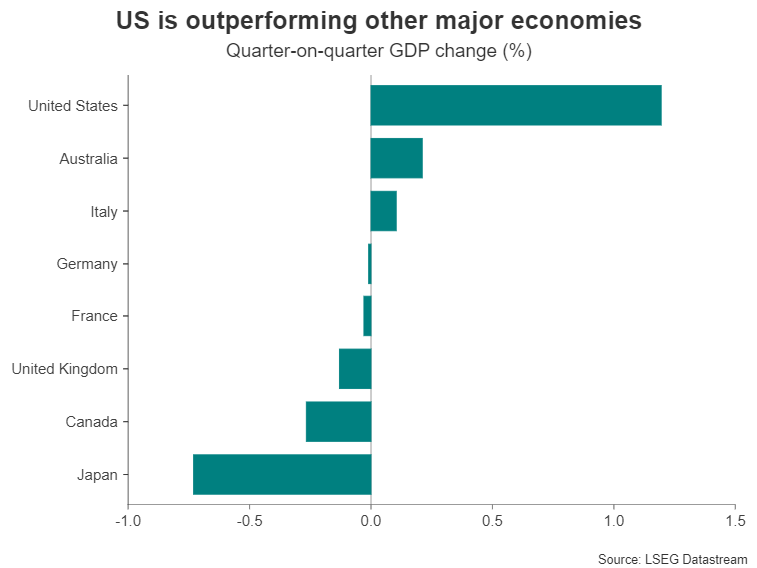

From recession fears to overheating risk

The US dollar may have ended 2023 on a bearish note as rate cut speculation reached fever pitch, but that has certainly not set the tone for 2024. In fact, the greenback rallied in the first week of January and the year-to-date uptrend received a solid endorsement on Friday when an upside surprise in the latest jobs report diminished hopes that the Federal Reserve would begin cutting rates as early as the March meeting. An equally stellar ISM services survey on Monday further cast doubt on the notion that policy easing is just around the corner.

Many investors are still holding out for a spring cut later in May, but even that may be too optimistic. As Chair Powell hinted at last week’s FOMC press briefing and in a subsequent interview, the Fed is in no rush to lower rates when the economy is so strong. Market odds for a May decrease currently stand at around 75%, leaving scope for a significant repricing if jobs growth and inflation don’t cool substantially enough over the next couple of months.

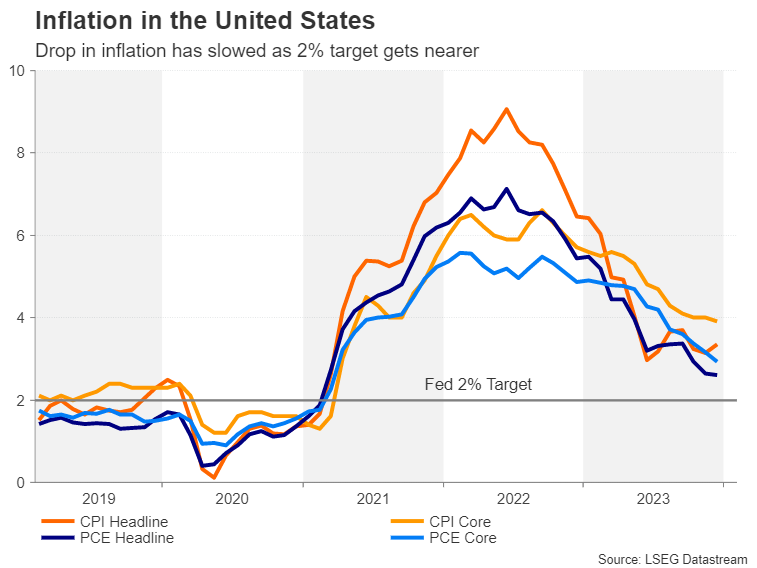

Fall in inflation has slowed down

However, neither is it completely right to say that markets are not paying attention to the data. Investors have priced out about 50 basis points of cuts for 2024 from where things stood in mid-January when easing bets peaked at around 165 bps. Nevertheless, there’s a danger that markets are too slow in dialling back their very dovish expectations and the Fed on its part isn’t being forceful enough in pushing back.

That leaves plenty of room for a further adjustment in market expectations should the inflation picture not pan out as most investors are hoping. The Fed is fairly confident that inflation is headed towards the 2% target in a sustainable manner, but there’s also likely to be some frustration that this final leg of the journey is taking longer than anticipated.

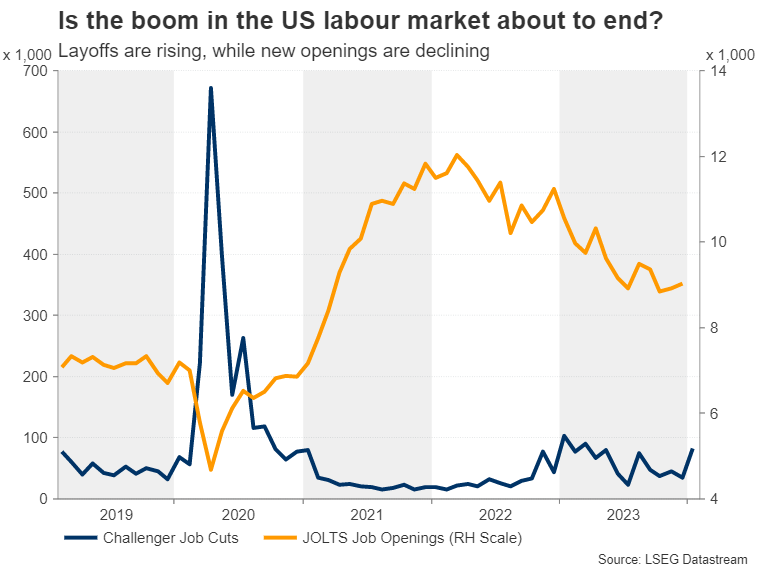

The labour market puzzle

Even if the disinflation process were to speed up over the next few months, Fed officials are unlikely to throw caution to the wind as long as the labour market remains so tight. The most worrying aspect of the January payrolls report was that annual wage growth unexpectedly accelerated to 4.5%, with average earnings rising by a whopping 0.6% month-on-month.

Those impressive readings might not be repeated soon as many Wall Street giants have announced a fresh round of layoffs. But they still suggest that the economy is at greater risk of running too hot than slowing down abruptly, with the soft landing narrative now looking increasingly like the base case scenario.

Is Fed policy restrictive enough?

Unless the labour market takes a turn for the worse, the Fed’s own ‘conservative’ forecast of 75 bps of cuts in 2024 could also start to come into question soon. As long as more jobs are being created than lost and wages are rising faster than inflation, consumers will keep spending and the risk of a recession will stay remote.

It doesn’t help that financial conditions have loosened substantially since November, as not only have Treasury yields tumbled by around 100 bps, but also stocks have climbed to fresh record highs. The Fed is partly to blame for this by appearing too eager to lean towards the dovish side. The latest gains on Wall Street have the potential to refuel consumer spending, which could prompt the Fed to wait until the summer before considering the first rate reduction.

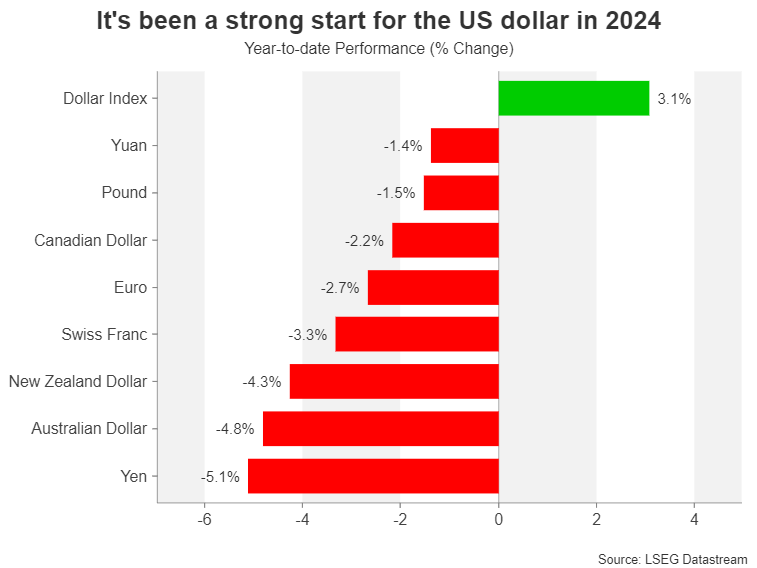

The case for a bullish dollar

All this makes the case for a weaker dollar less plausible in the first half of the year, particularly against the likes of the euro. With economic activity in the euro area remaining subdued and showing no sign of picking up, the European Central Bank is more likely to cut rates before the Fed does, making it difficult for the single currency to resume its late 2023 uptrend.

Of all the major currencies, the yen probably has a bigger chance of bouncing back against the US dollar should the Bank of Japan finally decide to end its negative interest rate policy. The BoJ has flagged April as the possible meeting to hike rates should this year’s spring wage negotiations result in large enough pay hikes.

For other currencies like the pound and Australian dollar where rate cuts could also be delayed by their central banks, it will be difficult for them to match the strong fundamentals for the US dollar, so until the Fed makes its pivot, they look set to stay on the backfoot.

Further bolstering the greenback’s prospects in the first few months of 2024 are the heightened geopolitical threats amid the spiralling conflict in the Middle East, which is supporting demand for safe havens.

A summer rate cut?

Heading towards the second half, however, the picture might start to change if the Fed does finally embark on a rate cutting cycle. The main problem with this scenario is that beyond the initial selloff, there may be limited downside for the dollar thereafter if the US economy remains comparatively more robust, preventing yield spreads with other currencies from narrowing significantly.

On the whole, however, it seems that the stars are gradually aligning for the dollar bears. The continued weakness in energy prices bodes well for a further decline in inflation over the coming months, allowing the Fed to lower rates even if there’s no downturn in sight, although this outlook is dependent on there not being a wider fallout of the Israel-Hamas war.

Barring any fresh crises or external shocks, the biggest threat to the US economy might be businesses reducing their workforce much more aggressively in 2024. With employment being one half of the Fed’s dual mandate, policymakers would not hesitate to slash borrowing costs if the labour market deteriorated.

Election and soaring deficit risks

There are other risks too that could become more prominent in the second half of the year. First is the presidential election in November, with Trump and Biden poised for a rematch. The former supports tax cuts and the latter favours more spending so neither would necessarily be negative for the markets. But Trump’s unpredictability and Biden’s age are something that could make the markets nervous if that’s the reality facing voters come November.

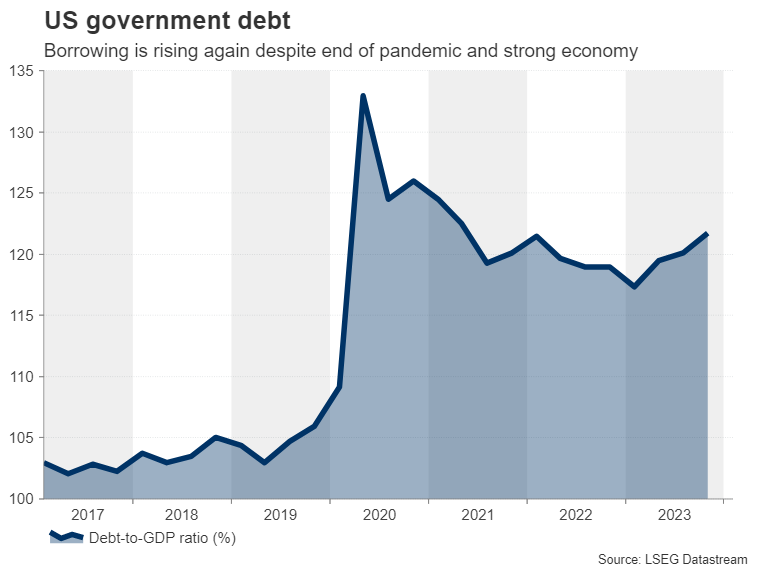

Finally, America’s ballooning debt poses both upside and downside risks for the dollar in 2024. Government borrowing surged in 2023 despite faster economic growth and pandemic-era spending being phased out. But the deficit could be even higher in 2024. Should Congress maintain the current course and debt jitters re-emerge, yields could spike higher, boosting the greenback in the short term.

Alternatively, if Congress decided to rein in some of the spending, tighter fiscal policy would give the Fed more room to cut rates, adding to the dollar’s potential downfall.

Best of the bunch

All in all, a major reversal in the dollar’s fortunes appears to have been pushed back again, in line with expectations of the Fed’s first rate cut. But just as there’s little reason for the Fed to move prematurely, it’s almost certain that a pivot is coming at some point this year. The gripe here is that when that happens, the scale of the cuts will probably disappoint, but perhaps more importantly, investors will still struggle to find better alternatives to the dollar.

{kind=link}