- We do not expect the Fed to make monetary policy changes in its March meeting, as broadly anticipated by both markets and consensus.

- Besides the obvious focus on rate cut timing cues, we will keep an eye on the updated rate and economic projections as well as more detailed discussion on QT.

- We think the Fed will cut rates for the first time in May and start to gradually phase out QT only from September. 2024 GDP forecast is set to be revised higher, but we think ‘dots’ will still signal three rate cuts for this year as a whole.

The Fed is set to balance upside surprises in recent inflation data with still cooling growth signals when it discusses monetary policy outlook for the rest of the year. Inflation data received after the January meeting has been concerning. Underlying services price pressures have remained elevated in early 2024, as we discussed in our Global Inflation Watch, 12 March, after this week’s CPI release.

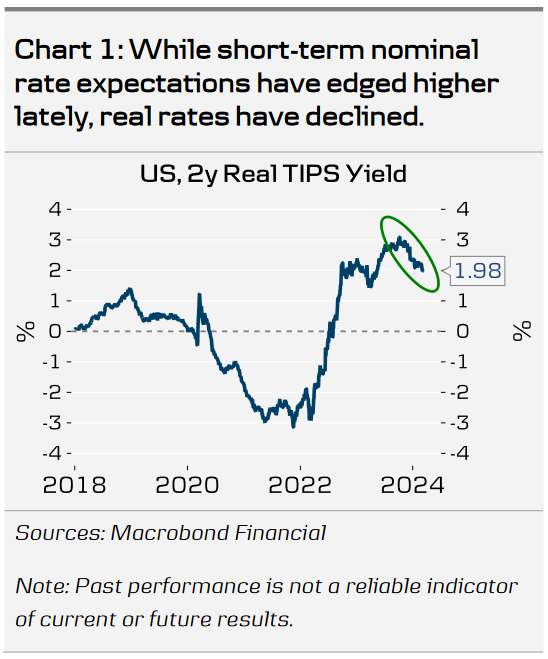

Inflation expectations have flashed warning signs as well. Even if longer-term expectations remain well anchored close to the Fed’s target levels, short-term break-evens have risen over the past weeks. NY Fed’s 3y survey-expectation also rose in February, albeit from a low level. While the current level of inflation expectations remains well below past years’ highs, and is by no means concerning as such, rise in expected inflation pushes real interest rates lower, causing monetary policy to turn less restrictive (Chart 1).

Growth overhang from strong Q4 will likely lead to an upward revision of 2024 GDP forecast. But with recent weaker signals from ISM, hiring and retail sales, we think Powell is likely to reiterate that tight monetary policy is still expected to weigh on growth over the coming year. Inflation forecasts will likely only receive minor tweaks, and we think the widely followed median ‘dot’ will still point towards three rate cuts this year.

The Fed is also set to discuss the endgame for QT, but we do not expect concrete signals about phasing out the balance sheet reduction quite yet. Bank reserves stand above USD 3600bn today, or around USD 600bn higher than a year ago despite the ongoing QT. This is a result of money market funds withdrawing funds from the Fed’s ON RRP facility and the Bank Term Funding Program (BTFP) introduced a year ago after the collapse of SVB. Over the next year, the remaining drawdown of ON RRP will add another USD 460bn to bank liquidity, while maturing BTFP will reduce it by USD 163bn. Treasury General Account (TGA) is currently very close to its target level (USD 768bn vs. target of USD 750bn), meaning it is unlikely to contribute to sharp swings in liquidity in 2024.

We believe the Fed will start to phase out QT by halving the pace of reductions only in September. Given the assumption above, bank liquidity would still hover roughly around $3000bn one year from today, which is most likely well above minimum ample level. In any case, we doubt the policymakers feel urgent need to communicate details about changing the pace of QT. Continuing balance sheet reduction will help maintain financial conditions restrictive even when the Fed will soon look to cut rates for the first time. We still look for total of three cuts this year, starting from May.

Markets: We expect a muted reaction

Long-end US rates will most likely react modestly to the outlined scenario for next week’s

meeting, with a slight upside risk from QT communication. The pricing of rate cuts this

year has converged close to the 75bp, which we believe the dot plot will continue to signal,

and the great uncertainty still rests on whether growth and inflation data will continue

surprising to the upside in the coming months. Our 12M target for the 10-year yield remains

at 4.25%, thus close to the current level. The same goes for the USD; we do not expect a

major reaction. If anything, the USD could broadly gain strength in the G10 space if the

upside risk to long-end US yields materializes. Our EUR/USD forecast remains unchanged,

towards 1.04 on a 12M horizon.

{kind=link}